You missed the deadline, and now you're wondering what happens when you file taxes late. Maybe life got in the way, maybe the paperwork overwhelmed you, or maybe you didn't have the money to pay what you owed. Whatever the reason, you're not alone, the IRS receives millions of late returns every year, and the situation is almost always fixable.

That said, ignoring it won't make it go away. The IRS charges both a failure-to-file penalty and a failure-to-pay penalty, and interest starts accruing immediately after the deadline passes. The longer you wait, the more expensive it gets. But here's what most people don't realize: filing late is still far better than not filing at all, even if you can't pay the full balance right now.

At Tax Experts of OC, our CPAs and Enrolled Agents help individuals and business owners across all 50 states resolve exactly these situations, from unfiled returns and back taxes to IRS notices and payment negotiations. This article breaks down the specific penalties and interest you're facing, walks you through how to file a past-due return, and lays out your options for dealing with what you owe. If you're owed a refund, we'll cover that too.

What it means to file taxes late

When you file taxes late, you've submitted your federal return after the IRS deadline without an approved extension on file. For most individual taxpayers, that deadline is April 15 of the tax year following the one you're reporting on. Miss that date, and the IRS marks your return as delinquent, triggering a clock that starts charging you penalties and interest the very next day. The penalty structure is not flat. It grows as a percentage of what you owe, which means the cost of waiting compounds over time rather than staying fixed.

