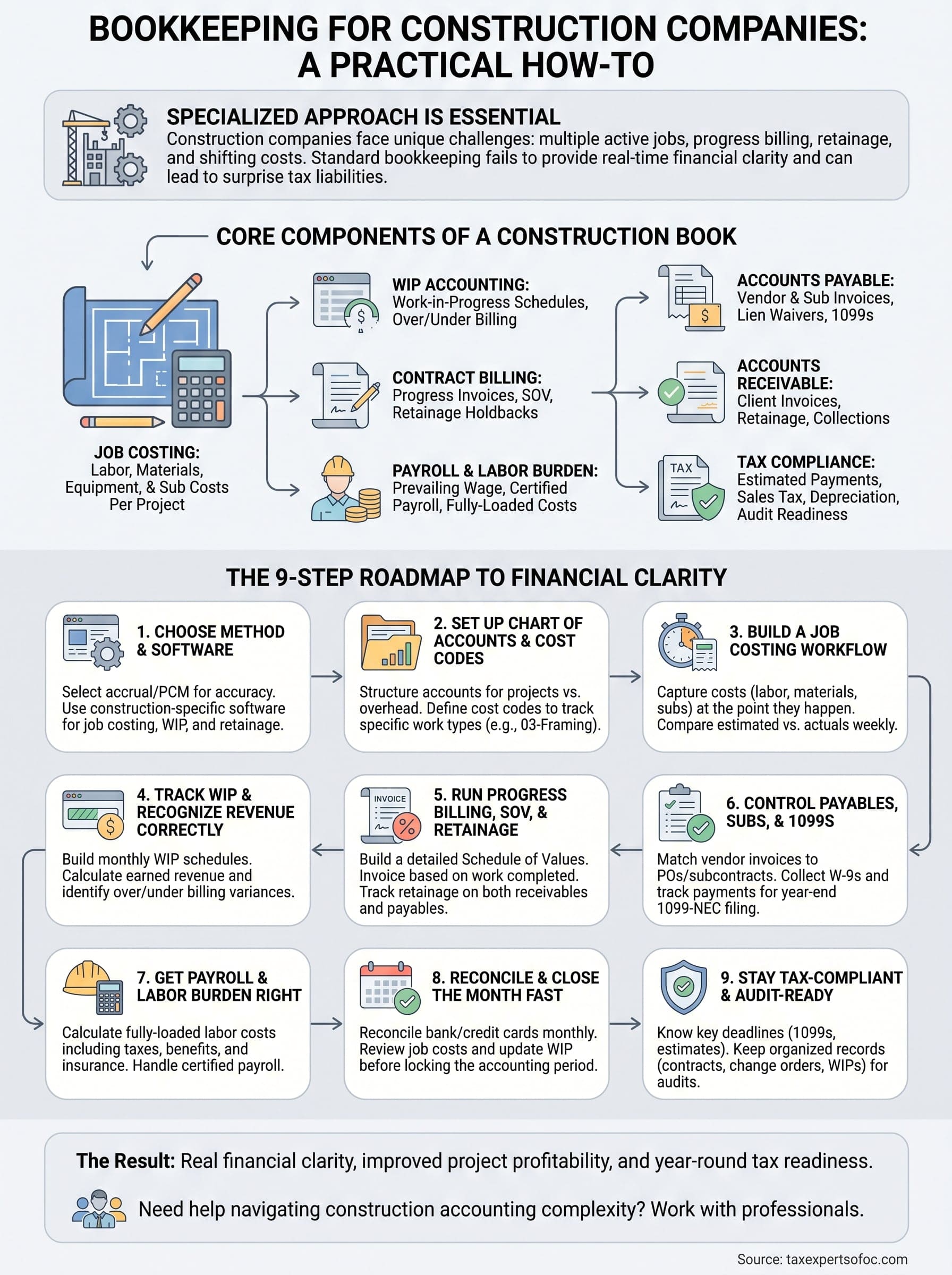

Construction businesses don't operate like typical companies, and their books shouldn't be managed like one either. Between progress billing, retainage holdbacks, and costs that shift from job to job, bookkeeping for construction companies demands a specialized approach. Get it wrong, and you're left guessing at profitability on projects that won't wrap up for months, or worse, you're blindsided by a tax liability you didn't see coming.

The core challenge is that construction accounting tracks money across multiple active jobs, each with its own budget, timeline, and cost structure. Standard bookkeeping methods weren't built for that. You need systems that account for job costing, handle long-term contracts properly, and give you real financial clarity, not just a pile of receipts and a prayer at year-end. This is exactly the kind of complexity our CPAs and Enrolled Agents at Tax Experts of OC help construction business owners sort through every day, from chart of accounts setup to ongoing monthly bookkeeping.

