Law firms operate under financial rules that most businesses never have to think about. Bookkeeping for law firms isn't just about tracking income and expenses, it requires strict separation of client funds, compliance with state bar regulations, and an accounting structure that can withstand scrutiny from both the IRS and your state's disciplinary board.

Get it wrong, and the consequences go beyond a tax penalty. Mishandling an IOLTA account or commingling client trust funds with operating money can result in disbarment, malpractice claims, and personal liability. Yet many attorneys either manage their own books without proper training or hire general bookkeepers who don't understand the unique compliance obligations that come with legal practice.

This guide breaks down everything you need to know: how trust and IOLTA accounting actually work, which bookkeeping methods and software fit a law firm's needs, and the best practices that keep you compliant and audit-ready. Whether you're a solo practitioner or managing a growing firm, you'll walk away with a clear framework for organizing your finances the right way.

At Tax Experts of OC, our CPAs and Enrolled Agents work with professionals across industries, including attorneys, to handle bookkeeping, tax preparation, and financial compliance at every level. If you'd rather hand this off to someone who understands the stakes, we're here for that conversation too.

What makes law firm bookkeeping different

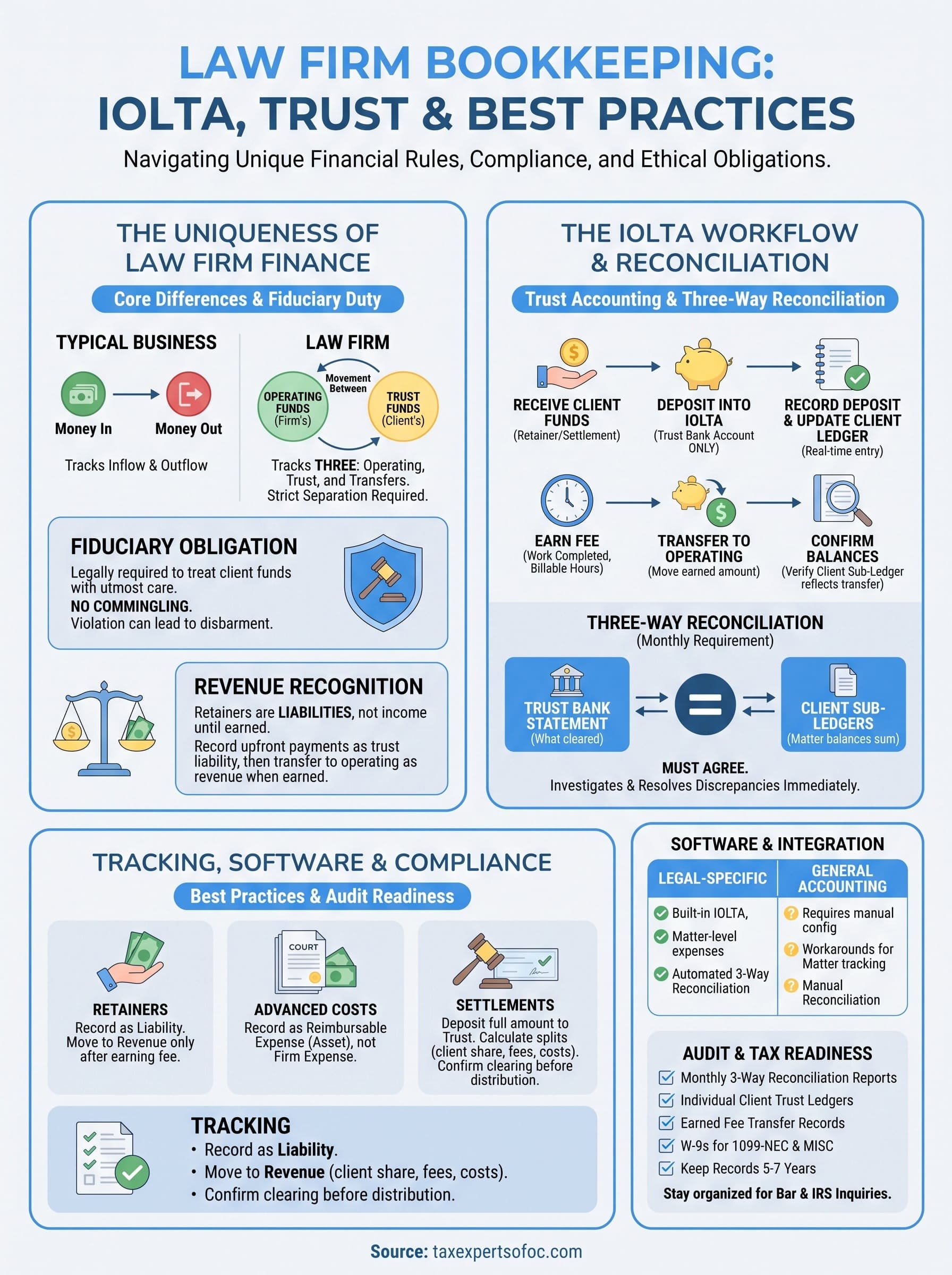

Most businesses track two things: money coming in and money going out. Law firms track three: their own operating funds, client trust funds, and the movement between the two. That third category is where most compliance problems start. When a client pays a retainer, that money doesn't belong to the firm yet. It sits in a separate trust account until the firm earns it, and every dollar must be accounted for precisely from the moment it arrives to the moment it transfers out.