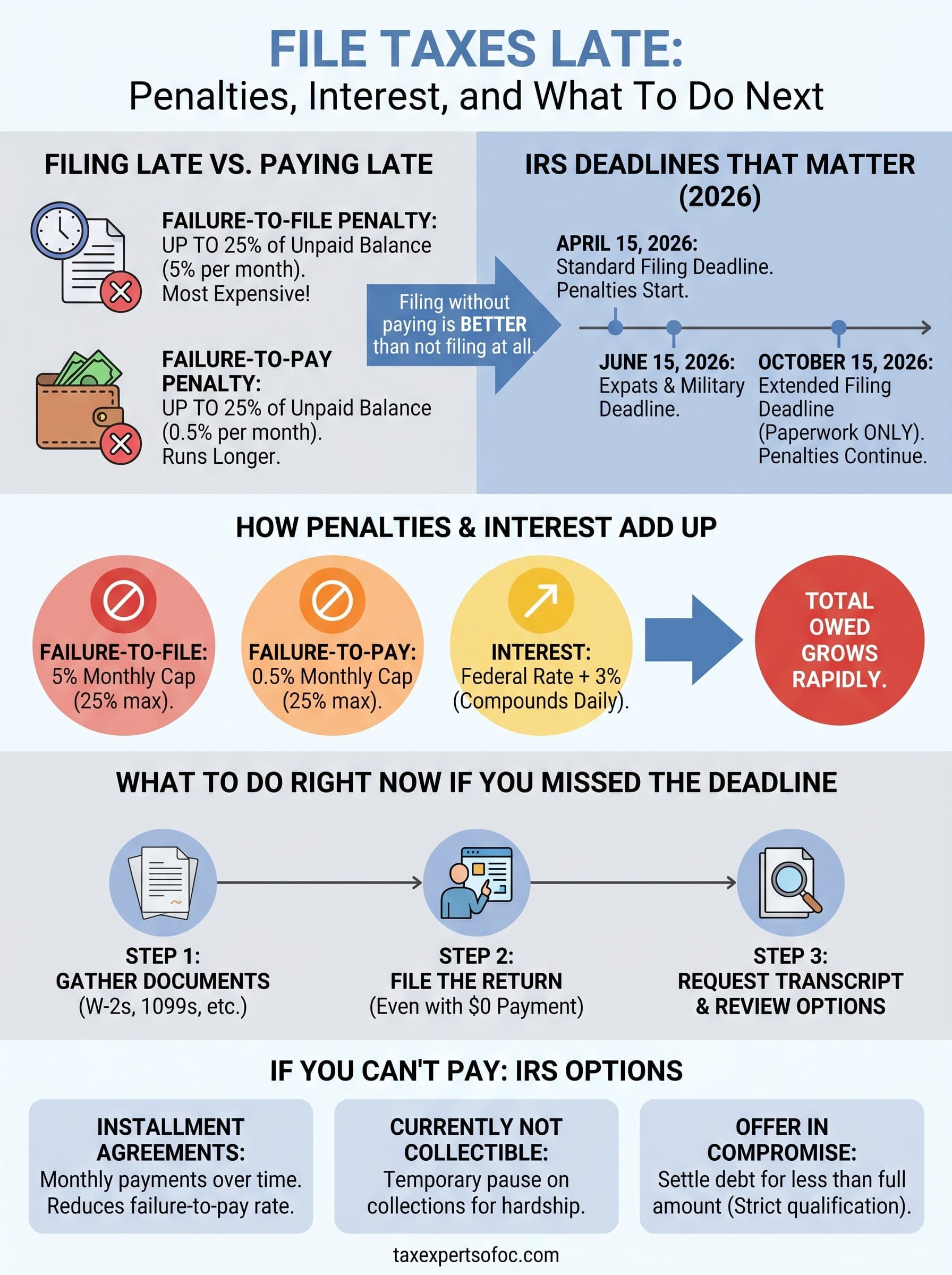

Filing late versus paying late

These two situations are separate in the IRS's eyes, and they carry separate penalties. You can file on time but pay late, or you can be late on both, and each condition triggers its own charge. Most people assume that because they can't pay, there's no point in filing. That assumption is expensive. The failure-to-file penalty is five times larger than the failure-to-pay penalty on a per-month basis, so filing your return even with a zero-dollar payment dramatically reduces the total financial damage.

Filing your return on time, even when you can't pay a cent, is one of the most effective ways to limit what you ultimately owe the IRS.

If you file late and carry an unpaid balance, both penalties run simultaneously. The IRS does apply a partial offset when both penalties overlap in the same month, but you're still paying significantly more than if you had filed on time and worked out the payment separately. The exact rates and caps are covered in detail in the penalty sections below.

When the IRS considers you late

The IRS uses the postmark date on paper returns and the submission timestamp on e-filed returns to determine whether you filed on time. If April 15 falls on a weekend or a federal holiday, the deadline shifts to the next business day. The same rule applies to quarterly estimated tax payments, which carry their own separate due dates throughout the year that are completely independent of your annual filing deadline.

Your filing status also affects the deadline in some situations. Taxpayers living outside the United States on the regular due date automatically receive a two-month extension to June 15, though interest still accrues on any unpaid balance from April 15 forward. Members of the military serving in a combat zone receive special deadline relief under IRS rules. If either situation applies to you, the standard late-filing rules do not fully apply, and you should confirm your specific deadline with a tax professional.

What counts as a filed return

A return is not considered filed until the IRS receives and processes a complete, accurate submission. Sending a blank return or a return missing required schedules does not count. If the IRS rejects your e-filed return due to an error, you have a limited window to correct and resubmit it. Once that window closes, the original submission date no longer protects you, and your return is treated as filed on the resubmission date.

This matters because taxpayers sometimes believe they filed on time after an e-file rejection, only to discover later that the return was never officially accepted. If you're working through a rejection notice, confirm the final acceptance timestamp from your tax software or preparer before assuming your filing date is secure.

