Missing a payroll tax deadline, even by a single day, triggers penalties that start accumulating immediately. Payroll tax penalties are among the most aggressively enforced consequences in the tax code because these funds include money withheld from employees' wages for Social Security, Medicare, and federal income tax. The IRS treats this as trust fund money, and when it isn't deposited on time or at all, the response is swift.

Penalty rates range from 2% to 15% of the unpaid amount depending on how late the deposit is, and that's before interest starts compounding. For business owners already managing tight margins, a single oversight in payroll processing can snowball into a five-figure liability. What makes this worse is that the IRS can hold individual officers and owners personally liable through the Trust Fund Recovery Penalty, meaning your personal assets are on the line, not just your business accounts.

At Tax Experts of OC, our CPAs and Enrolled Agents work directly with business owners across all 50 states to resolve payroll tax issues before they escalate. We've seen firsthand how quickly these penalties pile up and how much damage they cause when left unaddressed.

This article breaks down the specific penalty rates, the most common triggers that lead to them, and the concrete steps you can take to stay compliant. Whether you're behind on deposits or trying to prevent problems before they start, you'll find actionable guidance grounded in current IRS rules.

Why payroll tax penalties matter for employers

Payroll tax penalties don't work like most IRS fines. Most tax penalties allow some breathing room or carry a flat, predictable rate. Payroll penalties, by contrast, stack in layers: deposit penalties, failure-to-file penalties, failure-to-pay penalties, and compounding interest, all running simultaneously. For a small business owner managing tight cash flow, this layering effect can transform a $5,000 oversight into a liability exceeding $20,000 within a matter of months, often before you realize the full scope of the problem.