This guide breaks down the specific bookkeeping practices that construction companies need to get right: job costing fundamentals, choosing the right accounting method, managing cash flow across projects, and staying compliant with IRS requirements. Whether you're a general contractor running a crew of five or a specialty sub scaling into new markets, what follows is a practical roadmap you can actually put to work.

What construction bookkeeping includes

Construction bookkeeping covers every financial activity tied to running a contracting business, but its scope goes well beyond what you'd find in a standard retail or service operation. Job-level tracking sits at the core: every dollar of labor, materials, equipment, and subcontractor cost must be linked to a specific project so you know whether that job made money or lost it. That level of detail is what separates bookkeeping for construction companies from general small-business accounting, and it's the foundation everything else is built on.

When you can see the profit or loss on each individual job, you stop guessing and start managing your business with real data.

The core components of a construction book

A full set of construction books covers several distinct areas, each feeding into the overall financial picture. You track project revenues and costs at the job level, manage accounts payable and receivable across multiple clients and vendors, and handle payroll that fluctuates based on crew size, prevailing wage rules, and certified payroll requirements. Each of these areas has its own workflow, and skipping any one of them creates blind spots in your financials.

Here's a breakdown of what a complete construction accounting system tracks:

| Area | What it covers |

|---|---|

| Job costing | Labor, materials, equipment, and sub costs per project |

| Contract billing | Progress invoices, schedule of values (SOV), retainage |

| Accounts payable | Vendor invoices, subcontractor payments, lien waivers |

| Accounts receivable | Client invoices, collections, retainage receivable |

| Payroll | Wages, benefits, payroll taxes, certified payroll reports |

| WIP accounting | Work-in-progress schedules, over/under billing |

| Tax compliance | Estimated payments, 1099s, sales tax on materials, depreciation |

Why construction accounting is more layered than standard bookkeeping

Most businesses record a sale when they invoice and an expense when they pay. Construction doesn't work that cleanly. Long-term contracts can span months or years, which means you need to decide when to recognize revenue: at project completion, or as work progresses over time. Your cash flow position can look healthy on paper while you're actually overbilled on one job and underbilled on three others, a situation that only surfaces when you run a proper work-in-progress schedule.

On top of that, you're often managing retainage, the percentage of each invoice your client holds back until the project reaches completion, typically 5% to 10% of each draw. That money shows up as a receivable on your balance sheet, but you can't collect it for months. You also deal with subcontractor compliance: collecting W-9s before work begins, tracking every payment, and issuing 1099-NEC forms at year-end for any sub paid $600 or more.

Beyond subcontractors, equipment costs add another layer. You need to decide whether to expense a purchase outright, depreciate it over time, or allocate its hourly cost to jobs that use it. Each decision affects both your job-level profitability and your annual tax position. These aren't just accounting technicalities; they directly shape the numbers your lender, bonding company, or general contractor will scrutinize when you bid on larger work.

Step 1. Choose software and an accounting method

The tools and methods you select at the start shape every other part of bookkeeping for construction companies. Getting this foundation right early means fewer corrections later and cleaner data flowing into your tax returns, financial statements, and bonding applications.

Pick your accounting method first

Construction businesses can use cash basis or accrual basis accounting. Cash basis records income when you receive payment and expenses when you pay them. Accrual basis records revenue when earned and expenses when incurred, regardless of when cash changes hands. Most lenders and bonding companies prefer accrual-based financials because they give a more accurate picture of your actual obligations at any point in time.

For long-term contracts, the IRS recognizes two specific methods: percentage of completion (PCM) and completed contract method (CCM). Under PCM, you recognize revenue as the project progresses, calculated by dividing costs incurred to date by total estimated project costs. Under CCM, you defer all revenue and expenses until the contract is substantially complete.

Contractors with average annual gross receipts above $30 million are generally required by the IRS to use the percentage of completion method for long-term contracts.

Smaller contractors can often use CCM, which offers a tax deferral advantage by pushing income recognition out to project completion. That said, CCM can mask real-time job profitability, so running parallel job cost reports alongside your tax method is worth the extra effort.

Choose software built for construction workflows

General accounting software handles basic invoices and expenses, but it won't track job costs, retainage balances, or WIP schedules without heavy customization. Construction-specific platforms give you those features built in, which reduces setup time and cuts the risk of losing project-level financial detail.

When evaluating software, confirm it handles these core functions:

- Job costing tied directly to the general ledger

- Progress billing and SOV invoice templates

- Retainage tracking on both payables and receivables

- Subcontractor compliance management and 1099 preparation

- Certified payroll report generation

Your software choice also affects how easily a CPA or bookkeeper can access and review your books remotely, which matters when tax deadlines arrive and you need fast, accurate answers from a professional.

