Every paycheck you issue triggers a chain of financial entries, wages, tax withholdings, employer contributions, benefits deductions, that all need to land in the right accounts. Payroll bookkeeping is the process of recording those transactions accurately in your financial records, and getting it wrong can mean misreported taxes, IRS penalties, and a distorted picture of your business's actual costs.

Yet many small business owners treat payroll and bookkeeping as separate tasks, handled by different people or disconnected software. That gap is where errors multiply. Wages get recorded in lump sums without breaking out liabilities. Employer tax contributions go untracked. Quarterly filings don't match what's in the general ledger. By the time someone notices, you're already behind, and cleaning up the mess costs more than doing it right the first time.

This guide walks through how payroll entries actually work in your books: the accounts involved, the journal entries you need to make, and the common mistakes that trip up business owners. We'll also cover how dedicated software and professional services fit into the picture. At Tax Experts of OC, our CPAs and Enrolled Agents handle both bookkeeping and payroll for businesses across all 50 states, so the advice here comes from what we see, and fix, every day. Whether you're recording payroll yourself or deciding it's time to hand it off to a professional, this article gives you the knowledge to make that call with confidence.

What payroll bookkeeping means

Payroll bookkeeping is the practice of recording every financial transaction tied to employee compensation into your accounting system. Each time you run payroll, you create a series of entries that reflect what you owe employees, what you owe tax authorities, and what the true cost of labor is to your business. It is not a single entry for the total check amount. It is a structured set of debits and credits that break gross pay, withholdings, employer taxes, and benefit deductions into their correct accounts within your general ledger.

Treating payroll as a single lump-sum expense is one of the most common and costly mistakes small business owners make in their financial records.

The two functions defined

Bookkeeping is the systematic recording of all financial transactions in a business. Every sale, purchase, payment, and liability gets logged into a general ledger through journal entries. Your bookkeeper, or your accounting software, maintains a chart of accounts that organizes every transaction into categories like assets, liabilities, equity, income, and expenses. The goal is to produce accurate financial records that show exactly where your business stands at any given point in time.

Payroll, by contrast, is the process of calculating and distributing employee compensation. That includes gross wages, salary, hourly pay, overtime, commissions, and bonuses. It also covers tax withholding calculations for federal income tax, Social Security, Medicare, and applicable state taxes, along with any voluntary deductions for health insurance or retirement plan contributions. Payroll produces the numbers. Bookkeeping records them. When the two functions operate without coordination, your financial statements end up incomplete or inaccurate.

What gets captured in payroll entries

When you run payroll, several distinct figures need to land in your books. You are not just recording what hits each employee's bank account. You are also recording the liabilities you now owe to the IRS, your state tax agency, your benefits providers, and any other parties involved in compensation. Here is a breakdown of the main elements that payroll entries capture:

- Gross wages: the total compensation earned before any deductions

- Employee tax withholdings: federal and state income tax, Social Security at 6.2%, and Medicare at 1.45%, all taken from the employee's pay

- Employer payroll taxes: your share of Social Security and Medicare, plus federal unemployment tax (FUTA) and state unemployment tax (SUTA)

- Voluntary deductions: health insurance premiums, 401(k) contributions, wage garnishments, or other agreed deductions

- Net pay: the amount actually deposited into each employee's account after all deductions

Each of these items affects different accounts in your ledger. Net pay reduces your cash or bank account. Withheld taxes and employer taxes create liability accounts that sit on your balance sheet until you remit those payments to the IRS or your state agency. Benefits deductions create their own separate payable accounts. Mapping each figure to its correct account is precisely what payroll bookkeeping requires, and it is what separates a clean, audit-ready set of books from a rough approximation of your labor costs. If any of these elements go unrecorded or land in the wrong account, your financial statements will misrepresent your actual expenses and outstanding obligations.

