Most people only think about taxes between January and April. Then the deadline passes, the documents get shoved in a drawer, and it all repeats the following year, usually with the same surprises, the same scramble, and the same frustration. But year round tax planning changes that cycle entirely. It turns reactive panic into a strategy you actually control, one that reduces what you owe and keeps you organized every month, not just during filing season.

At Tax Experts of OC, our CPAs and Enrolled Agents work with individuals and business owners across all 50 states who are tired of that last-minute rush. We've seen firsthand how a few consistent habits throughout the year lead to significantly lower tax bills and far less stress when April rolls around. The key isn't doing more, it's doing the right things at the right time.

This article breaks down five practical tax planning tips you can apply starting today, no matter where you are in the calendar year. Whether you're a W-2 employee trying to keep more of your paycheck or a business owner juggling quarterly obligations, these strategies are built for real life, not just theory. Let's walk through what actually moves the needle.

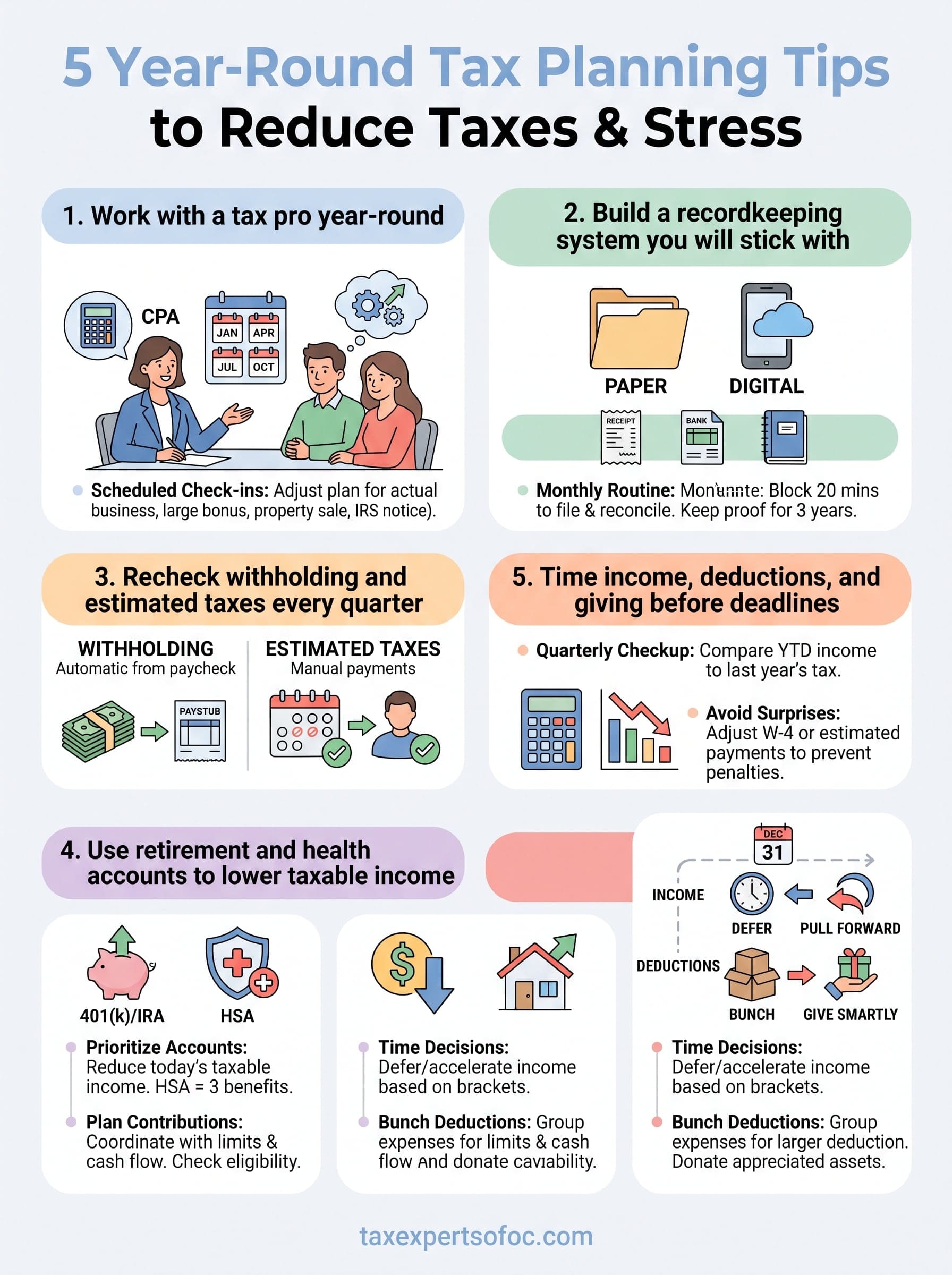

1. Work with a tax pro year-round

Most tax surprises are preventable. A qualified CPA or Enrolled Agent does more than prepare your return in April; they help you make smarter decisions all year. Bringing in a professional early means your strategy is set before the decisions are made, not after the money has already left your account.

What year-round tax planning with a pro looks like

Year round tax planning with a professional typically involves scheduled check-ins at key points throughout the year, not just one annual meeting. Your tax pro reviews your income, deductions, and any major life changes, then adjusts your plan to match your actual financial picture in real time rather than guessing from old data.

The moments you should not wait to get help

Certain events trigger immediate tax consequences that you cannot afford to ignore. Starting a business, receiving a large bonus, selling a property, getting married or divorced, or receiving an IRS notice are all situations where waiting costs you money or creates larger problems down the line.

If you receive any IRS correspondence, contact a tax professional before you respond.

What to bring to a planning meeting to save time and fees

