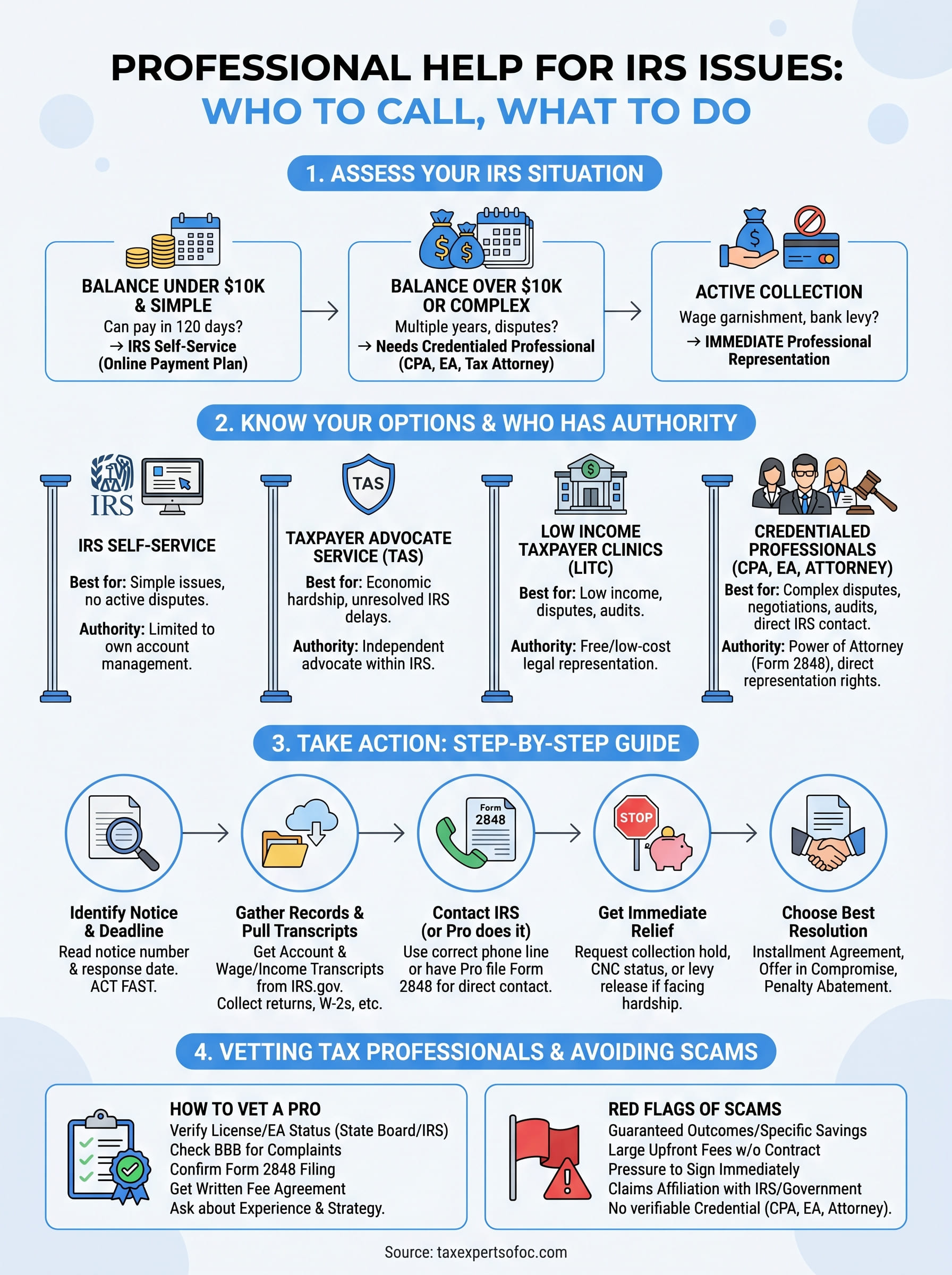

An IRS notice shows up in your mailbox, and suddenly your stomach drops. Maybe it's a balance you weren't expecting, an audit letter, or a collections warning for taxes you thought were handled years ago. Your first instinct might be to call the IRS directly, but anyone who's spent three hours on hold knows that doesn't always get you far. That's when most people start searching for professional help for IRS issues, and the number of options out there can feel overwhelming. Knowing who actually has the authority to represent you before the IRS matters more than most people realize.