The fiduciary obligation that changes everything

Attorneys hold a fiduciary duty to their clients, which means they are legally and ethically required to treat client funds with the same care they would apply to their own. This isn't a suggestion from the accounting industry. Every state bar in the country enforces trust accounting rules, and a violation can trigger disciplinary proceedings, suspension, or disbarment. Standard bookkeeping software and general accounting practices were not designed with this obligation in mind, which is why bookkeeping for law firms requires a different setup from the start.

Commingling client funds with your firm's operating account, even accidentally, is one of the most serious ethics violations a practicing attorney can commit.

Your firm's record-keeping standards must be higher than those of a typical small business. You need to show, at any point in time, exactly how much of each client's money sits in trust, when fees were earned and transferred out, and what the running balance looks like. A general ledger handles your firm's finances. Trust accounting handles someone else's money that you are holding on their behalf, which is an entirely different responsibility.

Revenue recognition works differently in legal practice

Unlike a product business that records revenue at the point of sale, a law firm often receives payment before completing any work. A $10,000 retainer collected upfront is a liability, not income. You record it as such in your books and only move it to your operating account after completing billable work and drawing it down against the balance. Contingency fee arrangements add another layer of complexity because income doesn't appear in your books at all until a case settles or a judgment gets paid.

Fixed-fee arrangements, hourly billing, and hybrid models each require different tracking logic. Your bookkeeping system needs to handle all of them without mixing up which dollars belong to the client and which ones belong to the firm.

State bar oversight adds a second layer of scrutiny

Your firm answers to the IRS on tax matters, but it also answers to your state's disciplinary authority on trust accounting matters. These two bodies operate independently and have different requirements. The IRS wants accurate income reporting. Your state bar wants to see that client money was handled ethically and in accordance with specific procedural rules, which often include monthly reconciliations, individual client ledgers, and proper handling of IOLTA interest.

Many states require firms to complete a three-way reconciliation each month, comparing the trust account bank statement, the trust ledger, and the individual client sub-ledgers so all three figures agree. This is a standard requirement that most industries never encounter. If your books don't support that process, you're already exposed before any audit or bar inquiry begins.

Set up the right bank accounts and chart of accounts

Your financial structure is the foundation that everything else in bookkeeping for law firms rests on. Before you process a single payment or record a billable hour, you need the right bank accounts in place and a chart of accounts that reflects how legal money actually moves. Most general small business setups lack the categories required to track client funds separately from firm revenue, which means you're either rebuilding later or patching problems as they surface.