The scale of financial exposure

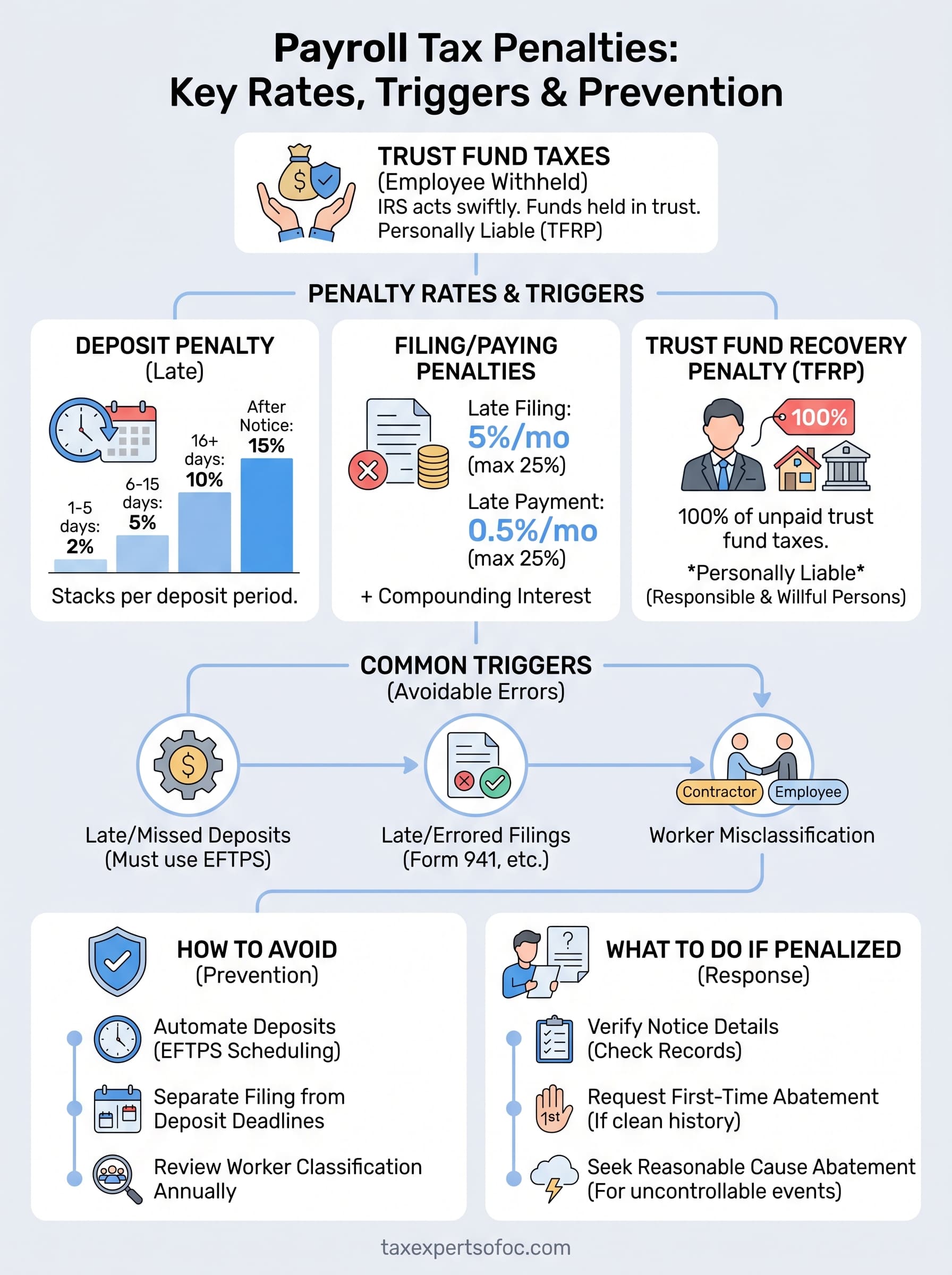

The raw dollar amounts here are significant enough to threaten the survival of a business. The IRS deposit penalty structure starts at 2% for deposits that are one to five days late, climbs to 5% for six to fifteen days late, and reaches 10% for anything beyond fifteen days. When you fail to deposit at all after the IRS sends a formal notice, the rate jumps to 15% of the unpaid amount.

These percentages apply per deposit period, not once per year, which means a business missing multiple payroll cycles can face penalties stacking across dozens of separate occurrences at the same time.

That math compounds quickly. Consider a business running a $50,000 biweekly payroll that misses three consecutive deposit deadlines by more than fifteen days. Deposit penalties alone in that scenario can exceed $7,500, and that number does not include the failure-to-pay or failure-to-file penalties that typically run alongside them. Add interest on the unpaid balance, and the actual liability can climb considerably higher before you receive a single formal notice from the IRS.

Personal liability extends beyond your business

Most business owners assume that forming an LLC or a corporation protects their personal finances from IRS collection. With payroll taxes, that assumption does not hold. The IRS uses a separate enforcement tool called the Trust Fund Recovery Penalty (TFRP), and it targets individuals directly, not just the business entity itself.

Under the TFRP, any person the IRS considers "responsible" and "willful" in failing to collect or remit trust fund taxes becomes personally liable for 100% of the unpaid trust fund portion. The IRS defines "responsible persons" broadly, and that definition can include business owners, officers, directors, and even certain employees who have authority over payroll decisions. Your personal bank accounts, home, and other assets all become vulnerable the moment the IRS pursues this avenue.

The operational ripple effect

Beyond the immediate financial damage, unresolved payroll tax problems create serious disruptions to your day-to-day operations. When the IRS moves into active collection, it can file liens against your business assets, levy your bank accounts, or garnish payments that clients or third parties owe you. These actions can halt your ability to meet other obligations, pay vendors, or keep operations running normally.

Ongoing payroll tax debt also damages your business credit profile, complicates future financing applications, and can disqualify you from government contracts or vendor relationships that require clean tax compliance records. Lenders and partners do look at this. What starts as a single missed deposit deadline can escalate into full IRS enforcement action that consumes significant time, money, and management attention you cannot afford to redirect away from your core business.

Payroll taxes and deadlines you must manage

Managing payroll means more than cutting paychecks to employees. You are responsible for withholding the correct amounts from each paycheck, matching certain employer contributions, depositing those funds with the IRS on a strict schedule, and filing the corresponding returns on time. Missing any one of these steps creates the conditions for payroll tax penalties to accumulate.

The taxes you are responsible for

Federal income tax withholding is the first category. You withhold this amount from each employee's paycheck based on the information they provide on their Form W-4, and the withheld amount goes directly to the IRS. The second category is FICA taxes, which cover Social Security and Medicare. Employees pay 6.2% of wages toward Social Security and 1.45% toward Medicare, and you as the employer must match both contributions dollar for dollar, making your total FICA obligation 15.3% of covered wages.

Your Federal Unemployment Tax (FUTA) obligation is separate and comes entirely from the employer side, not from employee wages. The standard FUTA rate is 6% on the first $7,000 of each employee's wages, though most employers qualify for a credit that reduces that effective rate to 0.6% after paying state unemployment taxes. State payroll tax requirements vary and run parallel to federal obligations, so you need to track both sets of deadlines independently.

Deposit schedules and filing deadlines

The IRS assigns you a deposit schedule, either monthly or semi-weekly, based on your total tax liability during a prior lookback period. Monthly depositors must submit taxes by the 15th of the following month. Semi-weekly depositors follow a tighter schedule: taxes on wages paid Wednesday through Friday are due by the following Wednesday, and taxes on wages paid Saturday through Tuesday are due by the following Friday.

