Getting married changes a lot of things, and your tax situation is near the top of that list. Whether you recently tied the knot or have been filing together for years, tax planning for married couples requires a different approach than filing as a single taxpayer. The decisions you make now, from how you file to where you put your money, can mean thousands of dollars saved or lost each year.

The 2026 tax year brings its own set of rules, phase-outs, and opportunities that married filers need to pay attention to. Some couples leave money on the table simply because they don't know what's available to them. Others make filing choices based on habit rather than strategy, and overpay the IRS as a result.

At Tax Experts of OC, our CPAs and Enrolled Agents work with married couples across all 50 states to build tax strategies that actually fit their financial picture. Below, we break down six specific ways you and your spouse can reduce your tax bill this year.

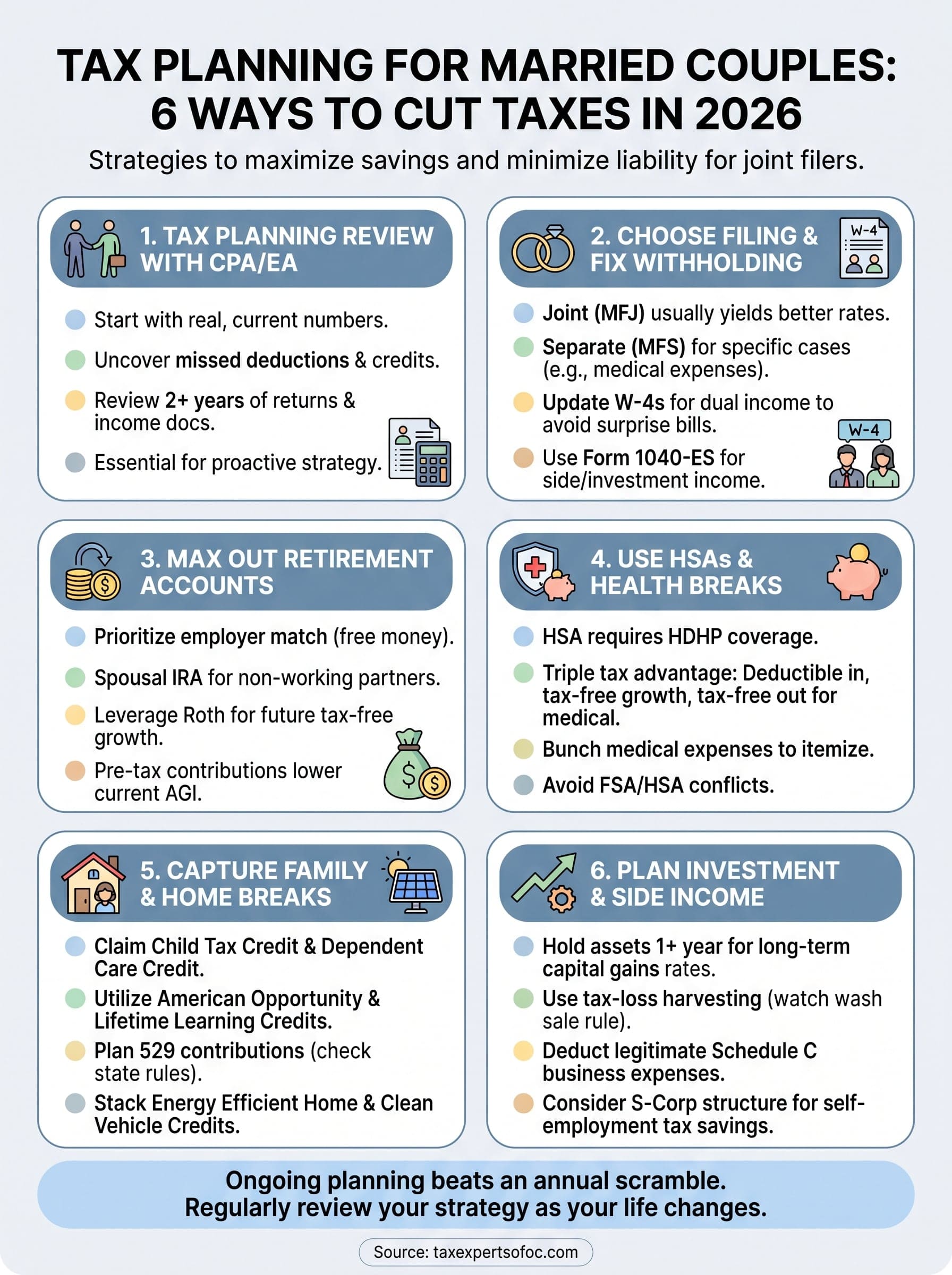

1. Start with a tax planning review with a CPA or EA

Before you make any decisions about deductions, contributions, or filing status, you need a clear picture of where you actually stand. A tax planning review with a licensed CPA or Enrolled Agent (EA) is the most effective first step for married couples who want to stop guessing and start making moves with real, current numbers behind them.

