Running an LLC gives you real flexibility, but that flexibility extends to your tax return, too. Tax deductions for LLC owners can significantly reduce what you owe, yet many business owners leave money on the table simply because they don't know what qualifies as a write-off.

The IRS allows LLC owners to deduct ordinary and necessary business expenses, from office supplies and software to health insurance premiums and retirement contributions. The catch? You need to know which deductions apply to your specific situation, how to document them properly, and where the line sits between a legitimate write-off and a red flag on your return.

At Tax Experts of OC, our CPAs and Enrolled Agents work with LLC owners across all 50 states to identify every deduction they're entitled to, and structure their filings to hold up under scrutiny. Below, we break down 10 key tax deductions every LLC owner should know about, with practical details on eligibility, limits, and how to claim each one correctly.

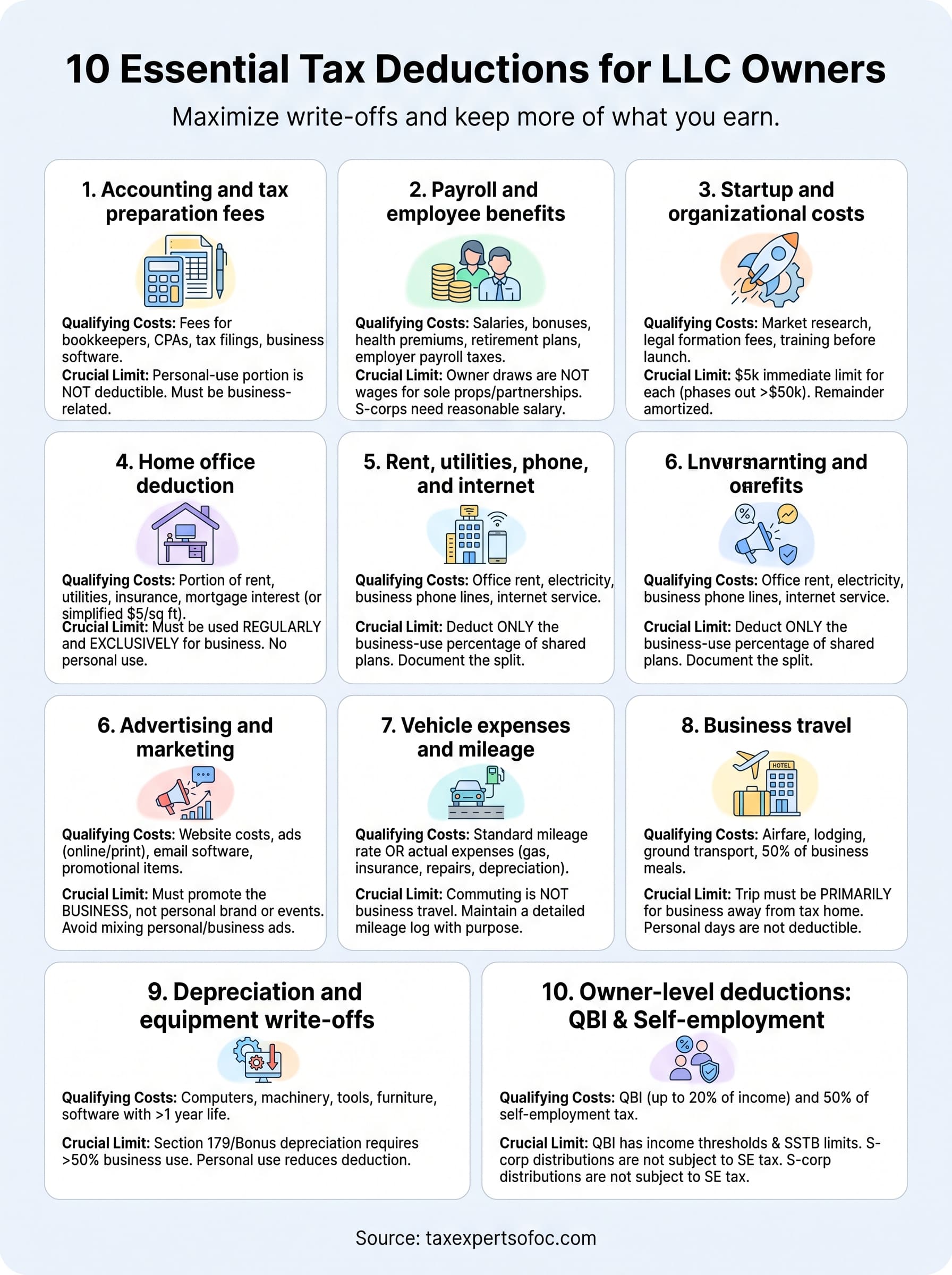

1. Accounting and tax preparation fees

This is one of the most reliable tax deductions for LLC owners, yet many underestimate its full scope. Any fees you pay to a CPA, Enrolled Agent, or bookkeeper to manage your business finances and prepare your business tax returns are generally deductible as ordinary and necessary business expenses under IRC Section 162.

Who can take this deduction based on LLC tax status

Your eligibility depends on how your LLC is taxed. Single-member LLCs taxed as sole proprietorships deduct these fees on Schedule C of your personal return. Multi-member LLCs taxed as partnerships report them on Form 1065. LLCs that elect S-corp or C-corp status deduct these costs directly at the entity level on their respective business returns.

One critical limit applies to disregarded entities: only the portion of fees tied to business tax preparation is deductible. Fees for the personal sections of your return do not qualify.

What costs qualify and where people go wrong

Qualifying expenses include fees for bookkeeping, tax return preparation, tax planning consultations, payroll tax filings, and audit representation. Business accounting software also qualifies if you use it exclusively for the business.

The most common mistake is deducting fees that cover personal financial matters. If your CPA prepares both your business and personal returns on one engagement, only the business-related portion is deductible. Ask your accountant to itemize the invoice so the allocation is explicit and audit-proof.

