Owing money to the California Franchise Tax Board is stressful, and it gets worse fast. The FTB can garnish your wages, levy your bank accounts, and file state tax liens, sometimes with less warning than the IRS gives. If you can't pay your balance in full right now, a California FTB payment plan lets you break that debt into monthly installments you can actually manage.

But applying isn't always straightforward. Your eligibility, the amount you owe, and whether your account is already in collections all affect which type of plan you qualify for and how you need to apply. Miss a step or choose the wrong option, and you could face delays or a denied request while penalties and interest keep growing.

This guide walks you through the entire process, eligibility requirements, application methods, what to expect after you apply, and how to avoid common mistakes. At Tax Experts of OC, our CPAs and Enrolled Agents help clients across California and all 50 states resolve state and federal tax debt every day. If your FTB situation is complicated or you've already been turned down, we offer a free 30-minute consultation to help you figure out your best path forward.

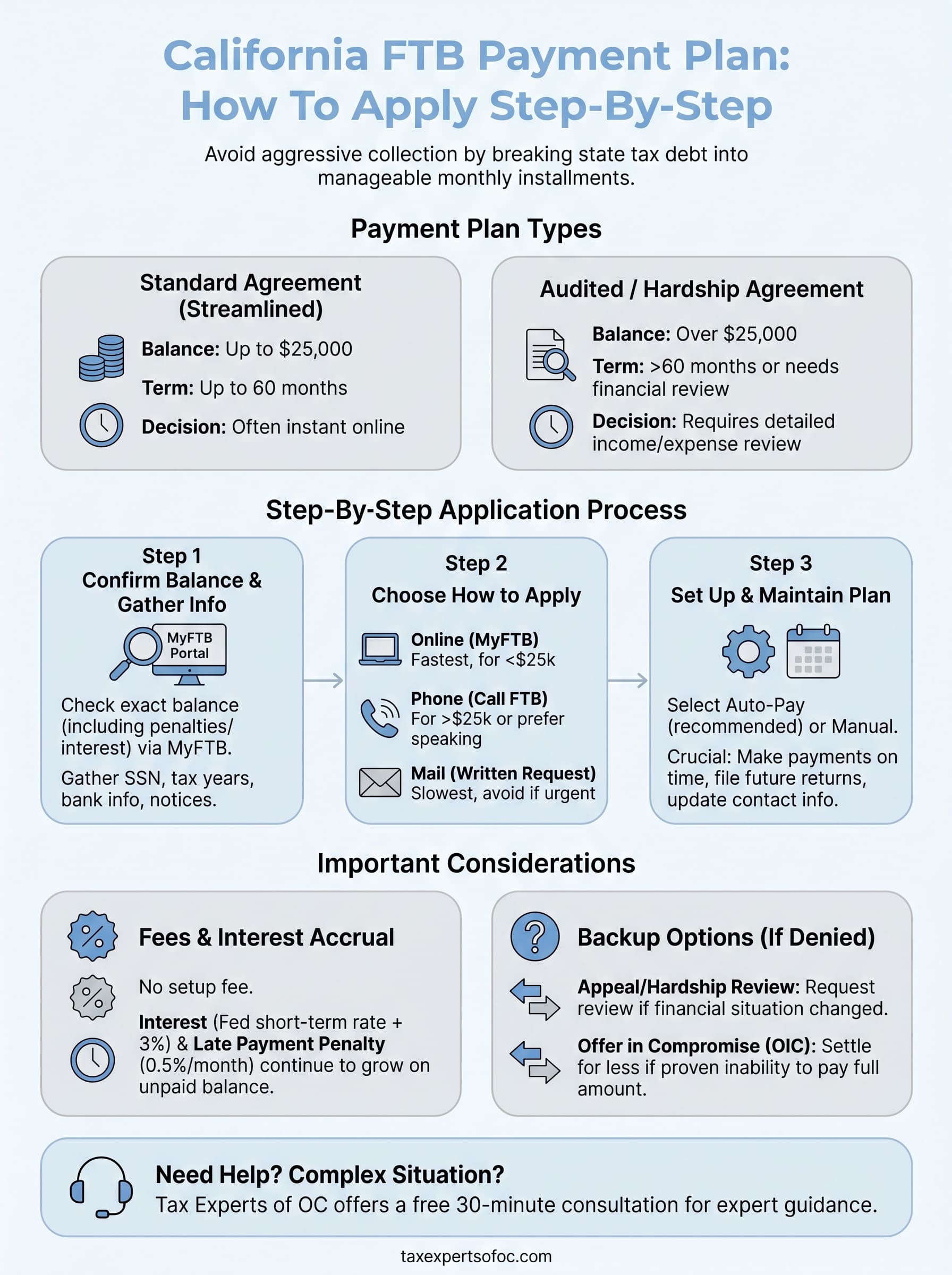

What the California FTB payment plan is and who qualifies

A California FTB payment plan, formally called an installment agreement, is an arrangement where the Franchise Tax Board lets you pay your state tax debt in fixed monthly payments instead of one lump sum. The FTB does not forgive any of the balance, and interest plus penalties continue to accrue until you pay in full. What you gain is time and structure, which prevents the FTB from moving forward with aggressive collection actions like bank levies or wage garnishments while your agreement is active and in good standing.

Keeping your installment agreement active stops most FTB collection activity, but only for as long as you make every payment on time and file all future returns by their deadlines.

The two types of FTB installment agreements