How payroll and bookkeeping work together

Payroll and bookkeeping are not independent systems that occasionally cross paths. Payroll generates the source data, and bookkeeping captures that data in your financial records. Every time you process payroll, it produces a report showing gross wages, tax withholdings, deductions, and net pay. Your bookkeeper, or your accounting software, then translates those figures into journal entries that update the general ledger. If the two processes operate in isolation, your balance sheet will carry untracked liabilities, and your income statement will understate your true labor costs by ignoring employer tax obligations entirely.

Payroll as a source document for your books

Think of each payroll run as a source document, similar to an invoice or a bank statement. It tells you exactly what happened during that pay period: who earned what, what was withheld from employee pay, and what you owe as the employer on top of those wages. Your bookkeeping process takes that document and posts the corresponding entries into the correct accounts. Gross wages hit your wage expense account, withheld taxes and employer contributions flow into liability accounts, and net pay reduces your cash balance. None of that happens accurately without a deliberate, structured link between your payroll process and your accounting records.

When payroll and bookkeeping operate as a unified process, your financial statements reflect the actual cost of labor, not just the cash that left your bank account on payday.

How timing connects the two functions

Payroll runs on a fixed schedule, whether weekly, biweekly, or semi-monthly, but bookkeeping needs to capture costs in the period they are earned, not just when cash moves. If your pay period ends on the 28th but payday falls on the 3rd of the following month, you need an accrual entry to record wages owed at month-end. This is where payroll bookkeeping demands more than basic data entry. It requires a working understanding of accrual accounting and how compensation cycles interact with your reporting periods. Businesses that skip those accrual entries often see their monthly profit figures swing significantly, not because revenue changed, but because labor costs are landing in the wrong month. Keeping payroll and bookkeeping tightly coordinated eliminates that distortion and gives you financial statements you can actually rely on when making decisions or preparing for tax season.

Why accurate payroll bookkeeping matters

Accurate payroll bookkeeping affects more than your accounting records. It directly shapes your tax compliance, your financial visibility, and your ability to avoid costly disputes with the IRS. When payroll entries are incomplete or inconsistently recorded, the consequences stack up quickly, and they rarely announce themselves until you are already dealing with a penalty notice or a cash flow problem you did not see coming.

Tax compliance and penalty avoidance

The IRS holds employers to strict deadlines for depositing payroll taxes, and those deposits must match the amounts you report on Form 941 each quarter. If your books do not accurately track withheld employee taxes and employer contributions as separate liabilities, you risk under-depositing or misreporting those amounts. The IRS failure-to-deposit penalty starts at 2% and can climb to 15% depending on how late the deposit is. Beyond deposit penalties, mismatched records between your general ledger and your payroll reports are a common trigger for IRS inquiries.

Getting your payroll entries right the first time costs far less than correcting them under pressure during an audit or after a penalty notice arrives.

Accurate records also protect you if a payroll dispute arises with an employee. Detailed journal entries that document gross wages, withholdings, and net pay for each period give you a verifiable paper trail that reconstructs exactly what was paid and when.

Your financial statements depend on it

Your income statement and balance sheet only tell an accurate story if payroll is recorded correctly. Gross wages are an expense, but employer taxes and unpaid benefits deductions are liabilities. If you book only the net pay as your total payroll cost, you are understating your actual labor expenses and hiding obligations that still need to be settled. That distortion makes your profit margins look stronger than they actually are, which can lead to bad decisions about hiring, pricing, or distributions.

Clean payroll records also make tax preparation faster and more accurate. When your bookkeeper or CPA can trace every payroll entry back to a specific pay run, reconciling quarterly and annual filings becomes straightforward rather than a reconstruction project. For businesses that rely on bank financing or investor reporting, financial statements built on accurate payroll data carry the credibility that lenders and stakeholders need to make informed decisions.

Gather the payroll details you must track

Before you can record a single journal entry, you need the raw data that each payroll run produces. Sloppy or incomplete source information is the root cause of most payroll bookkeeping errors, and no accounting system can fix what was never captured. Collecting the right details at the start of every pay period sets up every downstream entry for accuracy.