Never let a combined personal and business invoice go undocumented. A flat fee with no breakdown gives the IRS grounds to disallow the entire deduction.

Bookkeeping fees must also reflect work performed on business accounts only. Commingling personal and business recordkeeping on a single bill is a pattern that draws scrutiny during an audit.

What to keep for clean documentation

Retain itemized invoices from every accountant, bookkeeper, or tax professional you pay, along with bank or credit card statements that confirm payment. If your CPA charges one annual fee covering both business and personal work, request a written allocation by service type before you file.

Hold these records for at least three years from your filing date, or seven years if there is any question about income you reported.

2. Payroll and employee benefits

If your LLC has employees, the wages and benefits you provide them represent some of the largest deductible expenses available to you. These costs reduce your taxable income dollar for dollar, making payroll one of the most impactful tax deductions for LLC owners who have scaled beyond a solo operation.

Who can take this deduction based on LLC tax status

Every LLC structure can deduct employee wages, but the rules shift depending on how you file. Single-member LLCs report payroll costs on Schedule C, while multi-member LLCs use Form 1065. LLCs electing S-corp or C-corp status deduct payroll at the entity level, which also creates an opportunity to reduce self-employment tax through reasonable owner compensation.

What costs qualify and where people go wrong

Qualifying costs include employee salaries, bonuses, health insurance premiums, retirement plan contributions, and employer-paid payroll taxes. The most common mistake is classifying owner draws as wages. If your LLC is taxed as a sole proprietorship or partnership, you cannot deduct payments to yourself as payroll expenses.

If you elect S-corp status, the IRS requires you to pay yourself a reasonable salary, and that salary is deductible at the entity level.

What to keep for clean documentation

Keep payroll records, W-2s, Form 941 filings, and benefit plan documentation for every year you claim this deduction. Your payroll provider should generate most of these records automatically. Retain everything for at least four years after the tax due date for each return.