What you can uncover in one planning session

A single meeting with a qualified tax professional can surface opportunities you didn't know existed, from overlooked deductions to mismatched withholding between two incomes. You might discover that your combined household income pushes you into a higher bracket, that a Roth conversion this year would save you significantly down the road, or that you've been missing a credit you qualified for all along.

One focused session can pay for itself many times over when it uncovers a deduction or credit your previous filing missed entirely.

Documents and numbers to bring to get real answers

To get specific advice rather than general guidance, bring your most recent tax returns (at least two years), W-2s or 1099s for both spouses, current pay stubs, retirement account statements, and documentation for any major life changes such as a home purchase, a new dependent, or a business launch. The more complete your picture, the more precise and actionable your plan will be.

Your tax professional can only work with what you provide. Missing records translate directly into missed savings, so gather everything before your appointment.

When you need IRS representation, not just advice

If you have unfiled returns, unpaid balances, or an active IRS notice, a planning review is only the starting point. Enrolled Agents hold a federally authorized credential that lets them represent you directly before the IRS, which a general accountant or software product cannot do. If your situation involves collections or penalties, you need that level of authority in your corner.

How Tax Experts of OC can help married couples nationwide

Tax Experts of OC serves married couples across all 50 states through virtual consultations by phone and email. Whether you need proactive tax planning for married couples or resolution of an existing IRS problem, a CPA or EA on our team handles your case directly, not a general staff member, and your first 30-minute consultation is free.

2. Choose the right filing strategy and fix withholding

Your filing status and withholding setup directly determine how much you owe or receive each April. Most married couples default to filing jointly, but that choice deserves a deliberate annual review rather than an automatic assumption year after year.

Decide between married filing jointly and married filing separately

Filing jointly gives you access to more credits and lower effective tax rates in most situations. Filing separately can apply in specific cases, such as when one spouse carries significant medical expenses tied to an adjusted gross income threshold, but it typically eliminates credits like the Earned Income Credit and the Child and Dependent Care Credit entirely.

Run the numbers both ways with a CPA before you lock in a filing status, since the dollar difference can be substantial.

Reduce surprises by updating Form W-4 for two incomes

When both spouses work, your combined household income can push you into a higher bracket than either individual W-4 accounts for. Use the IRS Tax Withholding Estimator, then submit updated Form W-4s to both employers. That one step often eliminates the unexpected balance due that catches dual-income couples off guard each spring.

Use estimated taxes to avoid underpayment penalties

If either spouse receives freelance income, rental distributions, or self-employment income, withholding alone likely won't cover your full liability. Submit quarterly estimated tax payments using Form 1040-ES to stay current and avoid the underpayment penalty.

Watch for marriage penalty triggers and bracket creep

Strong tax planning for married couples means checking whether your combined income triggers phase-outs on credits like the Child Tax Credit. Bracket creep happens when two moderate incomes merge into a higher combined bracket, making proactive monitoring essential each year.

3. Max out retirement accounts as a couple

Retirement accounts are one of the most direct tools married couples have to reduce taxable income while building long-term wealth. Each contribution you make to a pre-tax account lowers your adjusted gross income for the current year, which can shift you into a lower bracket or unlock credits that phase out at higher income levels.

Prioritize 401(k) and 403(b) contributions and employer match

If both spouses have access to employer-sponsored plans, each can contribute up to $23,500 in 2026. Never leave employer matching contributions unclaimed since that match is essentially free additional compensation that also reduces your household tax burden.

Use IRAs strategically, including spousal IRA rules

Even if one spouse does not work, the spousal IRA rule allows a non-working partner to contribute up to $7,000 annually based on the working spouse's earned income. This doubles your household's IRA contribution capacity and can meaningfully reduce your combined taxable income.

A non-working spouse can still build a fully funded IRA as long as your household earned income covers both contributions.

Use Roth IRA, backdoor Roth, and conversion planning when income rises

When your combined income exceeds Roth IRA eligibility limits, the backdoor Roth strategy lets you contribute through a non-deductible traditional IRA and then convert it. Your money still grows tax-free and stays accessible under Roth distribution rules.

Coordinate retirement contributions with your tax bracket goals

Strong tax planning for married couples means matching your contribution types to your current and projected brackets. If you expect higher income in retirement, Roth contributions today may cost you less in lifetime taxes than pre-tax options.

4. Use HSAs and health-related tax breaks correctly

Effective tax planning for married couples includes health-related accounts, which offer a triple tax advantage that few other savings vehicles can match. Use these tools correctly and you reduce taxable income now, grow your balance tax-free, and spend it tax-free on qualified medical costs.