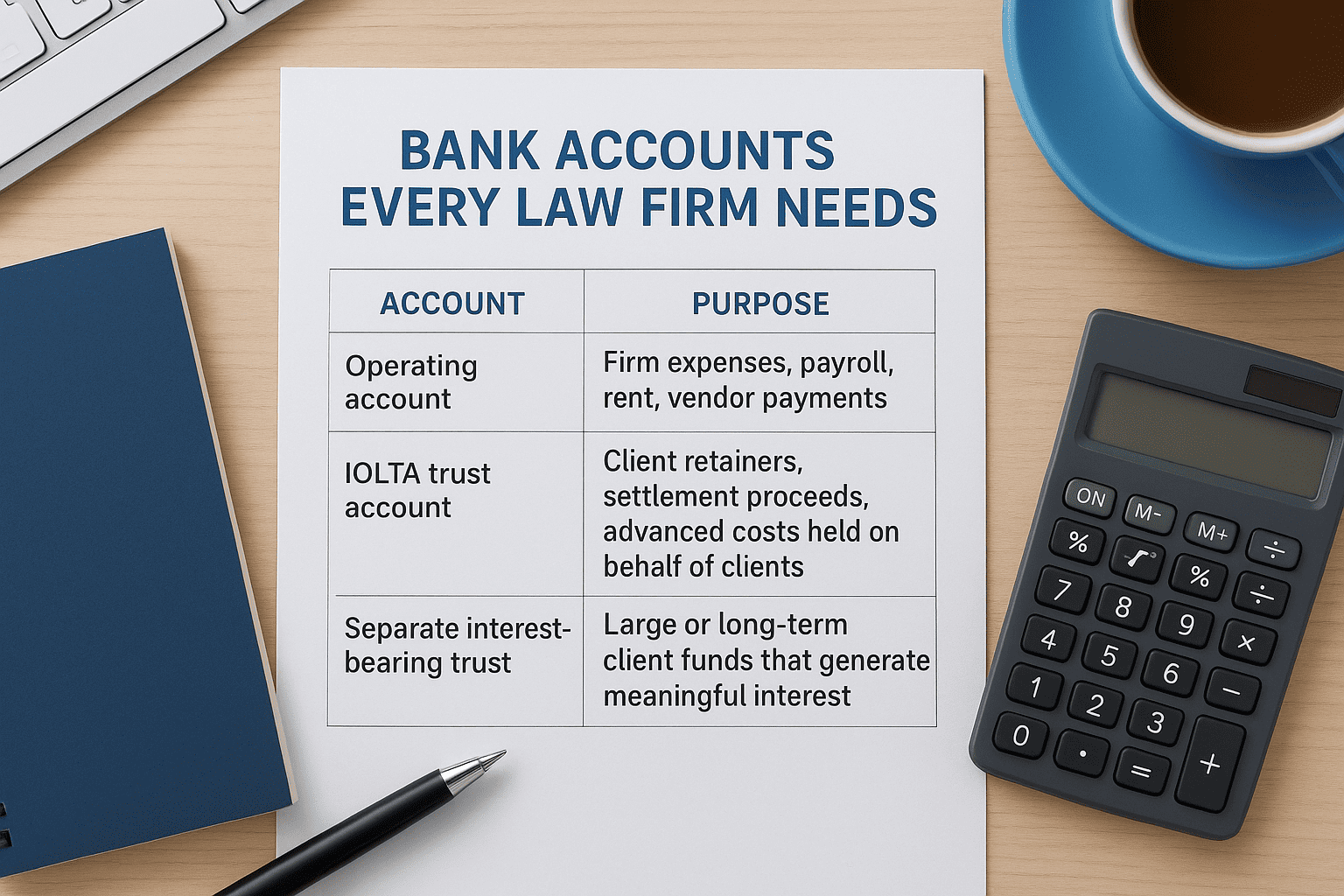

The bank accounts every law firm needs

Your firm requires at least three separate bank accounts operating at all times. Mixing any of these together creates compliance exposure that no amount of cleanup can fully resolve retroactively.

| Account | Purpose | Who owns the funds |

|---|---|---|

| Operating account | Firm expenses, payroll, rent, vendor payments | The firm |

| IOLTA trust account | Client retainers, settlement proceeds, advanced costs held on behalf of clients | The client |

| Separate interest-bearing trust | Large or long-term client funds that generate meaningful interest | The client |

Never deposit earned fees directly into your trust account and never pay firm expenses from it. Every dollar that touches trust has to be traceable to a specific client matter.

You should also maintain a dedicated payroll account if you have employees. Running payroll through your main operating account works, but a separate account makes tax deposits, reconciliation, and employee tax compliance significantly cleaner.

Build your chart of accounts around trust obligations

Your chart of accounts needs categories that standard small business templates don't include. Start by adding trust liability accounts for each client matter that has funds in trust. When a client sends a retainer, you debit your trust bank account and credit that client's trust liability account. When you earn fees and transfer them out, you reverse the liability and record the revenue.

A basic law firm chart of accounts should include:

- Operating bank account (asset)

- IOLTA trust bank account (asset)

- Client trust liability (broken out by matter)

- Accounts receivable for billed but unpaid fees

- Unearned retainer income for flat-fee arrangements not yet completed

- Cost recovery income for reimbursable expenses

- General and administrative expenses for rent, software, and overhead

- Professional fees for outside services

Set these up before your first client payment arrives. Retrofitting your chart of accounts after months of transactions is time-consuming and introduces errors that can follow you into tax season and bar audits.

Build a trust accounting workflow for IOLTA

An IOLTA (Interest on Lawyers' Trust Accounts) account holds client funds that are too small or short-term to justify a separate interest-bearing account for that individual client. The interest generated goes to your state's bar foundation, not to you or your client, which is why proper tracking and documentation matter from the moment money enters the account. Without a defined workflow, trust accounting becomes reactive, and reactive trust accounting is where bar complaints start.

Record every transaction as it happens

Your IOLTA workflow needs to run in real time, not at the end of the month. Every deposit and every disbursement requires a corresponding entry in both your trust bank register and the individual client ledger the same day it occurs. Waiting to record transactions creates gaps that are difficult to explain during a bar audit.

Follow this sequence for every IOLTA transaction:

- Receive client funds - Deposit into the IOLTA account only, never the operating account.