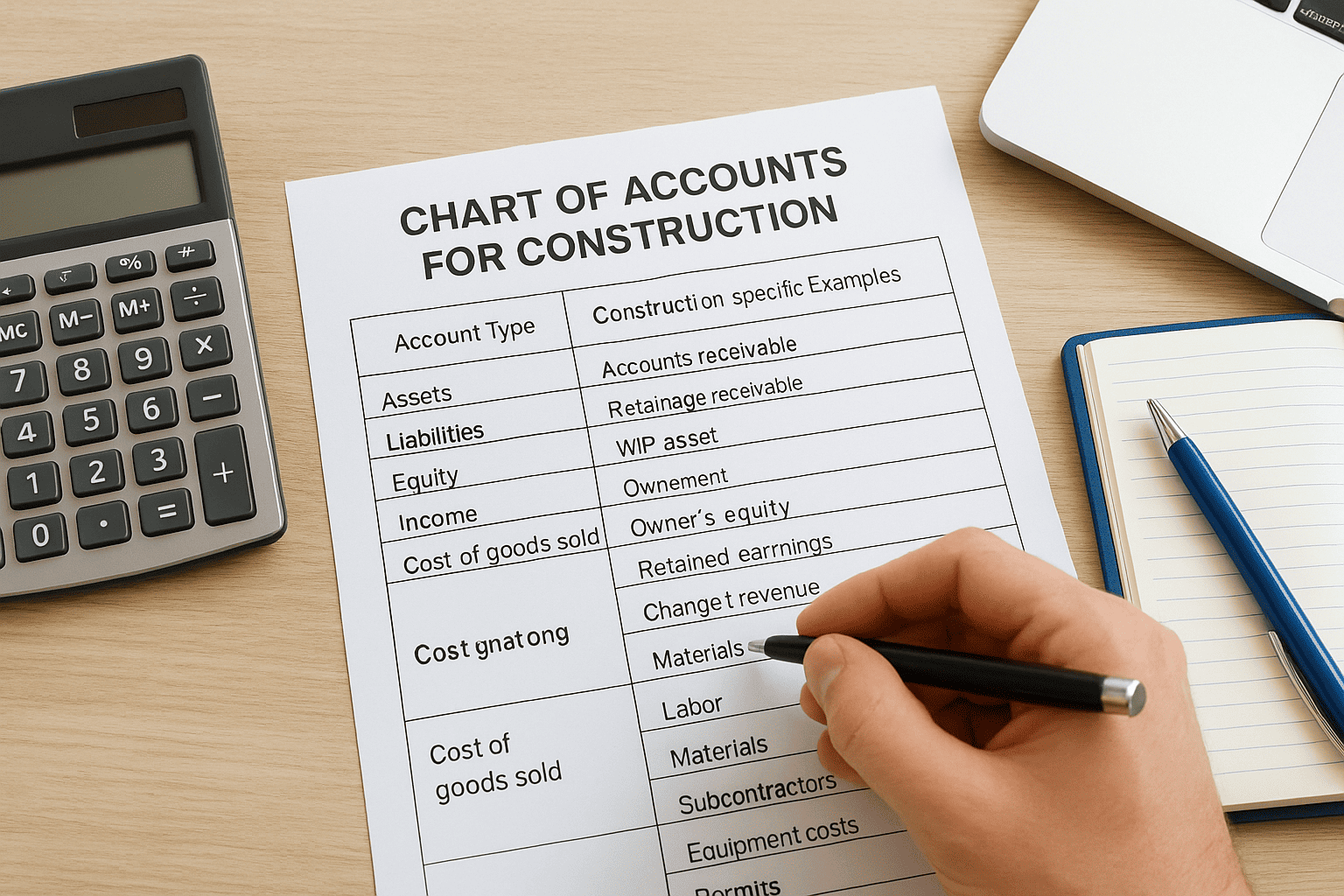

Step 2. Set up your chart of accounts and cost codes

Your chart of accounts is the backbone of every financial report you produce. In bookkeeping for construction companies, a generic chart of accounts pulled from accounting software defaults won't cut it, because it won't reflect the categories your business actually spends and earns money through. You need to build yours around construction-specific line items from the start, before you record a single transaction.

Structure your chart of accounts for construction

A well-structured chart of accounts separates your project-related accounts from your overhead accounts so you can see job margins clearly without mixing in office rent, administrative salaries, or software subscriptions. Start with the standard five account types (assets, liabilities, equity, income, and expenses), then add construction-specific subcategories under each.