Employee compensation data

Your gross wages figure is the starting point for every payroll entry, but gross wages alone do not tell the full story. You need the breakdown behind that number: regular hours worked, overtime hours calculated at the correct premium rate, any commissions earned, and any bonuses issued during the period. Salaried employees still require documentation of their full-period pay rather than a single total, because period-specific records matter when you need to reconstruct payroll data for audits or disputes.

Keep a record for each employee that includes their pay rate, hours worked, and employment classification (full-time, part-time, or contractor). Contractors paid through 1099 arrangements do not flow through your payroll tax accounts the same way W-2 employees do, so mixing the two in your records creates serious classification and filing problems at tax time.

Tax and deduction records

Federal and state tax withholding amounts need to be captured separately for each employee, not combined into a single withholding total. You need the federal income tax withheld, Social Security withheld at 6.2% of gross wages, and Medicare withheld at 1.45%. If your state imposes income tax, that amount gets tracked independently as well. These figures feed your liability accounts directly, and they must match exactly what you remit to the IRS and your state agency each deposit period.

Mismatched withholding records are one of the most common reasons an employer's Form 941 does not reconcile with their general ledger.

Beyond taxes, you also need to track each voluntary deduction separately: health insurance premiums, retirement contributions, wage garnishments, or any other agreed deductions from employee pay. Each deduction creates a payable to a different party, and they all need their own accounts in your books. Document the employer's share of benefits as well, because that cost belongs in your payroll bookkeeping records as a labor expense, not just the employee portion.

Set up payroll accounts in your chart of accounts

Your chart of accounts is the foundation of your entire payroll bookkeeping system. Before you record a single journal entry, you need to create the specific accounts that will hold each component of your payroll transactions. Without the right structure in place, your entries have nowhere accurate to land, and your financial statements will mix expenses and liabilities in ways that distort both your income statement and balance sheet.

Expense accounts for labor costs

Every dollar you pay employees, and every dollar you owe on top of their wages as the employer, counts as a labor expense in your books. You need separate expense accounts to capture the different types of compensation your business issues. Keeping them distinct makes it easier to analyze your labor costs by category and produce accurate reports for tax preparation or business planning.

Set up these expense accounts in your chart of accounts:

- Wages and Salaries Expense (or separate accounts for hourly and salaried pay)

- Payroll Tax Expense (employer share of Social Security, Medicare, FUTA, and SUTA)

- Employee Benefits Expense (employer-paid health insurance premiums and retirement contributions)

Combining all labor costs into a single payroll expense account will obscure the true composition of your costs and make tax reconciliation harder at year-end.

Liability accounts for payroll obligations

Payroll liabilities are the amounts you owe to third parties after each payroll run: taxes you have withheld from employee pay, employer taxes you have calculated but not yet remitted, and benefits deductions you have collected but not yet forwarded. These do not belong in your expense accounts. They sit on your balance sheet as current liabilities until you make the actual payment to the IRS, your state agency, or your benefits provider.

Your liability accounts should include the following:

- Federal Income Tax Payable

- Social Security Tax Payable (combined employee and employer portions)

- Medicare Tax Payable (combined employee and employer portions)

- State Income Tax Payable

- FUTA Payable

- SUTA Payable

- Health Insurance Premiums Payable

- 401(k) Contributions Payable

Maintaining each liability in its own dedicated account lets you verify at any point exactly what you owe and to whom. When you make your tax deposits or remit benefits payments, you clear those liability balances directly, which keeps your books accurate and your obligations visible between every pay period.