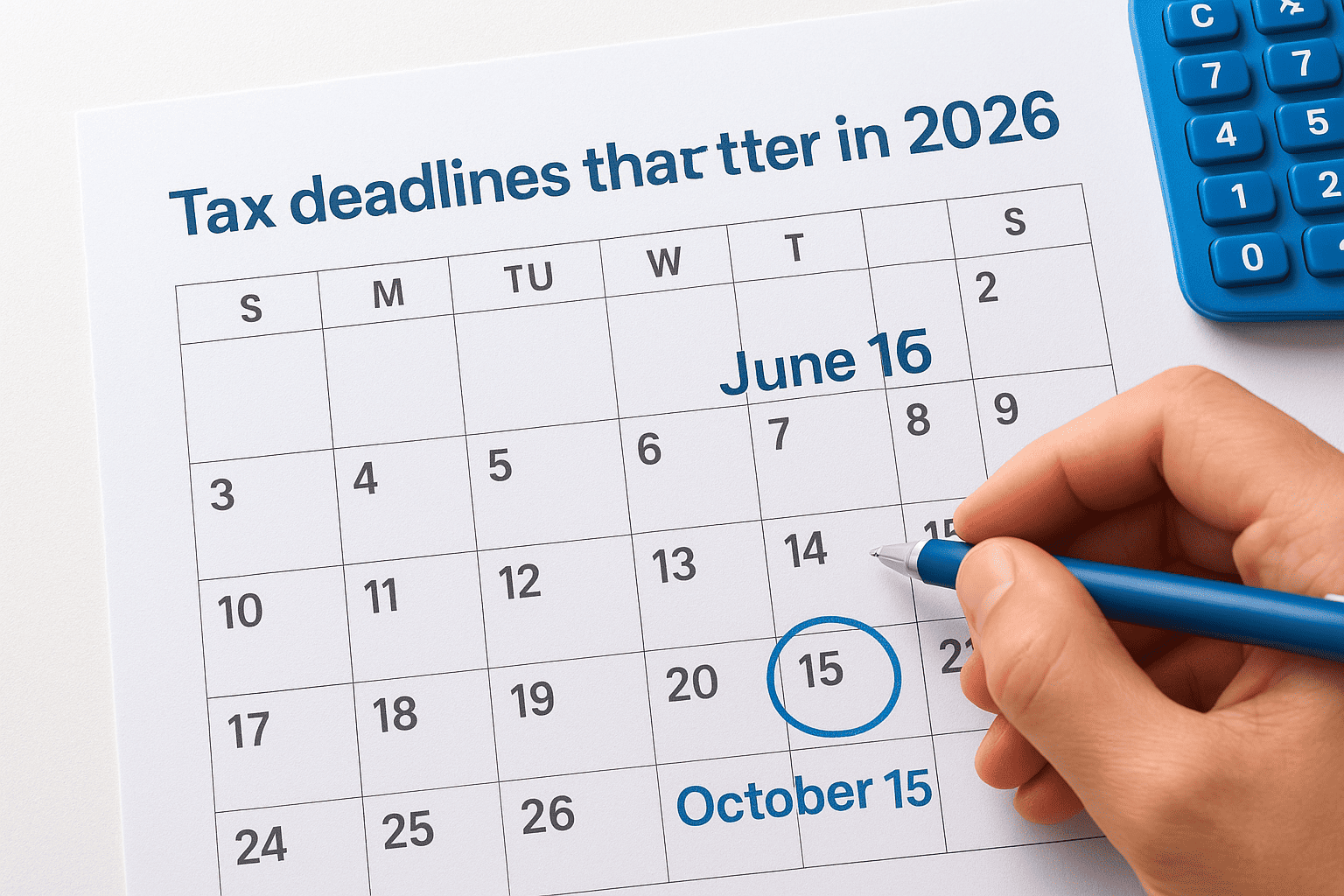

Tax deadlines that matter in 2026

If you're trying to figure out where you stand right now, knowing the exact dates is the starting point. The IRS operates on a fixed calendar, and each deadline triggers a different set of consequences depending on whether you've filed, paid, or done neither. Since today is late June 2026, some of these dates have already passed, which directly affects what you should do next.

The core individual deadlines

April 15, 2026 was the standard filing deadline for your 2025 federal income tax return. If that date passed without a return or an extension request on file, you are already accumulating failure-to-file penalties from April 16 forward. The extended deadline, available only to taxpayers who filed Form 4868 by April 15, pushes the filing due date to October 15, 2026. That extension covers the paperwork, not the payment. Any tax owed was still due on April 15.

If you missed April 15 and did not file an extension, October 15 is no longer your safety net. You are already late, and filing as soon as possible is the only way to stop penalties from growing.

Taxpayers who were living outside the United States on April 15 received an automatic two-month extension to June 16, 2026. If that applies to you, that date has also now passed. Interest on unpaid balances runs from April 15 regardless of which extension category you fall into.

Estimated tax and business deadlines

Quarterly estimated tax payments follow a separate schedule that runs throughout the year. If you file taxes late on your annual return, these quarterly payments may still be due or already overdue on their own timeline. The Q1 2026 payment was due April 15, Q2 was due June 16, Q3 is due September 15, and Q4 is due January 15, 2027.

Business returns carry their own deadlines. S corporations and partnerships filing Form 1120-S or Form 1065 had a March 17, 2026 deadline, with extensions running to September 15, 2026. C corporations filing Form 1120 had an April 15 deadline, with extensions to October 15, 2026. If your business missed its deadline, the same failure-to-file penalty structure applies, though the calculation works differently depending on the entity type and number of partners or shareholders involved.