Your meeting will be more productive when you arrive prepared. Bring your most recent tax return, recent pay stubs or profit-and-loss statements, documentation of any major purchases or sales, and a list of life changes from the past twelve months. The more complete your information, the faster your pro can build an accurate plan.

How to choose the right CPA or enrolled agent

Look for someone who holds an active CPA license or Enrolled Agent credential, since both are authorized to represent you before the IRS. Ask directly whether they work with clients year-round or only during filing season, and confirm they have direct experience with your specific situation, whether that is self-employment, multi-state income, or active IRS resolution.

2. Build a recordkeeping system you will stick with

Good records are the foundation of year round tax planning. Without them, you miss deductions, waste time reconstructing expenses, and hand your tax pro incomplete information that limits what they can do for you.

Decide on paper, digital, or hybrid and commit

Pick the format that matches how you actually work, not the one that sounds most organized. A simple folder system works fine if you use it consistently. Digital tools like a dedicated folder in Google Drive or a scanning app on your phone are low-cost and easy to maintain over time.

Create categories that map to your tax return

Organize your records around the same line items your tax return uses: income, business expenses, charitable contributions, medical costs, and home office if applicable. This reduces errors and saves time when your tax pro needs to locate specific documentation quickly.

Your records should be organized so that pulling any single category takes under two minutes.

Set a monthly routine in 20 minutes or less

Block 20 minutes each month to file receipts, reconcile accounts, and flag anything unusual. Short and consistent sessions beat one long annual scramble every time.

Keep audit-ready proof for common deductions and credits

Store receipts, bank statements, and written acknowledgments for charitable gifts over $250, mileage logs, and home office measurements. The IRS can audit returns up to three years back, so keep supporting records organized and accessible for at least that long.

3. Recheck withholding and estimated taxes every quarter

Paying too little tax throughout the year results in penalties and a large bill at filing time. Rechecking your withholding and estimated payments every quarter is a core part of year round tax planning that most people skip until it is too late.