Here's a starter framework you can adapt:

| Account type | Construction-specific examples |

|---|---|

| Assets | Accounts receivable, retainage receivable, WIP asset, equipment |

| Liabilities | Accounts payable, retainage payable, payroll liabilities, loan balances |

| Equity | Owner's equity, retained earnings |

| Income | Contract revenue, change order revenue, material sales |

| Cost of goods sold | Labor, materials, subcontractors, equipment costs, permits |

| Overhead expenses | Office rent, insurance, vehicle costs, professional fees |

Keep your COGS accounts strictly separate from overhead expenses. That separation is what lets you calculate true gross profit per job rather than just a blended net number at year-end.

Define your cost codes before the first job starts

Cost codes are the numeric or alphanumeric identifiers you assign to specific types of work or expense within a job. They give you the granularity to compare, for example, framing labor costs across five different projects side by side. Without them, your job costing data becomes too broad to act on.

Set your cost codes before you log the first transaction on any project. Retrofitting codes after the fact wastes time and produces gaps in your historical data.

A basic cost code structure for a general contractor looks like this:

- 01 - Site work and demolition

- 02 - Concrete and foundation

- 03 - Framing and structural

- 04 - Roofing

- 05 - Mechanical, electrical, plumbing (MEP)

- 06 - Finishes and fixtures

- 07 - Subcontractor costs

- 08 - Equipment and rentals

- 09 - Permits and inspections

Match your cost codes to the line items in your bids and contracts so you can compare estimated versus actual costs without translating between two different naming systems at month-end.

Step 3. Build a job costing workflow you can trust

Job costing is the process of tracking every cost on a project and comparing it to what you estimated before work began. A workflow is only as good as the data going into it, so the real challenge in bookkeeping for construction companies isn't understanding the concept; it's building a repeatable system that captures costs accurately and consistently, even when your crew is three sites deep and your inbox is full.

A job that looks profitable from memory and a job that's actually profitable are often two very different things.

Capture costs at the point they happen

The biggest gap in most job costing systems is lag time: costs get recorded days or weeks after they're incurred, which means your running job totals are always behind reality. Fix that by building a workflow where every cost type gets logged at the source, not at month-end cleanup.

Follow this capture process for each cost category:

- Labor: Require field crews to submit daily time logs tied to a specific job and cost code. Use a mobile timesheet app if your crew isn't desk-based.

- Materials: Code every vendor bill to a job and cost code the moment it arrives, before it gets filed or paid.

- Subcontractors: Log the subcontract value when you sign the agreement, then match each invoice against that committed cost when it comes in.

- Equipment: Track usage hours per job and apply a standard internal rate (for example, $85 per hour for a skid steer) so equipment cost shows up in job reports, not just on your asset schedule.

Compare estimated versus actual costs on a set schedule

Capturing costs is only half the workflow. You also need a fixed review cadence where you pull a job cost report and compare actuals to your original estimate line by line. Do this weekly on active jobs, not monthly. By the time a monthly review surfaces a cost overrun, you may have already committed to the next phase of work.

When a line item runs over budget, investigate the cause before the job closes: was the estimate wrong, did scope change, or did execution break down? That answer directly improves your next bid and tightens your overall cost control system over time.