- Record the deposit - Enter the amount, date, client name, and matter number in your trust ledger.

- Update the client sub-ledger - Add the deposit to that specific client's running balance.

- Earn the fee - Once work is completed and the fee is earned, prepare a disbursement record.

- Transfer earned funds - Move the amount from IOLTA to your operating account and record the transfer in both ledgers.

- Confirm balances - Verify that the client sub-ledger reflects the transfer before closing the entry.

Never transfer funds from your IOLTA account to cover operating expenses before you have completed the work that earns those fees.

Maintain individual client ledgers for every active matter

Each matter with funds in trust needs its own dedicated ledger, separate from every other client. This is a non-negotiable requirement in bookkeeping for law firms, and most state bars will ask to see these ledgers if they open an inquiry. Your ledger for each matter should show the opening balance, every deposit with the source and date, every disbursement with the recipient and reason, and the running balance after each transaction.

A simple client trust ledger template looks like this:

| Date | Description | Deposit | Disbursement | Balance |

|---|---|---|---|---|

| 2026-01-05 | Retainer received | $5,000.00 | $5,000.00 | |

| 2026-01-20 | Earned fees transferred | $2,000.00 | $3,000.00 | |

| 2026-02-10 | Court filing costs paid | $400.00 | $2,600.00 |

Keep these ledgers current and accessible at all times so you can produce them on short notice without scrambling through months of disorganized records.

Track retainers, advanced costs, and settlements correctly

Three categories of money create the most confusion in bookkeeping for law firms: retainers collected before work begins, costs you advance on a client's behalf, and settlement funds that arrive as a lump sum. Each one follows a different recording path, and treating any of them like ordinary business income will produce inaccurate books and potential bar compliance issues. Getting these right from the start saves you from unwinding months of incorrect entries later.

Handle retainers without recording them as income too early

A retainer is a deposit against future services, not revenue. When a client pays you $8,000 upfront, that money goes into your IOLTA account and gets recorded as a liability on your books until you earn it. Only after you complete billable work, document the hours or fees against the matter, and issue a fee transfer notice do you move the earned portion from trust to your operating account and recognize it as income.

Use this recording pattern for every retainer:

- Deposit received: Debit IOLTA trust bank account, credit client trust liability

- Fee earned: Debit client trust liability, credit operating bank account

- Revenue recognized: Record fee income in your operating ledger

Never skip the trust liability step, even if the retainer is small. The sequence protects both your books and your bar standing.

Record advanced costs as reimbursable expenses

When you pay a court filing fee, expert witness deposit, or process server charge on a client's behalf, that money is not a firm expense. It is a reimbursable cost that the client owes you. Record it in a cost recovery or client advances account rather than lumping it into your general operating expenses. When the client reimburses you, clear that receivable and record the incoming payment against the same account, not as new income.

Treating client cost advances as firm expenses will overstate your deductible costs and understate your taxable income, which creates problems during both a bar audit and an IRS review.

Process settlement funds carefully before any distribution

Settlement proceeds are the highest-risk category for trust accounting errors. When a settlement check arrives, deposit the full amount into your IOLTA account, not your operating account. Then calculate exactly how the funds split between the client's share, your earned fees, and any outstanding costs. Document each disbursement in the client's ledger before you transfer anything. Only move your fees out after you have confirmed the full deposit has cleared and all disbursements are recorded.

Keep billing, time, and expenses tied to matters

When your billing records, time logs, and expense entries all flow through a matter-centric system, you gain complete visibility into each case's financial activity. This connection matters because bookkeeping for law firms depends on knowing exactly what was billed, collected, and spent on each client file, not just across the firm as a whole. Without that link, your financial reports show aggregate numbers that obscure write-offs, unpaid invoices, and cost overruns until they become serious problems.

Capture time entries at the matter level

Every billable hour needs a matter number attached before it leaves your time-tracking tool. A time entry without a matter code is just a number floating in your system with no client, no invoice, and no way to reconcile against a retainer balance. When you record time, include the date, timekeeper name, matter number, task description, and hours spent. Most legal billing software provides a structured field for each of these, and you should use all of them, every time.

Here is a standard billable time entry format:

| Field | Example |

|---|---|

| Date | 2026-07-01 |

| Timekeeper | Sarah M. (Associate) |

| Matter Number | 2026-042 |

| Task Code | L120 - Analysis |

| Description | Reviewed discovery documents and prepared summary memo |

| Hours | 2.50 |

| Rate | $300/hr |

| Amount | $750.00 |

Incomplete time entries are one of the leading causes of billing disputes and revenue leakage in law firms.