The FTB offers two main options depending on how much you owe and how quickly you can pay. The first is a standard installment agreement, available to individuals who owe up to $25,000 and can pay the full balance within 60 months. The second is an audited or financial-hardship installment agreement, which applies when your balance is above $25,000 or you need more than 60 months to pay. This second type requires the FTB to review your income, expenses, and assets before approving a plan.

| Agreement Type | Balance Limit | Maximum Repayment Term |

|---|---|---|

| Standard | Up to $25,000 | 60 months |

| Audited / Hardship | Over $25,000 | Determined by financial review |

Business entities, including corporations, LLCs, and partnerships, can also request installment agreements, though the FTB evaluates those on a case-by-case basis using the business's financial records.

Who qualifies

To qualify for a standard installment agreement, you generally need to meet several basic conditions. The FTB expects you to be current on all filing obligations, meaning no unfiled state returns. Your account also must not already be assigned to the FTB's Interagency Intercept Collections program or referred to the Attorney General's office for legal action. If either of those applies to your situation, you will need to work through those issues first or contact the FTB directly to discuss options.

Here are the main qualifying criteria at a glance:

- Total balance is $25,000 or less (for the streamlined online option)

- All required California state tax returns are filed and up to date

- You have not recently defaulted on a prior FTB installment agreement

- Your account is not currently in active legal collection proceedings

- You agree to set up automatic bank withdrawals or make timely manual payments each month

Step 1. Confirm your balance and get ready to apply

Before you submit anything, you need to know your exact balance owed to the FTB, including penalties and interest. Applying for a California FTB payment plan without this number means you could request a monthly payment that does not satisfy the FTB's minimum requirements, which leads to delays or an outright rejection.