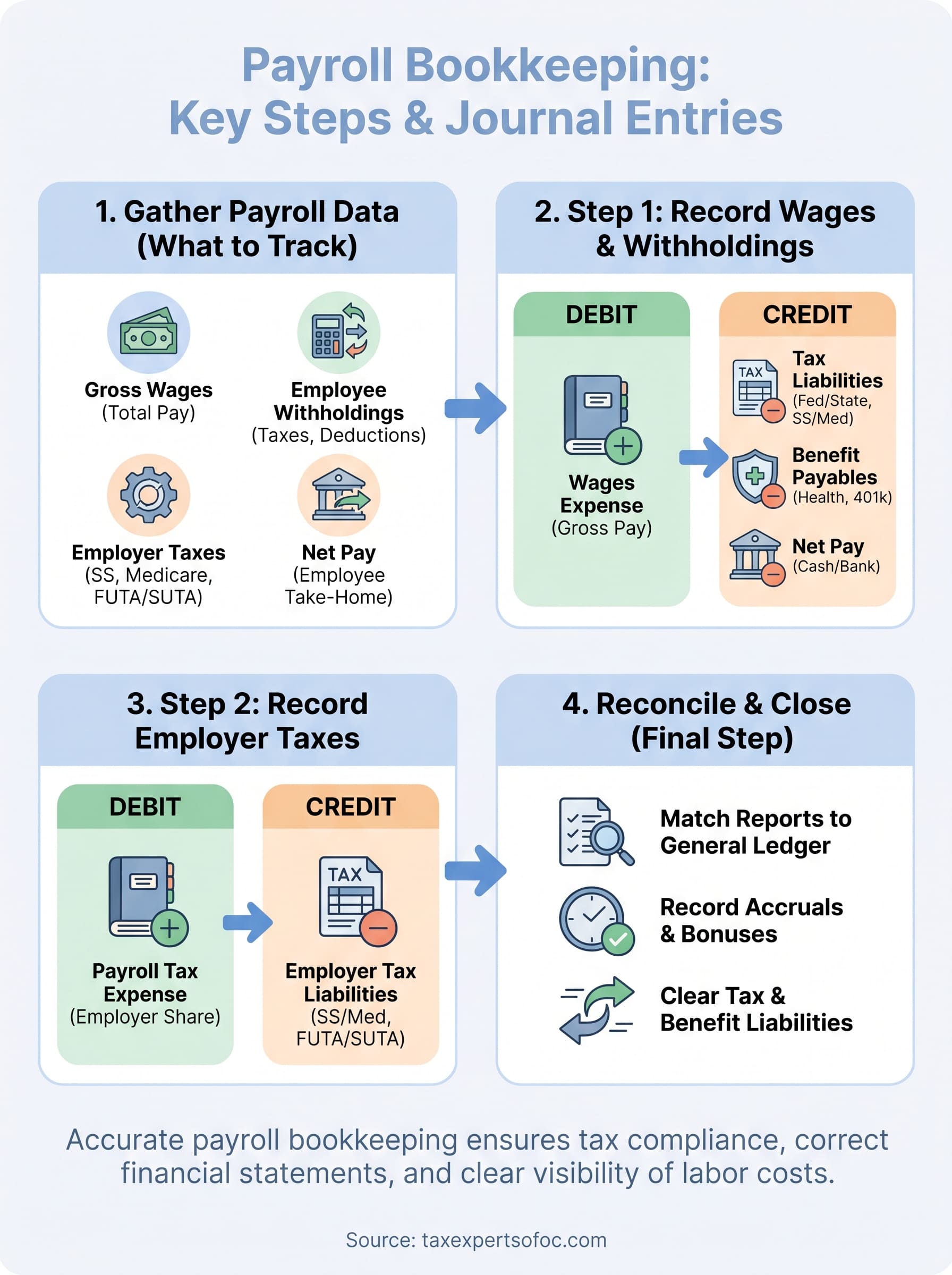

Record payroll step by step with journal entries

When you run payroll, you need to post two distinct journal entries to your general ledger. The first entry records the payroll obligation itself, capturing gross wages, employee withholdings, and net pay. The second records your employer tax expense and the corresponding liabilities. Together, these two entries complete the payroll bookkeeping cycle for each pay period and give you an accurate picture of what that payroll run actually costs your business.