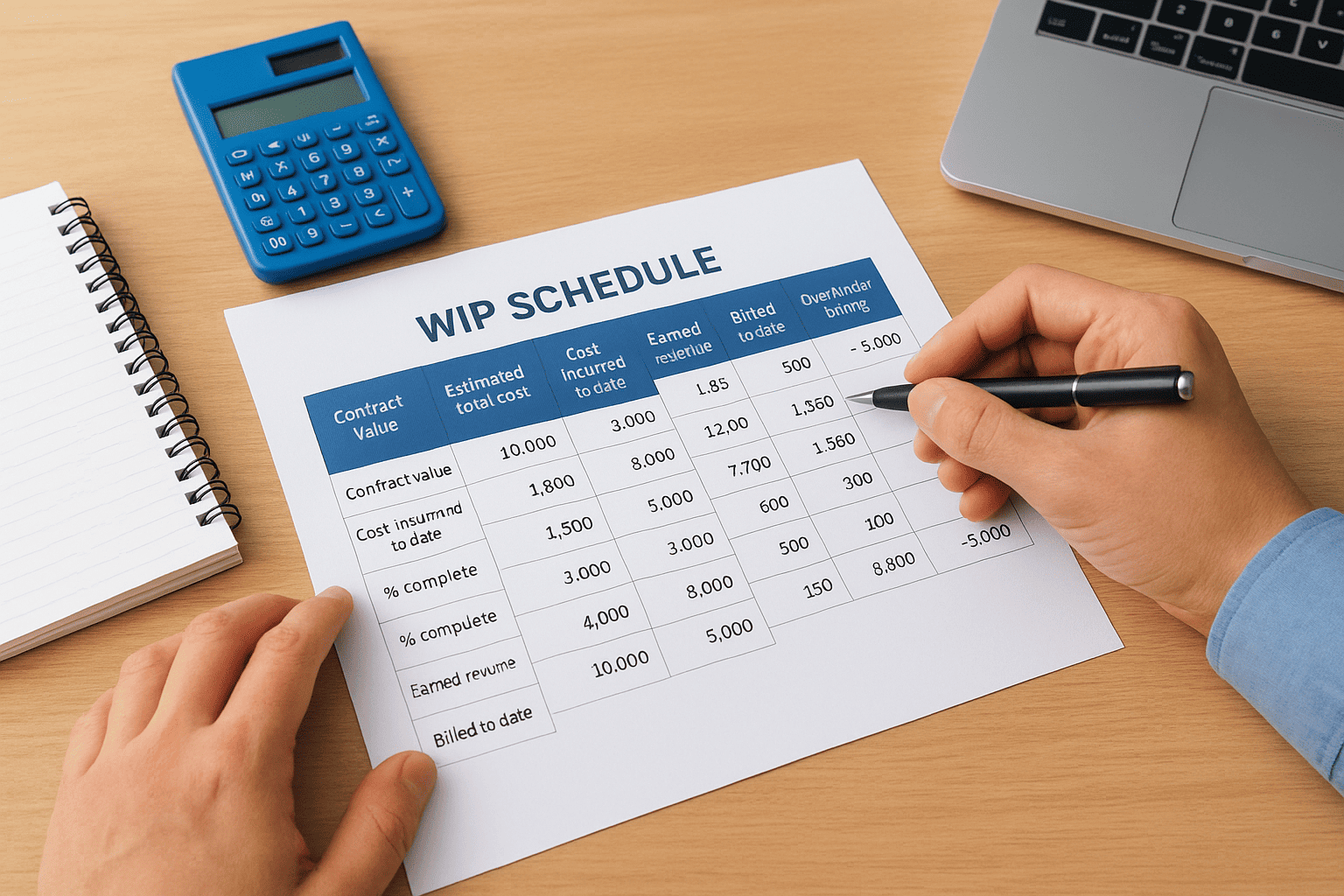

Step 4. Track WIP and recognize revenue correctly

WIP (work-in-progress) accounting is where bookkeeping for construction companies gets technical fast. Your WIP schedule tells you whether you've billed more or less than you've actually earned on each active contract at a given point in time. Without it, your income statement can mislead you: a month where you invoiced heavily looks profitable even if the underlying work is behind schedule and over budget.

Build your WIP schedule monthly

Your WIP schedule needs to pull together four numbers for every active contract: total contract value, costs incurred to date, total estimated costs, and amount billed to date. From those inputs, you calculate two derived figures: earned revenue (costs incurred divided by total estimated costs, multiplied by contract value) and the billing variance (billed to date minus earned revenue).

Use this template as your starting point:

| Column | Description |

|---|---|

| Contract value | Total agreed contract amount including approved change orders |

| Estimated total cost | Your current best estimate of total project cost |

| Cost incurred to date | Actual costs posted to the job through the report date |

| % complete | Cost incurred / estimated total cost |

| Earned revenue | % complete x contract value |

| Billed to date | Total invoices issued to the client |

| Over/under billing | Billed to date minus earned revenue |

A positive variance means you've billed more than you've earned (overbilling); a negative variance means you've earned more than you've billed (underbilling), and both carry real financial consequences.

Spot overbilling and underbilling before they compound

Overbilling might look like a cash flow win in the short term, but it creates a liability on your balance sheet: money you've collected for work you haven't completed yet. If that job stalls or runs over budget, you'll face a situation where you owe your client work that your cash has already funded.

Underbilling is equally damaging. It means you've performed work you haven't invoiced for, which understates your revenue and can trigger a cash shortfall when payroll and vendor payments come due. Review your WIP report at every month-end and flag any job where the billing variance exceeds 5% of contract value in either direction so you can correct the next billing cycle before the gap widens.