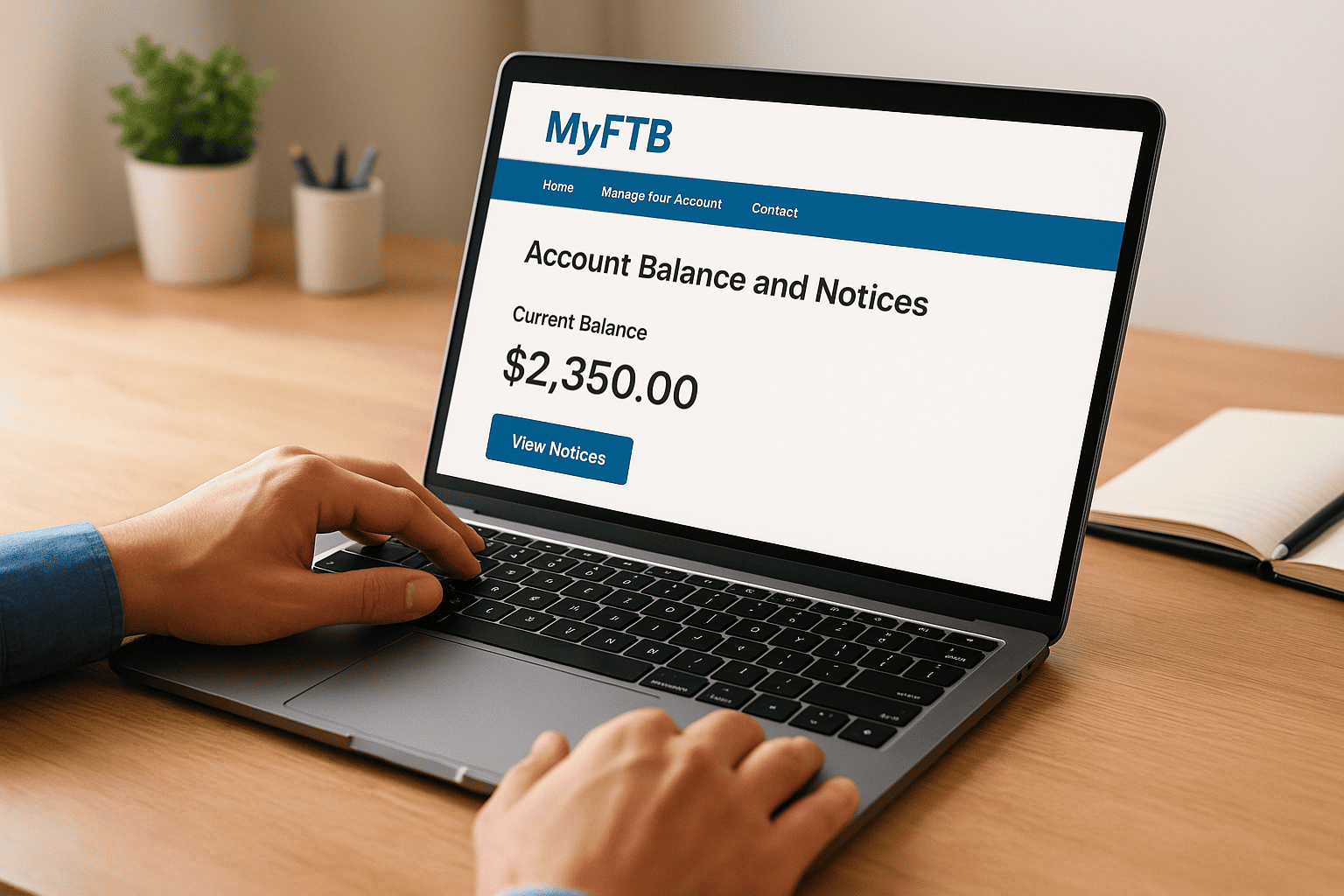

Check your balance through MyFTB

The fastest way to confirm what you owe is through the FTB's online portal, MyFTB. You can log in or create a free account, then navigate to your account balance and notices. The portal shows your current balance, any active collection actions, and copies of notices the FTB has sent. If you have multiple tax years with balances, the portal lists each year separately so you know the full picture before you apply.

If your balance looks different than you expected, check for any unposted payments or recent penalty assessments before moving forward, since applying with the wrong figure can complicate your agreement.

Gather these documents before you apply

Once you confirm your balance, pull together the information you will need to complete the application. Having everything ready in one place keeps the process moving and reduces the chance of an error that delays your approval.

Collect the following before you start:

- Your Social Security Number or California taxpayer ID

- The tax years included in your balance

- Your current monthly income and major expense figures (required if you owe over $25,000)

- Your bank account and routing number if you plan to set up automatic payments

- Copies of any FTB notices you have received, including the notice number

With your balance confirmed and your documents ready, you can move directly into the application.

Step 2. Apply online, by phone, or by mail

Once your documents are ready, you have three ways to submit your California FTB payment plan request. The right method depends on your balance, your situation, and how quickly you want a decision.