If your accumulated liability reaches $100,000 on any single day, the IRS requires you to deposit those funds by the next business day, regardless of your normal assigned schedule.

Beyond deposits, you must file Form 941 quarterly to report withheld income taxes and FICA contributions. Form 940, which covers FUTA, is an annual filing due by January 31 of the following year. Missing these filing deadlines triggers separate penalties that stack on top of any deposit penalties you already owe.

Common payroll tax penalties and current IRS rates

The IRS enforces several distinct payroll tax penalties, and each one targets a specific failure in the payroll compliance process. Understanding which penalty applies to which situation matters because these penalties do not replace one another. They stack, and each carries its own rate structure that can significantly change your total liability depending on the specific violation.

Failure to Deposit Penalty

When you miss a federal tax deposit or deposit less than the required amount, the IRS applies a penalty based on how many days late the deposit arrives. The rate structure breaks down as follows:

| Days Late | Penalty Rate |

|---|---|

| 1 to 5 days | 2% |

| 6 to 15 days | 5% |

| 16 or more days | 10% |

| After IRS notice | 15% |

Each deposit period is evaluated separately, meaning if you miss multiple payroll cycles, the IRS applies the penalty calculation to each one individually. A pattern of late deposits across even a few payroll cycles can push your total penalty exposure well beyond what you originally owed in taxes.

Failure to File and Failure to Pay Penalties

Missing the Form 941 filing deadline triggers a failure-to-file penalty of 5% of the unpaid tax for each month or partial month the return is late, capped at 25% of the total unpaid amount. This penalty starts accruing the day after the due date, not after you receive a notice.

When both the failure-to-file and failure-to-pay penalties apply in the same month, the IRS reduces the failure-to-file rate by the failure-to-pay rate, but the combined financial impact remains significant.

The failure-to-pay penalty runs at 0.5% per month on the unpaid balance, also capped at 25%. On top of both penalties, the IRS charges interest on all unpaid amounts at the federal short-term rate plus 3 percentage points, adjusted quarterly.

Trust Fund Recovery Penalty

This penalty stands apart from deposit and filing penalties and carries the most severe personal financial consequences. The IRS calculates the Trust Fund Recovery Penalty at 100% of the unpaid trust fund taxes, which includes the income tax and employee-side FICA amounts you withheld from wages but never remitted.

Any person the IRS considers both responsible and willful in the failure to remit these funds faces direct personal liability. That definition can reach owners, officers, directors, and even employees who had authority over payroll decisions.

Triggers that lead to payroll tax penalties

Payroll tax penalties don't happen randomly. Specific actions and avoidable oversights set them in motion, and understanding what triggers them puts you in a position to prevent them before they start. The IRS tracks every deposit, every return, and every discrepancy between what you withheld from employees and what you actually remitted to the government.

Missing or Late Deposit Deadlines

The most common trigger is simply depositing late. The IRS assigns you a deposit schedule, and any payment that arrives even one day after the deadline generates a penalty. Cash flow problems, new payroll software, and banking delays don't exempt you from the penalty calculation. The IRS expects the funds on time regardless of the reason they didn't arrive.

A related issue is depositing through the wrong channel. The IRS requires federal payroll deposits to go through the Electronic Federal Tax Payment System (EFTPS), and a check sent directly to the IRS rather than processed through EFTPS counts as a failed deposit. Depositing the correct amount through the wrong method still triggers the full penalty structure.

Sending a check to the IRS instead of using EFTPS is treated the same as not depositing at all under current IRS rules.

Filing Returns Late or With Errors

Late Form 941 filings operate as a second major trigger that runs independently from deposit penalties. Even when you've deposited all taxes on time, failing to file the quarterly return by its deadline generates a separate failure-to-file penalty. Errors on the return, such as misreported wages or incorrect withholding amounts, can also create discrepancies that lead to additional IRS assessments.

Amended returns that reveal underreported amounts expose you to back interest on the corrected balance alongside the penalties. Rounding errors and data entry mistakes in payroll software frequently cause these discrepancies, and a small error on one quarterly return can create a chain of mismatched records across multiple filing periods.

Misclassifying Workers

Treating employees as independent contractors to sidestep payroll tax obligations is one of the triggers the IRS audits most aggressively. When you misclassify a worker, you skip withholding federal income tax, Social Security, and Medicare, creating an immediate liability the moment the IRS identifies the arrangement. The IRS can reclassify those workers retroactively and assess all unpaid payroll taxes going back multiple years.

.png)

Beyond the back taxes, misclassification exposes you to penalties covering every payroll period where the correct withholding didn't happen. Both the employer share and the employee share of FICA become your responsibility in a reclassification scenario, along with interest that has been accruing since each original missed payment.