Record every expense directly to the responsible matter

When your firm pays a court fee, deposition cost, or expert witness retainer, log it against the specific matter the same day you pay it. Doing so keeps your cost recovery accounts accurate and makes it straightforward to bill the client for reimbursable costs when the invoice goes out. For internal overhead costs like office supplies or software subscriptions, use general overhead categories rather than client matter codes so your cost reports stay clean and your client billing stays defensible.

Follow this three-field rule for every expense entry:

- Matter number - links the cost to the right client file

- Expense category - separates reimbursable costs from overhead

- Payment method and date - creates an audit trail for reconciliation

Connecting billing, time, and expenses at the matter level means your invoices reflect reality and your financial reports show which matters generate profit and which ones do not.

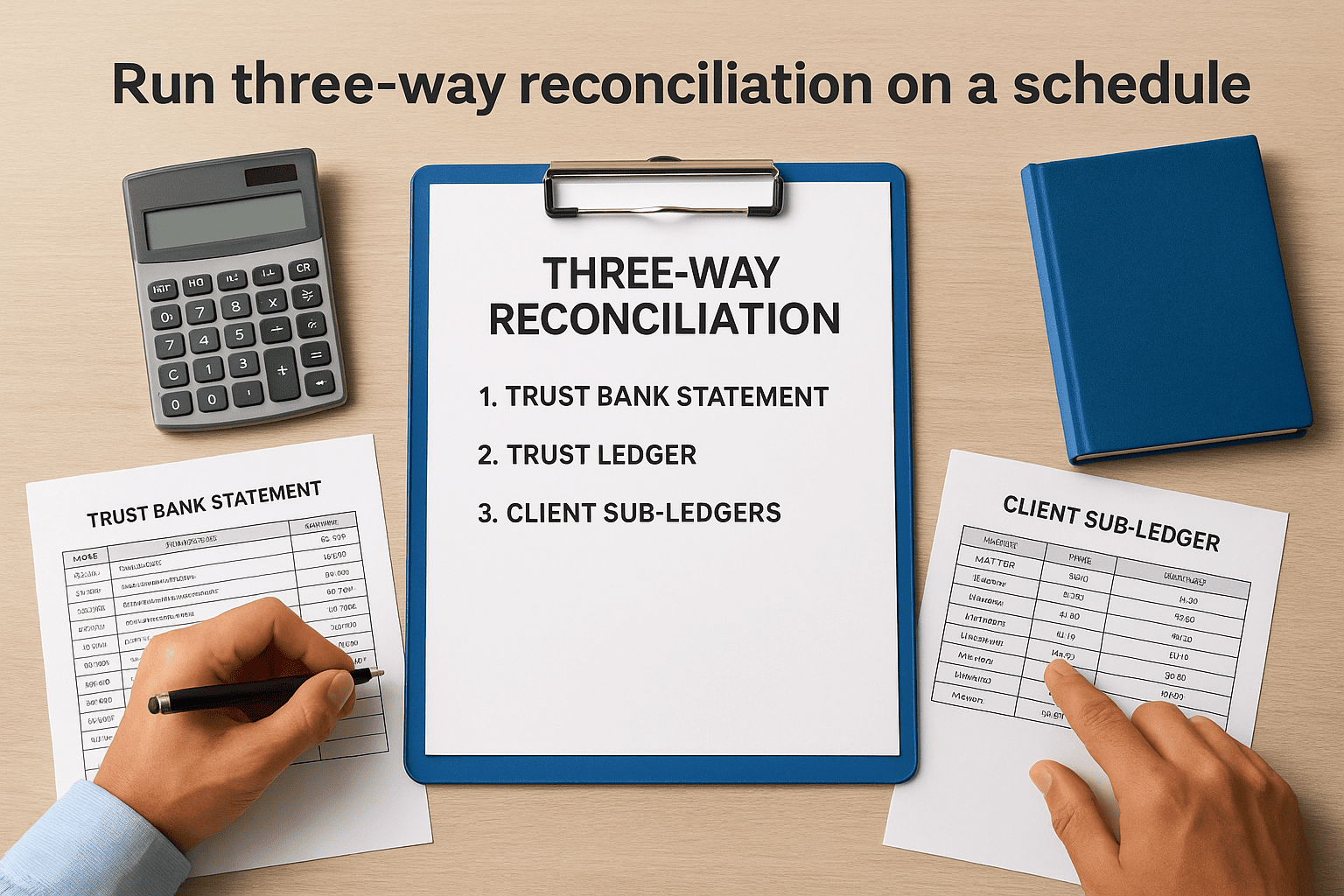

Run three-way reconciliation on a schedule

Three-way reconciliation is the core verification process in bookkeeping for law firms, and most state bars require you to complete it every month. The process compares three separate records, your trust bank statement, your trust ledger, and your individual client sub-ledgers, and confirms that all three show the same total balance for the same period. If the numbers don't match, you have an error somewhere that needs to be found and corrected before you close the month.