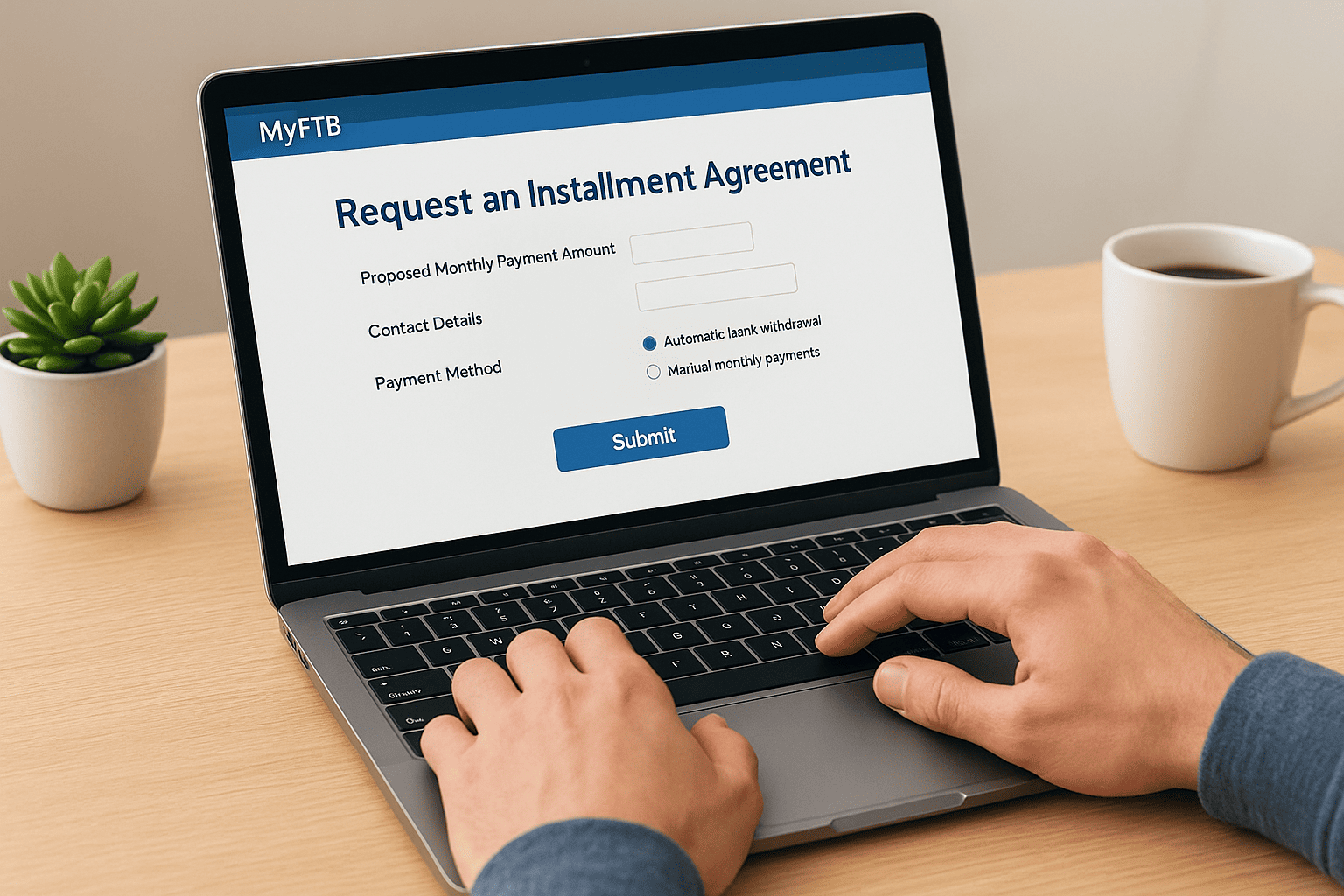

Apply online through MyFTB

The online application is the fastest option and works best if you owe $25,000 or less. Log in to your MyFTB account, select "Request an Installment Agreement," and follow the prompts. You will enter your proposed monthly payment amount, confirm your contact details, and choose between automatic bank withdrawal or manual monthly payments. The FTB typically gives you a same-session decision for standard agreements, so you leave knowing whether you are approved.

The FTB requires your monthly payment to be enough to pay off the full balance within 60 months, so calculate your minimum before you enter a number.

Apply by phone

If you prefer to speak with someone or your balance is above $25,000, call the FTB directly at 1-800-689-4776. A representative will pull up your account, review your balance, and walk you through the application. For higher balances or hardship agreements, the representative may ask about your income and expenses on the call or send you a financial disclosure form to complete afterward.