3. Startup and organizational costs

The IRS gives new LLC owners a structured way to recover early expenses, but the rules are specific. Understanding how startup deductions work before you file can prevent you from missing one of the more valuable tax deductions for LLC owners in the first year of business.

Who can take this deduction based on LLC tax status

Any LLC can take this deduction regardless of how it is taxed. Single-member LLCs deduct these costs on Schedule C, multi-member LLCs report them on Form 1065, and LLCs taxed as corporations handle them at the entity level. The deduction applies in the tax year your business becomes active, not when you first incur the costs.

What costs qualify and where people go wrong

Qualifying startup costs include market research, advertising before launch, consultant fees, and training expenses incurred before you opened for business. Organizational costs cover the fees paid to legally form the LLC, such as state filing fees and attorney costs to draft your operating agreement.

Under IRC Section 195, you can deduct up to $5,000 in startup costs and $5,000 in organizational costs in year one, with the remainder amortized over 180 months. If total startup costs exceed $50,000, the immediate deduction phases out dollar for dollar.

The most common mistake is deducting asset purchases as startup costs. Equipment and inventory are capitalized separately and do not fall under this category.

What to keep for clean documentation

Retain dated receipts, invoices, and contracts for every pre-launch expense, along with your state formation documents showing the date your LLC became official. A simple log that connects each expense to a specific business purpose protects the deduction if the IRS asks questions.

4. Home office deduction

The home office deduction is one of the most claimed and most audited tax deductions for LLC owners. If you use part of your home regularly and exclusively for business, you can deduct a portion of your housing costs, but the IRS applies strict criteria that trip up many filers.

Who can take this deduction based on LLC tax status

Single-member LLCs taxed as sole proprietorships claim the home office deduction on Schedule C using either the simplified method or the regular method. Multi-member LLCs cannot pass this deduction through to members on the partnership return; each member claims it on their own return instead. LLCs taxed as S-corps or C-corps cannot use this deduction at the entity level unless the business formally leases office space from the owner under a documented arrangement.

What costs qualify and where people go wrong

Under the regular method, you calculate the percentage of your home used exclusively for business and apply that figure to expenses like rent, mortgage interest, utilities, and insurance. The simplified method allows a flat $5 per square foot deduction, up to 300 square feet. The most common mistake is claiming a room that doubles as a guest bedroom or personal space, which violates the exclusive-use requirement and disqualifies the entire deduction.

The IRS requires the space to be used regularly and exclusively for business. Any personal use, even minor, voids the deduction completely.

What to keep for clean documentation

Keep a floor plan or diagram showing the square footage of the dedicated workspace versus your total home, along with rent or mortgage statements, utility bills, and insurance records. Dated photos of the dedicated space taken each year add a strong layer of protection if the IRS ever questions the deduction.

5. Rent, utilities, phone, and internet

If your LLC pays for a dedicated office space or uses utilities, phone lines, and internet service for business operations, those costs qualify as ordinary and necessary business expenses under IRC Section 162. This is one of the more straightforward tax deductions for LLC owners, but the business-use percentage requirement catches many people off guard.

Who can take this deduction based on LLC tax status

Every LLC structure can deduct these expenses regardless of how the business is taxed. Single-member LLCs deduct them on Schedule C, multi-member LLCs report them on Form 1065, and LLCs taxed as S-corps or C-corps deduct them at the entity level.

If you operate from a dedicated commercial space, the full rent and utility costs tied to that location are generally deductible without any proration required.

What costs qualify and where people go wrong

Qualifying expenses include office rent, electricity, gas, water, dedicated business phone lines, and internet service used for the business. The most common mistake is deducting the full cost of a phone or internet plan you also use personally.

You can only deduct the business-use percentage of any shared phone or internet plan, so document that split in writing before you file.