A single unresolved discrepancy in your trust account can trigger a bar inquiry, so never carry a difference forward to the next month without investigating it first.

Understand what each record represents

Each of the three records in a reconciliation serves a different purpose, and understanding that difference helps you pinpoint where an error originated when one appears.

| Record | What it shows | Who produces it |

|---|---|---|

| Trust bank statement | All deposits and withdrawals processed by the bank | Your bank |

| Trust ledger | All trust transactions recorded in your accounting system | Your bookkeeper or firm |

| Client sub-ledgers | Running balances for each individual matter in trust | Your bookkeeper or firm |

Your trust bank statement reflects what actually cleared. Your trust ledger reflects what you recorded. Your client sub-ledgers show how the total trust balance breaks down by matter. All three must agree.

Follow a consistent reconciliation process each month

Run your reconciliation within five business days of receiving your monthly bank statement. Doing it on a fixed schedule prevents backlogs and keeps your records current enough to catch errors while the underlying transactions are still recent.

Use this sequence every month:

- Pull your trust bank statement and confirm the closing balance.

- Compare it to your trust ledger and note any differences.

- Add up all client sub-ledger balances and confirm they equal the trust ledger total.

- Identify and resolve discrepancies before marking the reconciliation complete.

- Document the completed reconciliation with the date, the closing balance, and your signature or initials.

When your bank statement balance, your trust ledger total, and the sum of all client sub-ledgers match, your reconciliation is complete. Keep a printed or saved copy of each completed reconciliation for a minimum of five years, as many state bars require records going back that far during disciplinary investigations.

Close the books each month without chaos

Closing your books each month is less about a single task and more about running through a predictable sequence on a consistent schedule. In bookkeeping for law firms, skipping or delaying your monthly close creates a compounding problem: errors from one period bleed into the next, reconciliations become harder, and by the time you sit down for taxes, you're reconstructing months of activity rather than reviewing clean records.

Follow a fixed monthly closing checklist

A monthly close works best when you treat it as a checklist rather than a judgment call about what feels done. Every step should happen in the same order, every month, so nothing gets skipped because it seemed minor in the moment. Complete your three-way trust reconciliation first since it surfaces the most consequential errors, then work through your operating accounts.

Use this monthly closing checklist:

- Reconcile the IOLTA trust account against your trust ledger and all client sub-ledgers

- Reconcile your operating bank account against your general ledger

- Reconcile your payroll account if you run payroll through a separate account

- Review accounts receivable and flag any invoices past 30 days

- Confirm all earned fee transfers from trust to operating are recorded correctly

- Categorize any uncategorized transactions before closing the period

- Run a profit and loss report and review it for obvious anomalies

- Lock the accounting period in your software to prevent backdated entries

Locking the period is a step many firms skip, but it protects your records from accidental changes that can invalidate a reconciliation you already completed.

Catch and correct errors before they compound

When you find a discrepancy during your monthly close, investigate it the same day rather than flagging it for later. An unresolved difference between your bank statement and your trust ledger does not fix itself. The longer you wait, the harder it becomes to identify whether the error came from a missing deposit, a duplicate entry, or a misfiled client transaction that needs to be corrected across multiple ledgers.

Build a simple error log where you record each discrepancy found, the suspected cause, and the date it was resolved. This log serves as both a reference for future months and documentation that your firm actively monitors its own books.

Stay ready for audits, taxes, and 1099s

Bookkeeping for law firms runs on two parallel compliance tracks: your state bar's trust accounting requirements and the IRS's tax reporting obligations. Both can show up unannounced, and neither accepts "we'll clean it up later" as a response. If your books are current, organized, and reconciled, responding to an audit or preparing annual tax returns becomes a documentation task rather than a crisis.

Know your 1099 obligations

Law firms issue Form 1099-NEC to any individual or unincorporated business paid $600 or more for services during the calendar year, including expert witnesses, contract paralegals, and freelance investigators. You also issue Form 1099-MISC for certain attorney payments, particularly when your firm distributes settlement proceeds to a plaintiff. Many firms miss these because the payments flow through trust accounts and get overlooked when 1099 season arrives.

Track every vendor and contractor payment throughout the year so you're not reconstructing payee information in January under deadline pressure.

Use this 1099 readiness checklist throughout the year:

- Collect Form W-9 from every vendor before issuing their first payment

- Flag all payments to non-corporate individuals in your chart of accounts

- Review your trust disbursements for any qualifying attorney or settlement payments

- Confirm mailing addresses for all 1099 recipients before December 31

- File 1099s with the IRS and mail recipient copies by January 31

Prepare for a bar or IRS audit

A bar audit focuses on trust account integrity: whether client funds were held properly, whether individual ledgers match the bank account, and whether your reconciliation records are complete. An IRS audit focuses on income accuracy and expense substantiation. Both require you to produce records quickly, so organizing your files throughout the year rather than in response to a notice is the only practical approach.