Apply by mail

Mailing a written request is the slowest method but is available if you cannot use online or phone options. Write a letter that includes the following details and send it to the address on your most recent FTB notice:

- Your full name, address, and Social Security Number

- The tax years covered by your balance

- Your proposed monthly payment amount and preferred start date

- A statement requesting an installment agreement

Processing a mailed request typically takes several weeks, so continue watching for collection notices and document everything you send.

Step 3. Set up payments and keep your plan active

Getting approved is only half the job. Once the FTB confirms your California FTB payment plan, your next priority is making sure your first payment goes through on time and that nothing disrupts your agreement down the road.

Choose your payment method

The FTB gives you two ways to make monthly payments: automatic bank withdrawal or manual payments. Automatic withdrawal is the safer option because it removes the risk of forgetting a due date. You provide your bank's routing number and your checking account number during the application, and the FTB pulls your payment on the same date each month.

Missing even one payment can put your installment agreement in default, which lets the FTB resume collection activity immediately.

If you choose manual payments, you can pay online through your MyFTB account, by phone, or by mailing a check. Whichever method you use, keep a record of every transaction, including confirmation numbers for online payments and certified mail receipts if you send checks.

What to do every month to stay in good standing

Staying current on your agreement requires more than just making payments. The FTB also expects you to file all future California state tax returns on time and pay any new tax balances as they come due. A new unpaid balance from a future tax year can trigger a default even if your monthly installment payments are perfect.

Follow this checklist each month and each filing season:

- Confirm your scheduled payment posted by checking your bank statement or MyFTB account

- File every state return by its deadline, including extensions if you request them

- Contact the FTB immediately if your income drops and you can no longer make the agreed payment, since they may modify your plan rather than default it

- Keep your mailing address and contact information updated in MyFTB so you receive any notices the FTB sends

Fees, processing time, and backup options

A California FTB payment plan does not come with a setup fee, which is a meaningful difference from the IRS installment agreement process. However, interest and penalties continue to accrue on your unpaid balance throughout the entire repayment period, so the longer your agreement runs, the more you ultimately pay.

Pay more than your required monthly minimum whenever you can, since every extra dollar reduces the balance that interest compounds against.

Fees and interest you should expect

The FTB charges interest at the federal short-term rate plus 3 percent, adjusted each calendar year. On top of that, the monthly late payment penalty of 0.5 percent of your unpaid tax continues to build until your balance reaches zero or hits the 25 percent cap. There is no flat enrollment or administrative fee for a standard installment agreement, so your cost beyond the original tax debt is purely interest and ongoing penalties.

How long approval takes

Your approval timeline depends entirely on which application method you use. Online applications through MyFTB produce a near-instant decision for standard agreements. Phone applications typically resolve within minutes to a few days. Mailed requests take the longest, often four to six weeks, so avoid mailing if your account is close to a levy or lien action.

| Application Method | Typical Decision Time |

|---|---|

| Online (MyFTB) | Same session |

| Phone | Minutes to a few days |

| 4 to 6 weeks |

Backup options if the FTB denies your request

If the FTB denies your installment agreement, you still have options. You can request a formal appeal or hardship review, especially if you submitted financial disclosure documents and believe the reviewer made an error. Another route is an Offer in Compromise, which lets qualifying taxpayers settle their FTB debt for less than the full amount owed based on documented financial inability to pay.

Wrap-up and next steps

A california ftb payment plan gives you a structured way to clear your state tax debt without facing immediate collection action. The process is manageable if you confirm your balance first, choose the right application method for your situation, and stay current on both your monthly payments and future filing deadlines. The key risks are defaulting on your plan and letting new balances pile up, both of which you can avoid with consistent attention to your account.

If your balance is above $25,000, you have already been denied once, or the FTB has started collection activity against you, handling this alone becomes significantly harder. A qualified CPA or Enrolled Agent can step in, negotiate directly with the FTB on your behalf, and identify options like hardship agreements or an Offer in Compromise that you might not know are available. Talk to a tax resolution professional at Tax Experts of OC and get your free 30-minute consultation today.