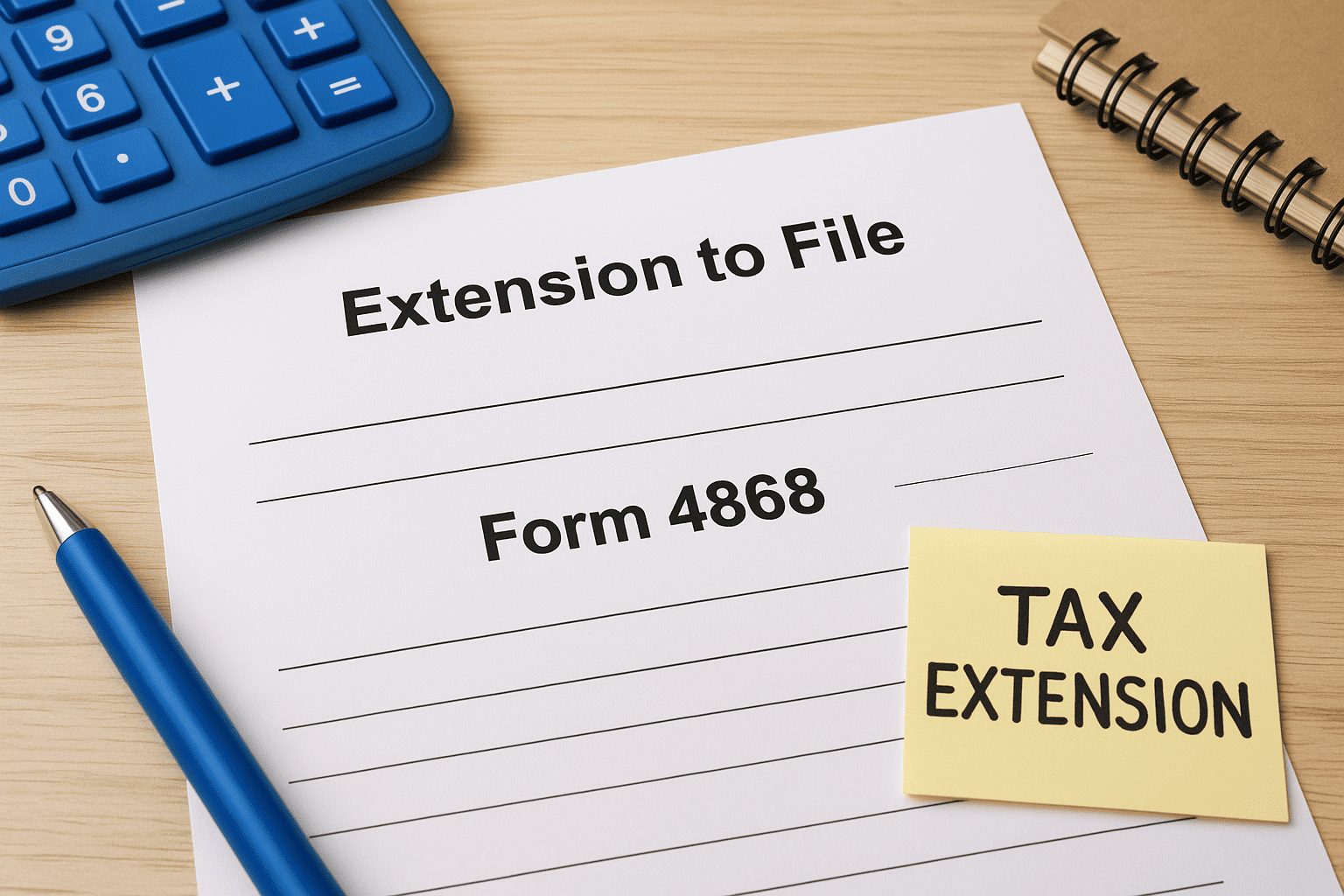

How an extension works and what it does not do

Filing Form 4868 gives you an automatic six-month extension to submit your federal tax return, pushing your filing deadline from April 15 to October 15. The IRS does not require a reason, and approval is automatic as long as you submit the form on time and include a reasonable estimate of what you owe. Many taxpayers treat this as a way to buy themselves time across the board, but the extension only covers one thing: the paperwork.

What Form 4868 actually does

When you submit Form 4868 by the April 15 deadline, the IRS stops the failure-to-file penalty clock for six months. You avoid the 5% per month charge on any unpaid balance during that extension window, provided you filed correctly and on time. This matters most when your return is genuinely complex, such as waiting on a late K-1 from a partnership, resolving questions about business income, or dealing with a multi-state filing situation where the documentation takes time to compile.