Confirm you qualify for an HSA through an HDHP

To open and contribute to a Health Savings Account (HSA), you must be enrolled in a High Deductible Health Plan (HDHP). For 2026, the IRS defines an HDHP as a plan with a minimum deductible of $1,650 for self-only or $3,300 for family coverage. Verify your plan qualifies before you make any contributions.

Max out HSA contributions and document qualified expenses

Married couples with family HDHP coverage can contribute up to $8,550 in 2026. Every dollar you put in lowers your adjusted gross income, making this one of the most straightforward deductions available. Keep receipts for every qualified expense you pay out of pocket.

An HSA is the only account that offers a tax deduction on contributions, tax-free growth, and tax-free withdrawals all in one.

Compare health deductions vs credits and timing strategies

If you itemize, unreimbursed medical expenses above 7.5% of your adjusted gross income are deductible. Bunching large costs into one tax year can push you past that threshold and produce a meaningful deduction when spreading them out would not.

Avoid common HSA and FSA coordination mistakes for couples

Contributing to an HSA while holding a general-purpose Flexible Spending Account (FSA) at the same time is not allowed. When one spouse carries an FSA through their employer, the other spouse's HSA eligibility is blocked unless that FSA is a limited-purpose account covering only dental and vision expenses.

5. Capture the biggest family and home tax breaks

Strong tax planning for married couples means treating family and housing costs as active tax opportunities. Several credits and deductions tied to your home and dependents carry significant dollar value that many couples miss entirely.

Claim child-related credits and dependent care benefits

The Child Tax Credit provides up to $2,000 per qualifying child, with a refundable portion available to lower-income households. If both spouses work, the Dependent Care Credit offsets daycare or after-school costs for children under 13, up to $3,000 for one child or $6,000 for two or more.

Use education credits and student loan interest rules without losing eligibility

The American Opportunity Credit covers up to $2,500 per student for the first four years of college, and the Lifetime Learning Credit applies to ongoing education costs. Student loan interest remains deductible up to $2,500, but it phases out at higher combined incomes, so track your adjusted gross income closely each year.

Filing jointly raises your combined income for phase-out calculations, making proactive income management essential before you lose these benefits.

Plan 529 contributions with your state tax rules in mind

Many states offer a state income tax deduction for contributions made to their own 529 plan. Check your state's specific rules since deduction caps and eligible expenses differ significantly across states.

- Earnings grow tax-free when withdrawn for qualified education expenses.

- Some states allow superfunding by front-loading five years of contributions at once.

Stack home energy credits and EV credits without missing requirements

The Energy Efficient Home Improvement Credit covers 30% of qualifying upgrades like insulation and heat pumps, capped at $3,200 per year. The Clean Vehicle Credit offers up to $7,500 for new EVs, but income thresholds and vehicle price caps can eliminate your eligibility entirely, so verify both before you commit to the purchase.

6. Plan investment income and side hustles to lower your bill

When both spouses earn income from investments or self-employment, tax planning for married couples expands well beyond wage income. These sources require active management throughout the year, not just at filing time, so you capture every available reduction.

Control capital gains with holding periods and gain harvesting

Assets held longer than one year qualify for long-term capital gains rates, which top out at 20% compared to ordinary income rates that can reach 37%. If your combined income falls in a lower bracket, you may pay 0% on long-term gains, making strategic gain harvesting a legitimate way to realize appreciation tax-free.

Use tax-loss harvesting and wash sale rules the right way

Selling investments at a loss offsets capital gains dollar for dollar and can reduce ordinary income by up to $3,000 per year. Watch the wash sale rule: repurchasing the same or substantially identical security within 30 days before or after the sale disqualifies your loss entirely.

Track every transaction across both spouses' accounts since the wash sale rule applies to your household, not just one individual account.

Deduct legitimate Schedule C expenses and track records that matter

Side income reported on Schedule C allows you to deduct direct business costs like home office use, equipment, and mileage. Keep detailed contemporaneous records because the IRS scrutinizes these deductions closely and missing documentation eliminates the deduction.

Evaluate entity choice, QBI deduction impact, and payroll planning

If your side business generates significant profit, structuring it as an S-corporation can reduce self-employment tax exposure considerably. Qualifying business income may also allow a 20% QBI deduction, which directly lowers your taxable income without requiring itemization.

Next Steps

Tax planning for married couples works best when you treat it as an ongoing process rather than an annual scramble. The six strategies above give you a solid foundation, but the real savings come from applying them consistently and adjusting as your income, family size, and goals shift from year to year.

Start by identifying which areas you haven't addressed yet. Whether you need to update your W-4 or open a spousal IRA, or review your investment income strategy, taking action on even one item this year puts you ahead of where most couples stand.

If you want a professional to walk through your full picture and identify what you're missing, schedule a free 30-minute consultation with Tax Experts of OC. Our CPAs and Enrolled Agents work with married couples across all 50 states and give you direct access to qualified professionals who build a plan around your specific numbers, not a generic template.