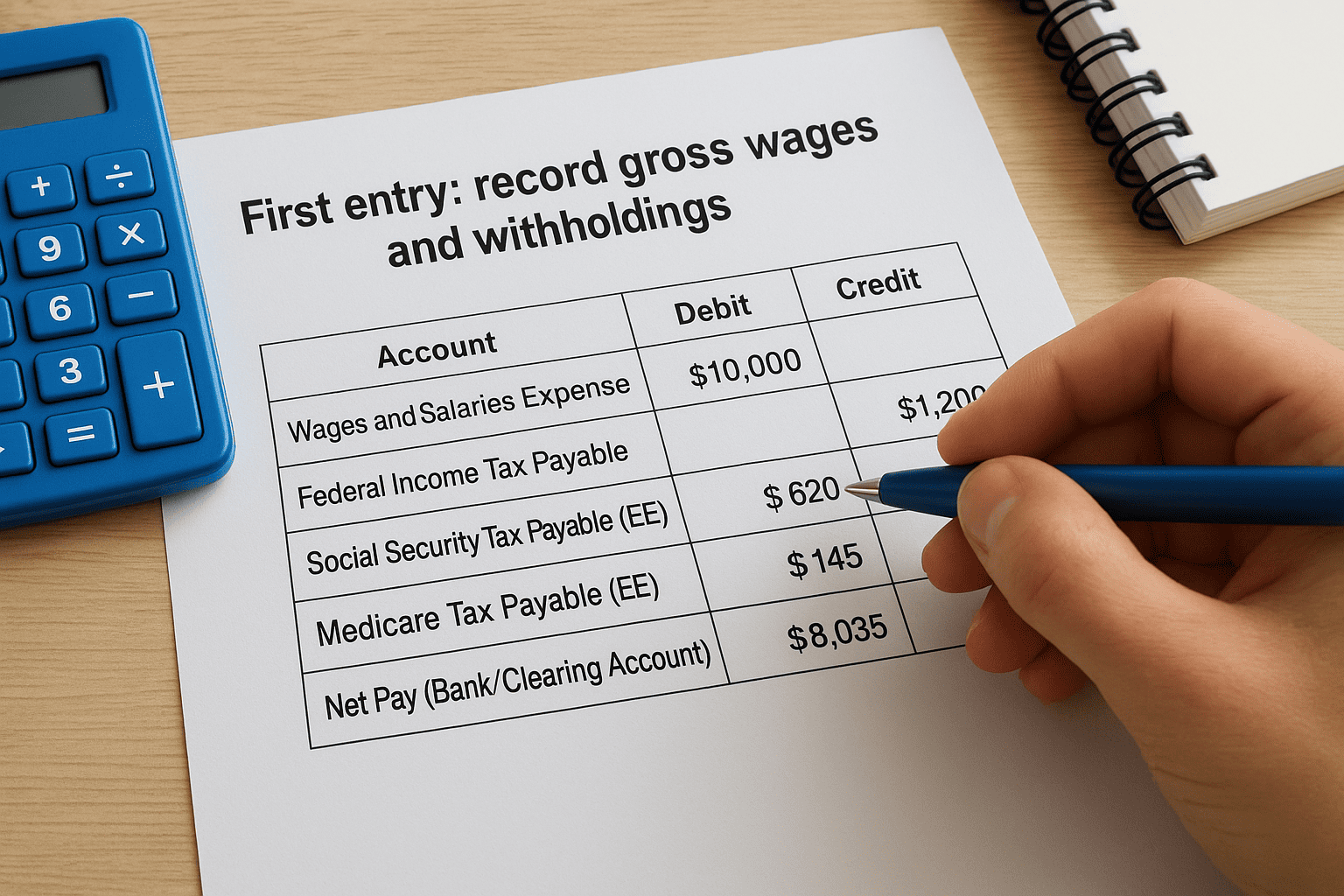

First entry: record gross wages and withholdings

Your first journal entry captures everything from the employee's perspective. You debit your Wages and Salaries Expense account for the total gross wages earned during the period. Then you credit each liability account for the amounts withheld from employee pay: federal income tax payable, Social Security tax payable, Medicare tax payable, state income tax payable, and any voluntary deductions. Finally, you credit your bank or payroll clearing account for the total net pay deposited into employee accounts.