What to keep for clean documentation

Retain the following for every expense you claim:

- Monthly utility bills and lease agreements

- Written records showing the business-use percentage applied to any shared services

- Bank or credit card statements confirming each payment

Keep these records for at least three years from your filing date.

6. Advertising and marketing

Every dollar you spend promoting your business can reduce your taxable income. Advertising and marketing costs qualify as ordinary and necessary business expenses under IRC Section 162, making them one of the most accessible tax deductions for LLC owners regardless of business size or structure.

Who can take this deduction based on LLC tax status

Every LLC can deduct advertising and marketing expenses, regardless of its tax classification. Single-member LLCs taxed as sole proprietorships claim these costs on Schedule C, multi-member LLCs report them on Form 1065, and LLCs taxed as S-corps or C-corps deduct them directly at the entity level.

What costs qualify and where people go wrong

Qualifying expenses include website design and hosting, paid search ads, social media advertising, print materials, email marketing software, and promotional items that carry your business name. The most common mistake is deducting costs that benefit you personally rather than promoting the business.

Sponsoring a local event qualifies if the sponsorship is tied to your business brand, but paying for a personal social media presence does not, even if you occasionally mention your LLC.

A second mistake is mixing personal and business promotion on a single payment, such as running personal and business ads through the same account without separating costs by campaign.

What to keep for clean documentation

Retain invoices, ad platform statements, and receipts for every marketing expense you claim. For each item, keep a brief written note connecting the cost to a specific business promotion goal to reinforce the business purpose if the IRS ever asks.

7. Vehicle expenses and mileage

If you use a vehicle for business purposes, the IRS allows you to deduct those costs as ordinary and necessary business expenses. Vehicle deductions are among the more substantial tax deductions for LLC owners who regularly drive for client visits, deliveries, or other business-related activities.

.png)

Who can take this deduction based on LLC tax status

Every LLC structure can deduct vehicle expenses, but the method depends on how you file. Single-member LLCs report these costs on Schedule C, multi-member LLCs include them on Form 1065, and LLCs taxed as S-corps or C-corps deduct them at the entity level. If the LLC owns the vehicle outright, the deduction flows through the business return without any personal-use proration, provided the vehicle is used exclusively for business.

What costs qualify and where people go wrong

The IRS gives you two options: the standard mileage rate or the actual expense method, which covers gas, insurance, repairs, registration, and depreciation. The most common mistake is claiming personal commutes as business miles. Driving from home to your regular office is commuting, not business travel, and it does not qualify.

You must choose your deduction method in the first year you place the vehicle in service for business. Switching from the standard mileage rate to actual expenses later is restricted under IRS rules.

What to keep for clean documentation

Maintain a mileage log that records the date, destination, business purpose, and miles driven for every trip you deduct. If you use the actual expense method, also retain the following:

- Fuel receipts

- Insurance statements

- Repair and maintenance invoices

- Vehicle registration records showing ownership

8. Business travel

When your work takes you away from home overnight, the IRS allows you to deduct ordinary and necessary travel expenses as one of the more valuable tax deductions for LLC owners. The trip must be business-driven, require you to sleep away from your tax home, and last longer than a normal workday.

Who can take this deduction based on LLC tax status

Every LLC structure can deduct business travel costs. Single-member LLCs claim them on Schedule C, multi-member LLCs report them on Form 1065, and LLCs taxed as S-corps or C-corps deduct them at the entity level.

Your LLC's travel must be to a location away from your tax home, which the IRS defines as the city or general area where your principal place of business is located. Day trips that don't require an overnight stay do not qualify under these rules.

What costs qualify and where people go wrong

Qualifying expenses include airfare, lodging, ground transportation, baggage fees, and 50% of business meals eaten during travel. The most common mistake is extending a trip for personal reasons and then deducting the full cost. If you tack vacation days onto a business trip, you can only deduct the business-related portion of the expenses, not the personal days.