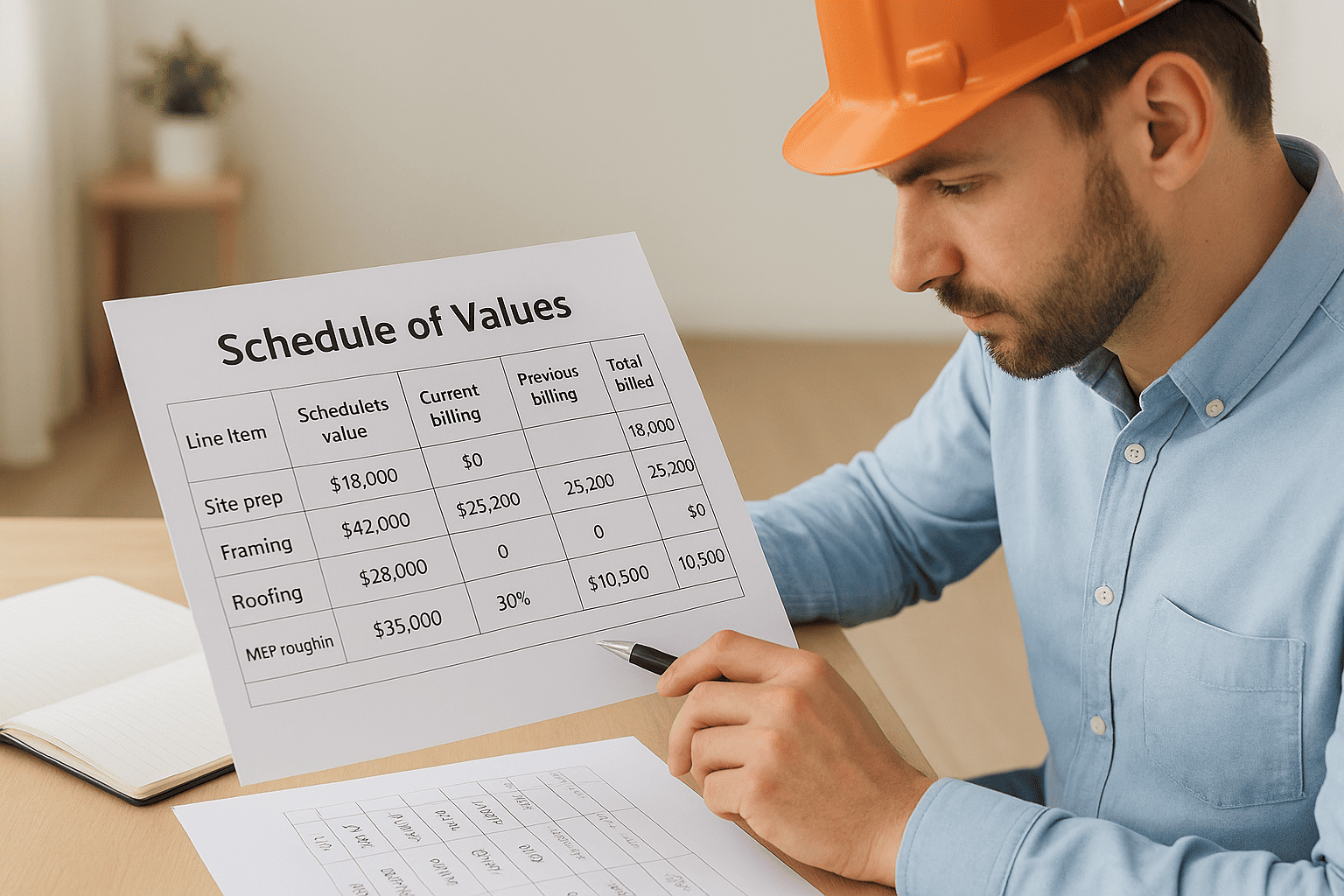

Step 5. Run progress billing, SOV, and retainage

Progress billing is the invoicing backbone of bookkeeping for construction companies. Rather than sending one lump invoice at project completion, you invoice your client at regular intervals based on how much work you've completed. Each draw ties back to a schedule of values (SOV), which breaks the total contract into line items and assigns a dollar amount to each one. Your client approves each draw against that SOV, so the setup needs to be detailed and defensible from day one.

Build your schedule of values before the first invoice

Your SOV functions as a shared language between you and your client for the entire life of the contract. Build it during preconstruction by breaking the contract value into discrete scope items that align with your cost codes and bid line items. Avoid grouping too many activities into a single line, because vague SOV entries invite disputes when you submit a progress draw.

A basic SOV structure looks like this:

| Line item | Scheduled value | % complete | Current billing | Previous billing | Total billed |

|---|---|---|---|---|---|

| Site prep | $18,000 | 100% | $0 | $18,000 | $18,000 |

| Framing | $42,000 | 60% | $25,200 | $0 | $25,200 |

| Roofing | $28,000 | 0% | $0 | $0 | $0 |

| MEP rough-in | $35,000 | 30% | $10,500 | $0 | $10,500 |

Update percentage-complete figures based on actual work performed, not on how much you'd like to bill that month.