Your audit-ready records should include:

- Monthly three-way reconciliation reports for every trust account

- Bank statements for all operating, trust, and payroll accounts

- Individual client trust ledgers for all active and recently closed matters

- Copies of all earned fee transfers with supporting documentation

- Categorized receipts and invoices for every deductible expense

Keep these records for a minimum of seven years. State bars in many jurisdictions require five years of trust records, and the IRS can assess taxes going back six years in cases involving substantial underreporting. Keeping seven years of organized records covers both requirements without managing separate retention timelines.

Choose software and integrations that fit

The software you use for bookkeeping for law firms determines how difficult or straightforward every other process in this guide will be. General accounting tools handle income and expenses well, but they were not built to track individual client trust balances, run three-way reconciliations, or enforce the separation between operating funds and IOLTA accounts. Choosing the right tool from the start saves you from building workarounds that break down under bar scrutiny.

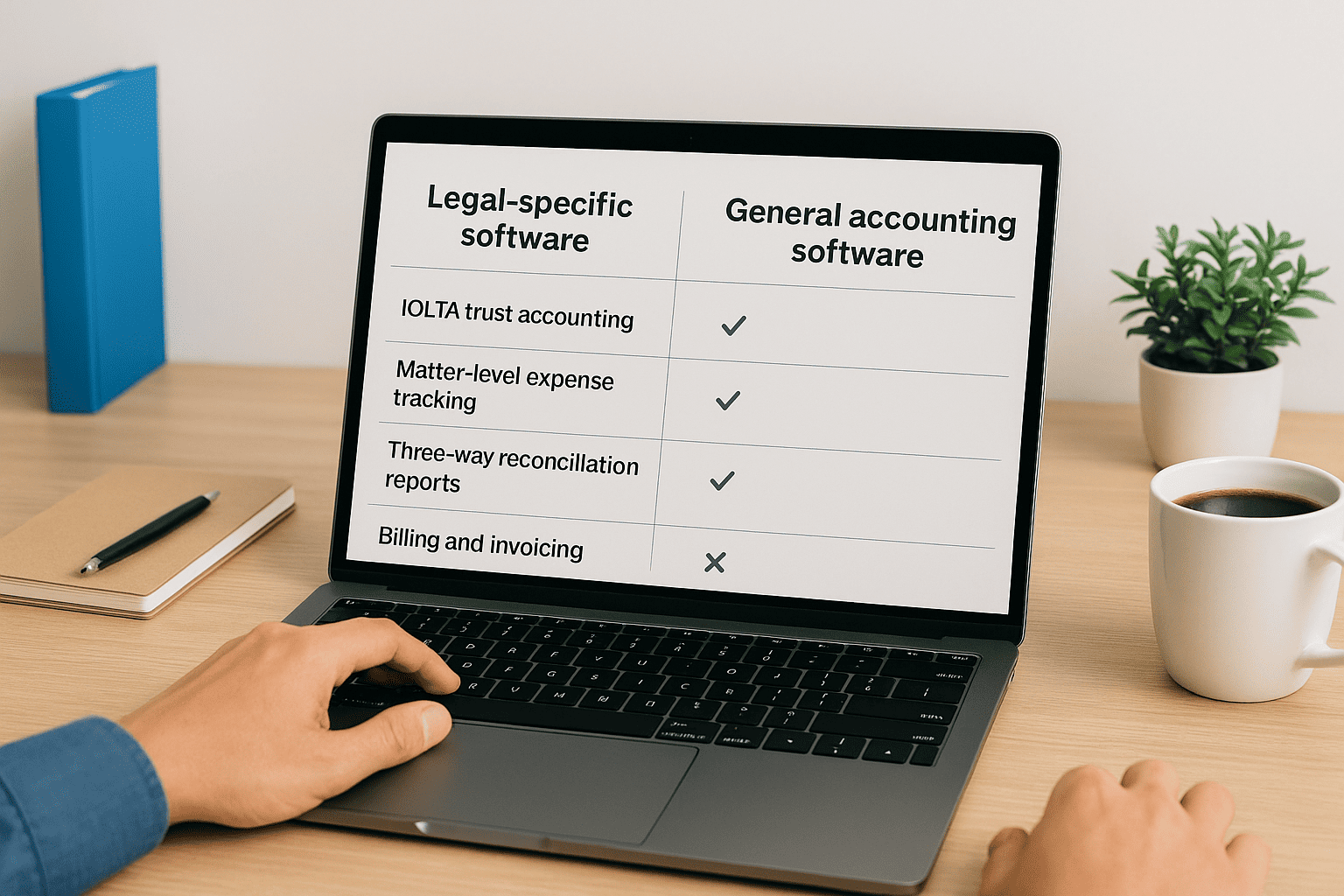

Legal-specific vs. general accounting software

Legal practice management software with built-in accounting gives you trust accounting workflows, matter-level reporting, and client ledger tracking out of the box. General accounting platforms like QuickBooks can work for a law firm, but only if you configure them carefully with the right chart of accounts and discipline around data entry. The table below compares what each category handles well.