You can file Form 4868 electronically through tax software, through a tax professional, or by mailing a paper copy to the IRS. The submission must reach the IRS by April 15, not October 15. If you miss the extension request deadline, you cannot retroactively apply for one, and the failure-to-file penalty begins accruing from the original due date forward. At that point, the only way to limit the damage is to file taxes late as quickly as possible.

What an extension does not cover

Here is where most taxpayers get caught off guard: the extension does not postpone your payment due date. Any federal income tax you owe was still due on April 15, full stop. If you filed a valid extension but did not pay your estimated balance by that date, the IRS charges failure-to-pay penalties and interest starting April 16, even though your return itself is not yet due.

An extension gives you more time to file, not more time to pay. Those are two completely different deadlines, and confusing them is one of the most common and costly mistakes taxpayers make.

The IRS expects you to calculate a reasonable estimate of your tax liability and pay it when you file Form 4868. You do not need a precise figure, but paying nothing when you clearly owe a significant balance increases your exposure to penalties and interest for the entire period between April 15 and whenever you do pay.

Late filing penalty and minimum penalty rules

The failure-to-file penalty is 5% of your unpaid tax balance for each month or partial month your return is late, up to a maximum of 25% of your unpaid balance. That cap is reached at five months. If you owe $10,000 and file five months late, the penalty alone adds $2,500 to your bill before interest or other charges factor in. The IRS treats any partial month as a full month, so being one day late into a new month triggers the full 5% for that period.

How the 5% monthly penalty works

The penalty calculation is based on the net tax you owe after credits and withholding, not your gross tax liability. If your employer withheld enough to cover your full balance, the failure-to-file penalty drops to zero because there is nothing unpaid for the IRS to apply the percentage against. This is why many taxpayers expecting a refund feel no financial urgency to file on time, though there are other consequences to ignoring the deadline covered further below.

When both the failure-to-file and failure-to-pay penalties apply in the same month, the IRS reduces the failure-to-file rate by 0.5% for each overlapping month, bringing the combined monthly rate to 5% rather than 5.5%. The failure-to-pay penalty continues running at its own rate separately. This partial offset helps, but it does not eliminate the cost of being late on both fronts at once.

The minimum penalty rule

If you file taxes late by more than 60 days past the original deadline, or past your extended deadline if you filed Form 4868, a minimum penalty kicks in. For returns due in 2025 and filed in 2026, that minimum is $510 or 100% of your unpaid balance, whichever is smaller. This rule exists to catch taxpayers who wait a very long time to file a return with a small balance, ensuring the IRS collects a meaningful penalty regardless of the dollar amount owed.

The 60-day minimum penalty rule means a $200 tax bill can become a $200 penalty on top of the original balance, effectively doubling what you owe before interest is added.

The minimum penalty does not apply if you owe nothing. A zero-balance return filed late carries no failure-to-file penalty at all, which is another reason why verifying your withholding and credits before assuming you owe is worth the effort before any deadline passes.

Late payment penalty and how interest adds up

The failure-to-pay penalty runs at a much lower rate than the failure-to-file penalty, but it lasts far longer. The IRS charges 0.5% of your unpaid balance for each month or partial month that the balance remains unpaid, with a maximum cap of 25% of the original amount owed. Reaching that cap takes 50 months, which is just over four years. Unlike the failure-to-file penalty, there is no minimum penalty rule attached to the failure-to-pay charge, so even a small unpaid balance accumulates this cost month after month until you resolve it.

How the rate changes once you act

When you set up a payment plan with the IRS, the failure-to-pay penalty rate drops from 0.5% to 0.25% per month for the period the installment agreement is active and in good standing. That reduction does not sound dramatic, but over a multi-year repayment period it meaningfully reduces your total cost. If the IRS issues a final notice of intent to levy, the penalty rate jumps to 1% per month starting 10 days after that notice. Taking action before the IRS escalates collection keeps your penalty rate at its lowest possible level.

How IRS interest compounds against you

Interest is separate from the penalty and runs on a different calculation entirely. The IRS sets the federal short-term interest rate each quarter and adds 3 percentage points on top of it. That combined rate applies to your entire unpaid balance, including any penalties that have already accrued. Interest compounds daily, which means each day your balance is unpaid, the interest for that day is added to the principal and becomes part of the base for the next day's calculation.

Interest on an unpaid balance never stops on its own. It continues until you pay in full, and unlike penalties, the IRS has very limited authority to reduce or remove it.