Handle retainage on both sides of the ledger

Retainage affects your cash flow and your balance sheet at the same time, so you need to track it with precision. When your client holds back 5% to 10% of each draw, record that amount as retainage receivable on your balance sheet rather than reducing the invoice total. It's money you've earned; you just can't collect it yet.

Apply the same logic when you hold retainage from subcontractors. Record those amounts as retainage payable, and release them only after your client releases yours and the sub's scope passes final inspection. Keeping both sides of retainage on your balance sheet gives you an accurate picture of what you're owed and what you owe, so you're not caught short when release requests arrive.

Step 6. Control payables, subs, and 1099s

Accounts payable management in bookkeeping for construction companies runs deeper than just paying bills on time. Every vendor invoice and subcontractor payment needs to be coded to the right job and cost code, matched against an approved purchase order or subcontract, and filed in a way that supports lien waiver documentation and year-end 1099 reporting. Skipping any of those steps creates downstream problems that are expensive and time-consuming to fix.

Build a payables workflow around job coding and approvals

Before you pay any vendor invoice, confirm it matches a purchase order or approved subcontract, then code it to the correct job and cost code in your accounting system. This two-step verify-then-code process keeps your job cost reports accurate and prevents unauthorized charges from slipping through. Set a clear approval threshold: anything above, for example, $2,500 requires a project manager sign-off before payment is released.

Paying an invoice without matching it to an approved document first is how job cost overruns stay invisible until it's too late to address them.

For subcontractors specifically, collect a signed W-9 before the first check goes out and hold payment until you have it. No exceptions. That discipline saves you significant scrambling in January when 1099 deadlines arrive and you're hunting down tax ID numbers from subs who have long since moved on to the next job.

Track 1099 obligations from day one

The IRS requires you to file a 1099-NEC for any subcontractor or unincorporated vendor paid $600 or more during the tax year. Running a last-minute report in January to find out who qualifies is avoidable if you build your vendor records correctly from the start.

Use this setup template when you add a new vendor or subcontractor to your system:

| Field | What to capture |

|---|---|

| Legal business name | Must match exactly what's on their W-9 |

| Tax ID (EIN or SSN) | Required for 1099 filing |

| Entity type | Sole prop, partnership, LLC, or corporation |

| 1099 required | Yes or No based on entity type and payments |

| YTD payments | Running total updated with each payment |

Track year-to-date payment totals throughout the year so you never reach January surprised by who crossed the $600 threshold. Corporations are generally exempt from 1099 reporting, but LLCs taxed as sole proprietors or partnerships are not, so confirming entity type upfront removes guesswork at filing time.

Step 7. Get construction payroll and labor burden right

Payroll is the largest cost on most construction jobs, and it's also the most misrepresented in bookkeeping for construction companies. Many contractors track only gross wages per employee, then wonder why their job cost reports show a profit that their bank account doesn't reflect. The gap is almost always labor burden: the additional employer costs layered on top of every dollar of wages you pay.

Calculate full labor burden, not just wages

Your true labor cost per employee includes far more than their hourly rate. Once you add employer payroll taxes, workers' compensation premiums, general liability insurance allocated to labor, health benefits, and any union or apprenticeship contributions, the real cost of a $30-per-hour carpenter often runs between $42 and $50 per hour. If your job cost reports use the $30 wage figure, every labor-intensive job is understated from the start.

Build your labor burden rate before the job starts, not after you've already priced the work.

Use this template to calculate a fully-loaded labor burden rate for each employee class:

| Cost component | Example amount | Notes |

|---|---|---|

| Base wage | $30.00/hr | Confirmed rate |

| FICA (employer share) | $2.30/hr | 7.65% of wages |

| FUTA / SUTA | $0.42/hr | Varies by state |

| Workers' comp premium | $3.60/hr | Rate varies by trade classification |

| General liability (labor %) | $1.20/hr | Allocated portion |

| Health benefits | $2.10/hr | Monthly premium divided by hours |

| Total labor burden rate | $39.62/hr | Use this figure in job cost reports |

Apply this fully-loaded rate when you enter labor costs into your job costing system, so your project margins reflect what you actually spend.

Handle certified payroll and multi-state compliance

If you work on prevailing wage projects funded by federal, state, or local government, you're required to submit certified payroll reports, typically using U.S. Department of Labor Form WH-347. These reports document each worker's name, trade classification, hours worked, and wages paid, and they must match your payroll records exactly. Discrepancies trigger audits and can cost you future bids on public work contracts.