| Capability | Legal-specific software | General accounting software |

|---|---|---|

| IOLTA trust accounting | Built-in, compliant by default | Requires manual configuration |

| Matter-level expense tracking | Native feature | Requires workarounds |

| Three-way reconciliation reports | Automated | Manual process |

| Billing and invoicing | Integrated | Separate tool usually needed |

| Tax reporting and financials | Limited in some tools | Strong, especially QuickBooks |

If your general accounting platform does not support client sub-ledgers natively, add them manually through your chart of accounts before you process a single trust deposit.

Connect your billing and accounting tools

Your time-tracking and billing platform should flow directly into your accounting system without requiring manual re-entry. Every time you create an invoice or record a payment in your billing tool, that transaction should appear automatically in your ledger on the same day. Manual data transfer between disconnected systems introduces errors and creates the kind of timing gaps that cause your monthly reconciliation to fail on the first attempt.

The integrations your firm actually needs depend on size, but most firms benefit from connecting these four systems:

- Time and billing software to your accounting platform for automatic invoice and payment sync

- Bank feeds from all operating and trust accounts for daily transaction imports

- Payroll software to your general ledger for automatic payroll entry and tax deposit tracking

- Document storage linked to your accounting tool so receipts and disbursement authorizations stay attached to the transactions they support

Set up each integration before your firm is active, test it with a sample transaction, and confirm that the data lands in the correct account and matter before relying on it at scale.

Decide when to outsource and how to vet help

Managing bookkeeping for law firms in-house works well when your volume is low and your systems are tight. As your caseload grows, the administrative burden of trust accounting, reconciliations, and tax compliance grows with it. At some point, the time you spend on financial records costs more than the work itself, and that is when outsourcing becomes a practical decision rather than a luxury.

Recognize the signs that you need outside help

Several clear signals indicate your firm has outgrown its current bookkeeping setup. If your monthly reconciliation consistently takes more than a few hours, if you have missed a 1099 deadline, or if your trust account has carried unresolved discrepancies longer than one month, your current approach is not scaling. Another clear sign is that your tax preparer is spending significant time cleaning up your books before they can file, which means you are paying twice for work that should happen once.

Watch for these specific warning signs:

- You cannot produce a client trust ledger within 10 minutes of a request

- Your billing and accounting systems are not connected and require manual re-entry

- You discovered a trust balance error after a client asked about their funds

- Your books are more than 30 days behind at any point during the year

If a bar inquiry arrived today and you needed to produce three-way reconciliation records for the past 12 months, knowing whether those records exist and are accurate tells you exactly where your firm stands.

Ask the right questions before you hire anyone

Not every bookkeeper or accountant understands the compliance requirements that apply to legal trust accounts. Before you hire outside help, confirm that the person or firm you are evaluating has direct experience with law firm finances, not just general small business accounting. Ask them to explain how they handle an IOLTA trust account and what their process is for maintaining individual client sub-ledgers. A qualified candidate answers those questions without hesitation.

Use these screening questions for every candidate:

| Question | What a strong answer looks like |

|---|---|

| How do you handle trust account reconciliation? | Describes three-way reconciliation, monthly cadence, and documentation |

| Have you worked with legal billing software? | Names specific platforms and explains how they connect to accounting |

| How do you track earned fee transfers? | Explains the liability-to-revenue sequence with clear steps |

| What records do you maintain for a bar audit? | Lists ledgers, reconciliation reports, and retention timelines |

Verify references from other law firm clients specifically, not general business clients. Specialized experience is not transferable from a retail bookkeeper to a firm managing active IOLTA accounts.

Keep your books clean going forward

Bookkeeping for law firms is not a one-time project you complete and walk away from. Every month brings new retainer deposits, earned fee transfers, and trust reconciliations that require the same precision as the month before. The habits you build now, running reconciliations on schedule, maintaining individual client ledgers, and keeping billing tied to matters, are what prevent small errors from becoming bar complaints or audit findings. Clean books are a direct result of consistent processes, not periodic cleanup efforts.

If you have read through this guide and realized your current setup has gaps you do not have time to close on your own, that is a practical problem with a direct solution. A qualified accounting professional who understands legal trust accounting can take this off your plate entirely. Reach out to Tax Experts of OC to schedule a free consultation and talk through what your firm actually needs.