When you decide to file taxes late with a balance owed, both the penalty and interest are already running. Because interest compounds on the total outstanding amount, penalties that have already piled up make your interest charges grow faster over time. A $5,000 balance that has accumulated $1,200 in penalties is now a $6,200 balance generating daily interest. Paying even a partial amount reduces the base the IRS uses for these calculations, so any payment you can make right now limits the total cost, even if it does not clear the balance completely.

If you're due a refund, what changes

When the IRS owes you money, the rules shift in your favor in one important way: there is no failure-to-file penalty and no failure-to-pay penalty when your return shows a refund balance. The IRS only charges those penalties on unpaid tax, and if you overpaid through withholding or estimated payments, you have no unpaid balance. That means you can file taxes late without triggering the financial penalties described in the previous sections. However, the absence of penalties does not mean you can wait indefinitely.

The three-year window to claim your refund

The IRS enforces a hard three-year deadline for claiming a refund on a late-filed return. If you do not file your return within three years of the original due date, the IRS keeps your money permanently. There is no appeal process, no exceptions for hardship, and no way to recover it after that window closes. For your 2022 tax return, which was due April 18, 2023, that three-year window closes in April 2026, meaning some taxpayers are already losing refunds right now by not acting.

Filing a late return even years after the deadline is worth doing if you are still inside the three-year window, because the IRS does not send your unclaimed refund back to you automatically.

The three-year rule counts from the original due date, not any extension deadline you may have received. If you filed an extension for your 2022 return to October 2023 but never submitted the return, the clock still started in April 2023, not October 2023. Extensions do not reset the refund claim window.

What late filing still costs you, even without a balance

Even when a refund is coming, sitting on an unfiled return carries real costs beyond just losing the refund itself. Your refund does not earn interest while it sits unclaimed with the IRS, so every month you wait is money that could have been in your account working for you. If you also have a balance due for a different tax year, the IRS can apply your refund against that debt, but only if your return is actually on file for them to process.

Your Social Security credits, loan verification records, and government benefit eligibility can also depend on having current tax returns on file. Lenders, housing agencies, and federal program administrators frequently require recent returns as proof of income. A missing return creates problems beyond the IRS, and filing resolves all of them at once.

What to do right now if you missed the deadline

The most important move you can make today is simple: stop waiting. Every additional month you go without filing is another 5% added to your unpaid balance, and another month of compounding interest stacking on top of whatever penalty you have already accrued. If you decide to file taxes late, doing it now rather than next month or next quarter directly reduces the total amount you owe the IRS before any payment negotiation even begins.

Gather your documents first

Before you can file, you need the right paperwork in front of you. Collect every W-2, 1099, and supporting schedule that applies to the tax year you are filing for. If you are missing a W-2 from a former employer, you can request a transcript of your wage and income data directly from the IRS using Form 4506-T, which pulls the information employers already reported on your behalf. Banks and financial institutions that issued 1099s are required to file copies with the IRS, so that data is typically available in your transcript even if your personal copy is lost.

Once you have your documents organized, do not let an incomplete set become a reason to delay further. File with what you have, then amend the return later if additional information surfaces. A slightly imperfect return filed today stops the penalty clock. A perfect return filed six months from now does not.

File the return before anything else

Your priority is the return itself, not the payment. Submitting the return immediately stops the failure-to-file penalty, which runs at 5% per month. The failure-to-pay penalty at 0.5% per month is far less damaging and gives you more time to arrange funds. If you owe a large balance and cannot pay it in full, filing with a $0 payment still reduces your total cost significantly compared to continuing to accumulate both penalties at once.

Filing without paying is always better than not filing at all. The IRS has formal programs to help you pay over time, but none of them apply until you have a return on file.

After your return is accepted, request your tax transcript through your IRS online account to confirm the return posted correctly. This also shows your current balance, including any penalties and interest that have already accrued, so you have an accurate starting point for whatever payment arrangement you pursue next.

If you can't pay, IRS options to consider

Owing money you cannot immediately pay is stressful, but the IRS has formal programs specifically designed for this situation. Filing your return is still the first step regardless of your ability to pay, because none of these options are available until the IRS has your return on record. Once you file taxes late and your balance is confirmed, the programs below give you real, structured paths to resolve what you owe without the situation spiraling further.