Travel must be primarily for business. If the personal component outweighs the business purpose, the IRS can disallow the entire deduction.

What to keep for clean documentation

Retain itineraries, boarding passes, hotel receipts, and meal receipts for every trip you deduct. For each trip, write a brief note identifying the business purpose, destination, and dates so the connection to your LLC is clear and verifiable if the IRS ever requests documentation.

9. Depreciation and equipment write-offs

When your LLC purchases physical assets like computers, machinery, or office furniture, the IRS lets you recover those costs over time through depreciation, or immediately through accelerated write-off provisions. These rules represent some of the most powerful tax deductions for LLC owners who invest in equipment to run their business.

Who can take this deduction based on LLC tax status

Every LLC structure can deduct depreciation and equipment costs regardless of how the business is taxed. Single-member LLCs report these deductions on Schedule C, multi-member LLCs include them on Form 1065, and LLCs taxed as S-corps or C-corps handle them at the entity level. The deduction applies in the year the asset is placed in service, not simply purchased.

What costs qualify and where people go wrong

Qualifying assets include computers, office furniture, machinery, tools, and business software with a useful life greater than one year. Under Section 179, you can deduct the full purchase price of qualifying equipment in the year you buy it, up to the annual limit. Bonus depreciation offers a similar immediate write-off. The most common mistake is deducting personal-use assets or equipment used only partially for business without applying the correct business-use percentage.

If your business-use percentage for an asset falls below 50%, Section 179 and bonus depreciation are both off the table for that item.

What to keep for clean documentation

Retain purchase receipts, invoices, and records showing the date each asset was placed in service. Also document the business-use percentage for any asset shared with personal use, and keep depreciation schedules your accountant prepares each year.

10. Owner-level deductions: QBI and self-employment

Two of the most significant tax deductions for LLC owners operate at the owner level rather than the business level: the Qualified Business Income (QBI) deduction and the self-employment tax deduction. Together, these can reduce your taxable income substantially, but the rules are precise and easy to misapply without professional guidance.

Who can take this deduction based on LLC tax status

Single-member LLCs and multi-member LLCs taxed as sole proprietorships or partnerships can claim both deductions. The self-employment tax deduction lets you deduct 50% of your self-employment tax from your gross income, which offsets the double burden of paying both the employer and employee share. The QBI deduction, created under the Tax Cuts and Jobs Act, lets eligible pass-through owners deduct up to 20% of qualified business income, subject to income thresholds and business type restrictions. LLCs taxed as S-corps do not pay self-employment tax on owner distributions, which changes the calculation significantly.

What costs qualify and where people go wrong

The QBI deduction phases out for specified service trade or business (SSTB) owners above certain income levels, and many professional LLC owners don't realize their business falls into this restricted category. Accountants, consultants, and financial advisors face stricter limits than other business types.

If your taxable income exceeds the threshold, the QBI deduction can shrink to zero for certain service businesses, so calculating this correctly before you file is essential.

What to keep for clean documentation

Retain your Schedule SE, Form 1040, and any supporting QBI worksheets your tax preparer generates. Document your net self-employment income clearly so the 50% deduction calculation is traceable if the IRS ever reviews your return.

Your next steps

Claiming every tax deduction for LLC owners you're entitled to requires more than a checklist. You need accurate records, the right filing method for your LLC's tax status, and a clear understanding of where the IRS draws the line on each category. Miss a detail on any of these deductions, and you either leave money behind or invite scrutiny you don't need.

Working with a qualified CPA or Enrolled Agent gives you the best chance of getting this right. A professional can review your current setup, identify deductions you may have missed in prior years, and build a documentation system that holds up if the IRS ever asks questions. If your returns are already filed and you believe you left deductions unclaimed, an amended return may recover what you missed.

Schedule a free 30-minute consultation with Tax Experts of OC to review your LLC's tax position and put every legitimate deduction to work for you.