When your crew crosses state lines, confirm each state's payroll tax registration requirements before work begins. Running payroll in a new state without registering first creates penalty exposure that your job margin won't absorb.

Step 8. Reconcile accounts and close the month fast

Monthly reconciliation in bookkeeping for construction companies is what separates clean, usable books from a year-end scramble. Your goal is to close each month within five to seven business days of month-end so your job cost reports and financial statements reflect current reality, not numbers that are already three weeks stale by the time you review them.

Reconcile bank accounts and credit cards first

Start your close by pulling your bank and credit card statements and matching every transaction to what's recorded in your accounting system. Any transaction in the bank feed that isn't coded to a job and cost code is a gap in your job costing data, and it needs a home before you move forward. Flag unmatched items immediately rather than letting them collect in a suspense account.

Run this reconciliation sequence every month without exception:

- Match your bank statement ending balance to your general ledger cash account

- Clear all outstanding checks older than 60 days and investigate any that haven't cleared

- Confirm credit card statement totals match your recorded liability balance

- Verify payroll tax deposits appear in both your bank feed and your payroll liability accounts

If your bank balance and your general ledger balance don't agree before you close the month, nothing else in your financials will be reliable.

Check job cost totals and WIP before you lock the period

After bank reconciliation, pull a job cost report for every active project and confirm that all labor, materials, subcontractor invoices, and equipment charges posted during the month are coded to the correct job and cost code. A misrouted cost means your profitability numbers are wrong in two places simultaneously: the general ledger and the job report.

Once job costs look clean, update your WIP schedule with the latest percentage-complete figures and recalculate earned revenue for each active contract. Lock the accounting period only after your WIP schedule, your income statement, and your job cost reports all tell the same story. Build a written monthly close checklist and run through it in the same order every month so nothing gets skipped when deadlines pile up.

Step 9. Stay tax-compliant and audit-ready year-round

Tax compliance in bookkeeping for construction companies isn't a once-a-year sprint before April. It's a continuous process built into your monthly close, your vendor management, and your payroll workflow. The construction industry draws more IRS scrutiny than most sectors because of its cash-intensive operations, subcontractor relationships, and the complexity of long-term contract reporting. If your records aren't organized year-round, you'll spend more time and money responding to notices than you would have spent maintaining clean books in the first place.

Know your key tax deadlines and obligations

Your annual tax calendar needs to account for multiple filing types, not just your income tax return. Missing a payroll deposit deadline or a 1099 due date can trigger penalties before your CPA even sees your year-end books. Build this calendar into your accounting workflow so each deadline gets treated as a hard due date, not a suggestion.

Missing a single quarterly estimated payment can trigger an underpayment penalty even if you pay your full balance in April.

Track these obligations every year:

| Deadline | Obligation |

|---|---|

| January 31 | 1099-NEC filed and distributed to subs |

| January 31 | W-2s distributed to employees |

| March 15 | S-Corp and partnership returns (Form 1120-S / 1065) |

| April 15 | Individual and C-Corp returns, Q1 estimated tax payment |

| June 16 | Q2 estimated tax payment |

| September 15 | Q3 estimated tax payment, extended partnership and S-Corp returns |

| October 15 | Extended individual returns |

| December 31 | Year-end equipment purchases for Section 179 or bonus depreciation |

Keep your records audit-ready all year

Audit readiness means your documentation supports every number on your return without requiring a reconstruction project. For each job, retain your original contract, all change orders, progress billing records, lien waivers, and subcontractor agreements in a single organized folder, physical or digital. The IRS can audit returns up to three years back under normal circumstances and six years if they suspect a substantial understatement of income.

Your audit file for each tax year should include bank statements, payroll tax filings, depreciation schedules, equipment purchase receipts, and your WIP schedules from each month-end close. Review these records quarterly rather than waiting until an audit notice forces the issue.

Wrap-Up and Next Steps

The nine steps in this guide give you a working framework for bookkeeping for construction companies that goes well beyond basic record-keeping. You now have a system for job costing, WIP tracking, progress billing, subcontractor compliance, payroll burden, monthly close, and year-round tax readiness. Each piece connects to the next: clean job costs feed accurate WIP schedules, accurate WIP schedules support defensible progress billing, and solid billing records keep you audit-ready without the last-minute scramble.

Putting all of this in place takes time, and running it correctly while managing active projects takes consistent discipline. If your books are behind, your job costs are mixed together, or IRS notices have started arriving, the right move is to work with a professional who understands construction accounting. The team at Tax Experts of OC includes CPAs and Enrolled Agents who help contractors clean up their books, resolve tax issues, and build financial systems that actually hold up.