Here is how a simplified first entry looks for a single pay period with $10,000 in gross wages:

| Account | Debit | Credit |

|---|---|---|

| Wages and Salaries Expense | $10,000 | |

| Federal Income Tax Payable | $1,200 | |

| Social Security Tax Payable (EE) | $620 | |

| Medicare Tax Payable (EE) | $145 | |

| Net Pay (Bank/Clearing Account) | $8,035 |

Every liability account you credit in this entry represents a real obligation that stays on your balance sheet until you remit the payment to the IRS or the appropriate tax agency.

Second entry: record employer payroll taxes

Your second journal entry records the employer-side tax costs that never touch employee pay. You debit your Payroll Tax Expense account for the total employer taxes owed: your matching share of Social Security at 6.2%, Medicare at 1.45%, plus FUTA and SUTA. You then credit each corresponding liability account for those same amounts. These liabilities sit on your balance sheet alongside the employee withholdings until you make the actual deposits.

Once both entries are posted, your books reflect the full cost of that payroll run, not just the cash that left your bank account on payday. When you remit taxes to the IRS, you debit each tax liability account and credit your bank, which clears the balance and confirms that specific obligation is fully settled for the period.

Handle accruals, bonuses, and benefits correctly

Not every payroll cost hits your books on payday. Accruals, bonuses, and employer-paid benefits each require their own treatment in your payroll bookkeeping records, and handling them incorrectly will distort your monthly financial statements and create reconciliation problems when you close out each period. Understanding how to record these three categories keeps your labor costs accurate in the period they belong to.

Record accrued wages at period end

When a pay period spans two calendar months, employees earn wages before you actually pay them. You need to record that liability at month-end through an accrual entry, even though no cash moves yet. Debit your Wages and Salaries Expense account for the wages earned in the current period, and credit an Accrued Wages Payable account on your balance sheet. When payday arrives in the following month, you reverse the accrual and post the standard payroll entry. Skipping this step causes your labor expenses to fall in the wrong month, which makes your profit figures unreliable for any period where a pay cycle crosses a month boundary.

Accrual entries for wages are not optional adjustments. They are the mechanism that keeps your income statement accurate to the actual period your employees worked.

Book bonuses as liabilities before they are paid

When you commit to paying an employee a bonus, that obligation exists the moment you make the decision, not the moment you write the check. Debit your Bonus Expense account and credit a Bonus Payable liability account as soon as the bonus is earned or approved. This approach matches the cost to the period it relates to rather than the period it is paid, which is especially important for year-end or performance bonuses that are declared in December but distributed in January. When you process the actual bonus payment, you debit Bonus Payable and credit your bank account to clear the liability.

Track employer-paid benefits as separate costs

Employer contributions toward health insurance, dental coverage, and retirement plans are part of your total labor cost, but they do not flow through employee paychecks. Each employer contribution needs its own expense and liability accounts in your chart of accounts. Debit Employee Benefits Expense for the amount you contribute, and credit the corresponding benefits payable account. When you remit the payment to your insurance carrier or retirement plan administrator, you clear the payable balance by debiting it and crediting your bank account, the same pattern you use for payroll tax deposits.

Reconcile payroll and close each period

Reconciliation is the step where you confirm that what your payroll records show matches what is actually in your general ledger and your bank account. Without it, small discrepancies build up over time and turn routine payroll bookkeeping into a correction project at year-end. Running a clean reconciliation after every pay period keeps your books accurate and your tax liabilities visible before they become problems.