Know the difference between withholding and estimated taxes

Withholding comes automatically from your paycheck, while estimated taxes are payments you make directly to the IRS four times a year if you are self-employed, have investment income, or earn other income without automatic withholding.

Run a quick quarterly checkup using your real numbers

Pull your actual year-to-date income and compare it to last year's tax liability. Then estimate whether your current payments will cover what you will owe by year-end.

The IRS generally requires you to pay at least 90% of your current year tax or 100% of your prior year tax to avoid underpayment penalties.

Avoid underpayment surprises and penalties

Underpayment penalties apply even when you pay your full balance by April 15. Submit quarterly payments on time using the IRS's scheduled due dates each year.

What to do if your income changes mid-year

Adjust your withholding immediately by submitting a new Form W-4 to your employer, or recalculate your estimated payment amounts for the next quarter so you stay current.

4. Use retirement and health accounts to lower taxable income

Tax-advantaged accounts are one of the most direct and legal ways to reduce taxable income. Making regular contributions part of year round tax planning means you capture every savings opportunity rather than scrambling at year-end.

Prioritize the accounts that reduce today's tax bill

Traditional 401(k) and IRA contributions reduce your taxable income in the year you make them. HSA contributions work the same way and carry over indefinitely, making them a powerful long-term tool if you have a qualifying health plan.

An HSA is the only account that offers three tax benefits: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Coordinate contributions with income limits and cash flow

Roth IRA eligibility phases out at higher income levels, so confirm your modified adjusted gross income first. Spread contributions across the year rather than depositing a lump sum in April to keep your cash flow steady.

Avoid common contribution and rollover mistakes

Exceeding annual limits triggers a 6% IRS excise tax on the excess amount. When moving funds between accounts, use a direct rollover to avoid the mandatory 20% withholding that applies to indirect distributions.

Special notes for self-employed and small business owners

Self-employed individuals can use a SEP-IRA or Solo 401(k), both of which allow much higher contribution limits than a standard IRA. A Solo 401(k) lets you contribute as both employer and employee, sheltering a significant share of your net self-employment income from federal tax.

5. Time income, deductions, and giving before deadlines

Timing decisions are one of the most powerful tools in year round tax planning. By controlling when income is received and deductions are claimed, you can shift your tax burden between years and keep more money in your pocket.

Decide when to accelerate or defer income legally

If you expect a lower tax bracket next year, defer income by delaying an invoice until January. If rates are likely to rise, pull income forward into the current calendar year before December 31.

Bunch deductions and plan big expenses with intent

Many taxpayers never itemize because the standard deduction is high. Bunching eligible expenses into a single year, such as medical costs or property taxes, can push you over the threshold and unlock a larger deduction in that year.

Make charitable gifts in a tax-smart way

Donating appreciated stock directly to a qualified charity lets you skip capital gains tax while claiming the full fair market value as a deduction. A donor-advised fund lets you take the deduction now and distribute grants to charities later.

The IRS requires a written acknowledgment from the charity for any single cash gift of $250 or more.

Harvest investment losses carefully and avoid wash sales

Selling losing positions offsets capital gains and up to $3,000 of ordinary income annually. Do not repurchase the same or substantially identical security within 30 days before or after the sale, or the IRS will disallow the loss under wash sale rules.

Next steps for a smoother tax year

Year round tax planning is not a single event. It is a set of consistent habits that compound over time, and the earlier in the year you start, the more options you have available to reduce what you owe. Every tip in this article works better when you apply it before deadlines force your hand, not after.

Start by picking one area to address this week, whether that is setting up a recordkeeping folder, checking your withholding, or scheduling a consultation with a qualified professional. Small actions taken early produce better outcomes than perfect plans executed too late. If your tax situation involves IRS debt, unfiled returns, or complex business income, do not wait until April to get clarity.

The team at Tax Experts of OC includes licensed CPAs and Enrolled Agents who work with clients in all 50 states. Schedule your free 30-minute consultation today and put a real plan in place for the rest of the year.