How to avoid payroll tax penalties

Avoiding payroll tax penalties comes down to building consistent habits around your deposit schedule, filing calendar, and internal controls. The IRS doesn't offer automatic forgiveness for honest mistakes, and the penalty structure escalates quickly enough that prevention is significantly cheaper than resolution. Setting up the right systems before a problem occurs is the most effective strategy available to you.

Enroll in EFTPS and Automate Your Deposits

The Electronic Federal Tax Payment System (EFTPS) is the required channel for all federal payroll tax deposits, and setting it up correctly from the start removes one of the most common penalty triggers. You can schedule deposits in advance through the system, which means your payments process automatically even when you're focused on other parts of your business.

Scheduling your EFTPS deposits at least one business day before the due date gives you a buffer against banking delays or processing issues that could otherwise make an on-time deposit arrive late.

Once enrolled, track your deposit schedule type (monthly or semi-weekly) and build calendar reminders that account for your specific payroll cycle. When your tax liability hits $100,000 on any single day, the next-day deposit rule applies regardless of your normal schedule, so staying on top of daily totals matters as much as knowing your regular deadlines.

Keep Filing Deadlines Separate From Deposit Deadlines

Many business owners assume that depositing on time is enough, but Form 941 must still be filed quarterly even when all deposits are current. Treat your filing deadlines as an independent calendar item, not as a byproduct of completing your deposits. A dedicated payroll compliance calendar that lists every deposit due date and every return deadline in one place reduces the chance that a filing deadline slips through during a busy quarter.

Review Worker Classifications Before Each Tax Year

Misclassification is one of the most expensive avoidable errors in payroll. Before each tax year starts, review the working arrangements of every person you pay, particularly contractors who work regular hours, use your equipment, or take direction from your management team. The IRS applies behavioral control, financial control, and relationship type tests to determine classification, and you can find detailed guidance in IRS Publication 15-A. Getting this right upfront protects you from retroactive assessments that can cover multiple years of unpaid payroll taxes at once.

What to do if you receive a penalty notice

Receiving a payroll tax penalty notice from the IRS does not mean your only option is to pay the full amount immediately. Your response in the first few weeks determines how much you ultimately owe and whether the IRS escalates to more aggressive collection. Acting quickly and systematically gives you the best chance of reducing or eliminating the penalty.

Review the Notice and Verify the Details

The first thing you should do is read the notice carefully and confirm that the penalty is actually accurate. The IRS does issue notices with errors, and the deposit records or return filings they reference may not match what you submitted. Pull your EFTPS transaction history and internal payroll records and compare them line by line against what the notice describes.

If you find a discrepancy, you have the right to dispute the notice directly with the IRS. Document the evidence, including bank confirmation numbers, EFTPS transaction confirmations, and timestamped filing records, and respond in writing before the deadline listed on the notice. Ignoring even a potentially incorrect notice puts you in a worse position because the IRS will treat it as accepted.

Request Penalty Abatement if You Qualify

The IRS offers first-time penalty abatement for taxpayers who have a clean compliance history, meaning no penalties in the three years prior to the notice. If you qualify, you can request this relief by calling the number on the notice or submitting a written request. First-time abatement applies to failure-to-deposit, failure-to-file, and failure-to-pay penalties, and the IRS grants it administratively without requiring detailed explanations of why the failure occurred.

If first-time abatement doesn't apply, you can still request reasonable cause abatement by showing that the failure resulted from circumstances outside your control, such as a natural disaster, serious illness, or banking system failure.

For situations involving significant payroll tax penalties, especially those that include a Trust Fund Recovery Penalty assessment, working with a CPA or Enrolled Agent changes the outcome. A qualified professional can file the correct forms, communicate directly with the IRS on your behalf, and negotiate resolution options like installment agreements or offers in compromise. The IRS website outlines the formal process for responding to employment tax notices if you want to review it directly.

Next steps

Payroll tax penalties move fast once they start. The deposit penalty structure, filing deadlines, and the personal liability exposure through the Trust Fund Recovery Penalty all create a situation where waiting to act makes the problem significantly more expensive. If you're current on your deposits and filings, the steps in this article give you a solid framework to stay that way. If you're already dealing with a penalty notice or back payroll taxes, the time to respond is now, not after the next notice arrives.

Qualified professional help changes outcomes when payroll tax issues reach the IRS collection stage. At Tax Experts of OC, our CPAs and Enrolled Agents work directly with business owners to resolve employment tax problems and negotiate with the IRS on your behalf. Start with your free 30-minute consultation to understand exactly where you stand. Contact Tax Experts of OC today to get direct answers from a qualified professional, not general staff.