Installment agreements

An installment agreement lets you pay your balance over time in monthly amounts you negotiate with the IRS. If you owe $50,000 or less in combined tax, penalties, and interest, you qualify for a streamlined installment agreement, which the IRS approves quickly without requiring detailed financial documentation. You can apply directly through your IRS online account or by submitting Form 9465.

Setting up a payment plan reduces your failure-to-pay penalty rate from 0.5% to 0.25% per month for as long as the agreement stays in good standing.

Interest continues to run on your remaining balance throughout the repayment period, so paying more than the minimum each month reduces your total cost. If your financial situation improves, you can increase your payment amount without penalty. Missing a scheduled payment can default the agreement and return your case to active collections, so choosing a payment amount you can reliably meet matters more than choosing the fastest payoff schedule you can theoretically manage.

Currently not collectible status

If paying anything right now would prevent you from covering basic living expenses like housing, food, and utilities, you may qualify for currently not collectible status. The IRS temporarily suspends collection activity, meaning no levies, no garnishments, and no aggressive collection notices while the status is active. You apply by providing a detailed financial statement through Form 433-F or 433-A showing your income, expenses, and assets.

This status is not forgiveness. Your balance, penalties, and interest continue to grow, and the IRS reviews your financial situation periodically. Once your income improves, collection resumes. However, if the collection statute of limitations expires while you hold this status, portions of your debt may expire uncollected, which is why this option works better as part of a broader strategy than as a standalone plan.

Offer in Compromise

An Offer in Compromise lets you settle your tax debt for less than the full amount owed if you can demonstrate that paying in full would create genuine economic hardship or if there is legitimate doubt about whether the IRS could collect the full balance. The IRS evaluates your income, expenses, asset equity, and future earning capacity using a specific formula. Acceptance rates are lower than many taxpayers expect, so working with a qualified tax professional before submitting significantly improves your odds of a realistic, approvable offer.

Back taxes and what happens if you don't file

Choosing not to file at all is the most costly path available to you. When you file taxes late, you at least establish a record with the IRS and start resolving the situation. When you never file, the IRS does not simply forget about you. The agency cross-references data from employers, banks, and financial institutions every year, and missing returns show up quickly in their system. What follows is a structured escalation process that gets more expensive and more disruptive the longer it runs.

The IRS will file a return for you

If you go long enough without filing, the IRS uses the income data it already has on file to prepare what is called a Substitute for Return, or SFR. This is the IRS's version of your tax return, and it is not done in your favor. The IRS uses the least favorable filing status available, claims no deductions beyond the standard deduction, and applies no credits you may have qualified for. The result is almost always a higher tax bill than you would have owed if you had filed the return yourself.

Once the IRS finalizes an SFR and sends you a notice of deficiency, you have 90 days to respond before the assessed amount becomes official. Missing that window means the IRS can begin collecting immediately, including levies on bank accounts and garnishments on wages. You can still file your own return to replace the SFR, but doing so after a levy has started requires working directly with the IRS to halt collection while your return is processed.

How the collection process escalates

The IRS follows a defined sequence before taking aggressive collection action. You will receive written notices starting with a CP14, which is a simple balance-due notice, progressing through increasingly urgent letters culminating in a Final Notice of Intent to Levy. At that point, the IRS is authorized to seize wages, bank funds, and certain other assets without further warning.

Filing your return, even years after the deadline, stops the IRS from relying on an SFR and gives you control over your own numbers before collection begins.

Unfiled returns also extend the collection window. The IRS normally has 10 years from the date a tax is assessed to collect it, but that clock does not start until a return is filed or an SFR is finalized. Staying unfiled keeps the statute of limitations from running at all, meaning your exposure has no expiration date until you act.

Wrapping up and getting help

When you file taxes late, the financial damage grows with every month you delay. The failure-to-file penalty, the failure-to-pay penalty, and compounding daily interest all run simultaneously on your unpaid balance, and the IRS does not pause collections while you figure out your next move. Filing immediately, even without full payment, stops the most expensive penalty and gives you access to every resolution option the IRS offers.

Your situation is fixable at almost any stage, but the earlier you act, the fewer options the IRS needs to force on you. Whether you are dealing with a single missed deadline, years of unfiled returns, or a balance you cannot pay in full, working with a qualified professional makes a real difference in the outcome. The team at Tax Experts of OC includes CPAs and Enrolled Agents who handle exactly these cases every day. Schedule your free 30-minute consultation with Tax Experts of OC and start resolving your tax situation today.