Match your payroll reports to your general ledger

Your payroll processor or software produces a payroll register after each run. That report shows gross wages, every withholding, employer taxes, and net pay by employee. Your job is to compare those totals line by line against the journal entries you posted in your general ledger. Every figure on the payroll register should have a corresponding debit or credit in your books. If the numbers do not match, you need to find the discrepancy before you move forward.

A single transposition error in one payroll entry will throw off every liability balance you carry until you catch and correct it.

Check your bank account or payroll clearing account as well. The total net pay on your payroll register should equal the total withdrawals or ACH payments that left your account on payday. If you use a clearing account to process payroll, it should return to a zero balance after all entries post. A non-zero clearing account balance means a transaction did not record correctly, and you need to track it down before closing the period.

Clear your tax liability accounts before closing

Once you have confirmed your journal entries match the payroll register, review each tax liability account on your balance sheet. Any amount you have already remitted to the IRS or your state agency should have been cleared when you posted the payment entry. What remains in those accounts represents taxes still owed for the current period. Before you close the period, confirm that the balance in each liability account matches exactly what you will owe on your next deposit deadline.

Run the same check for benefits payable accounts. Confirm that premiums and retirement contributions forwarded to carriers and plan administrators have been cleared, and that only the current period's obligations remain open. Closing each period with accurate liability balances ensures that your balance sheet reflects exactly what you owe, nothing more and nothing less.

Choose software or outsource payroll bookkeeping

At some point, the manual journal entry approach stops being practical. As your headcount grows, pay structures become more complex, and the time cost of recording every payroll entry by hand starts to outweigh the savings. You have two realistic options: use dedicated software that automates the entries, or hand the entire function to a professional who handles both payroll and bookkeeping as an integrated service. Which path makes sense depends on the complexity of your payroll, your comfort with accounting, and what your time is actually worth.

Use payroll software to automate the entries

Most modern payroll platforms connect directly to your accounting software and post journal entries automatically after each payroll run. When you process payroll in a system like QuickBooks Payroll or a comparable platform, the software calculates gross wages, withholdings, and employer taxes, then maps each figure to the accounts you have set up in your chart of accounts. This eliminates the manual step of building each entry yourself and reduces the risk of transposition errors on tax withholding amounts.

Software works well when your payroll is straightforward: a consistent number of W-2 employees, standard deductions, and no complex multi-state tax situations. The limitation is that automated entries are only as accurate as your setup. If your chart of accounts is not configured correctly, or if the system maps wages to the wrong expense categories, you will produce clean-looking books that contain real errors. You still need to review the entries after each run and reconcile the output against your payroll register.

When to outsource to a professional

If you are dealing with multi-state payroll, contractor and employee classifications, accrual entries, or year-end reconciliation, the value of professional oversight rises significantly. A CPA or Enrolled Agent who manages both your payroll and your books will catch discrepancies between your tax deposits and your general ledger before they compound into a filing problem.

Outsourcing payroll bookkeeping to a qualified professional is not just a time decision. It is a risk management decision, particularly if your business has faced IRS notices or has a history of inconsistent records.

Tax Experts of OC works with businesses across all 50 states to handle payroll and bookkeeping together, keeping your records accurate and your tax obligations current. If your current process leaves you uncertain about what your books actually reflect, that is the clearest sign it is time to bring in professional support.

Next steps

Accurate payroll bookkeeping starts with the right accounts, the right entries, and a consistent reconciliation habit after every pay period. You now have the framework to record gross wages, withholdings, employer taxes, accruals, bonuses, and benefits in a way that keeps your books and tax obligations current. The gap between knowing the process and executing it cleanly is where most small business owners run into trouble, especially as payroll complexity grows with each new hire or state you operate in.

If your current records are inconsistent, your tax deposits have not matched your filings, or you simply want a professional managing both functions together, Tax Experts of OC can help. Our CPAs and Enrolled Agents work with businesses across all 50 states to handle payroll and bookkeeping as a unified service, so nothing falls through the gap between the two. Schedule your free 30-minute consultation to get started.