The truth is, not every tax professional can speak to the IRS on your behalf. There are specific credentials, CPA, Enrolled Agent, tax attorney, that grant power of attorney and direct representation rights. Choosing the wrong type of help can cost you time you don't have and money you can't afford to lose. At Tax Experts of OC, we handle IRS disputes, back taxes, audits, and unfiled returns every day through our team of credentialed CPAs and Enrolled Agents who work with clients across all 50 states.

This guide breaks down exactly who you can call when IRS problems get serious, what each type of professional actually does, and the step-by-step actions you should take, whether you're dealing with wage garnishments, an unexpected audit, or years of unfiled returns. We'll also cover free government resources like the Taxpayer Advocate Service so you can weigh all your options. By the end, you'll know the right move for your specific situation instead of guessing.

How to decide what kind of IRS help you need

The type of professional help for IRS issues you need depends on three things: the amount of money at stake, whether the IRS is actively taking collection action against you, and whether you need someone to speak directly to the IRS on your behalf. Getting these three factors wrong means you could either spend money on representation you don't need or, worse, handle something yourself that requires a licensed professional with power of attorney.

What the dollar amount and complexity tell you

Not every IRS problem needs a tax attorney or CPA. Small balances under $10,000 that you can pay within 120 days usually don't require professional representation at all. The IRS offers a short-term payment plan online that takes about ten minutes to set up. However, once you cross into larger balances, multiple unfiled years, or disputes over what you actually owe, the math changes fast.

The higher the balance and the more years involved, the more likely it is that a credentialed professional will save you more than they cost.

Use this quick reference to assess your situation before deciding on a next step:

| Situation | Likely level of help needed |

|---|---|

| Balance under $10,000, can pay in 120 days | Self-service IRS payment plan |

| Balance $10,000-$50,000, need a payment plan | Enrolled Agent or CPA |

| Balance over $50,000 or multiple unfiled years | CPA, Enrolled Agent, or tax attorney |

| Active wage garnishment or bank levy | Immediate professional representation |

| IRS audit with complex business records | CPA or tax attorney |

| Criminal tax investigation | Tax attorney only |

How active collection action changes your options

When the IRS moves from sending notices to actually taking your money, your window to act gets much shorter. A wage garnishment can start with as little as 30 days' notice after the final demand letter. A bank levy can freeze your account the same day it is issued. At that point, you need someone who can call the IRS Automated Collection System (ACS) or a Revenue Officer directly and negotiate a hold while a resolution gets put in place.

If you have received IRS Notice CP90, CP297, or Letter 1058, those are final notices of intent to levy. You have 30 days from the date on the letter to request a Collection Due Process hearing. Missing that window gives up significant appeal rights, which is why acting the same week you receive the notice is critical.

Whether you need representation or just guidance

Some situations only require that you understand what the IRS letter means and what to file in response. For example, a simple CP2000 notice, which proposes a change based on mismatched income documents, often just needs a written response with supporting records. You may be able to handle that yourself with some guidance, without paying for full representation.

Other situations require someone who holds IRS power of attorney through Form 2848. That form authorizes a CPA, Enrolled Agent, or attorney to speak directly to IRS agents, pull your account transcripts, receive IRS correspondence on your behalf, and negotiate resolutions. If the IRS has assigned a Revenue Officer to your case, you need a credentialed professional in your corner before you say anything to that officer directly.

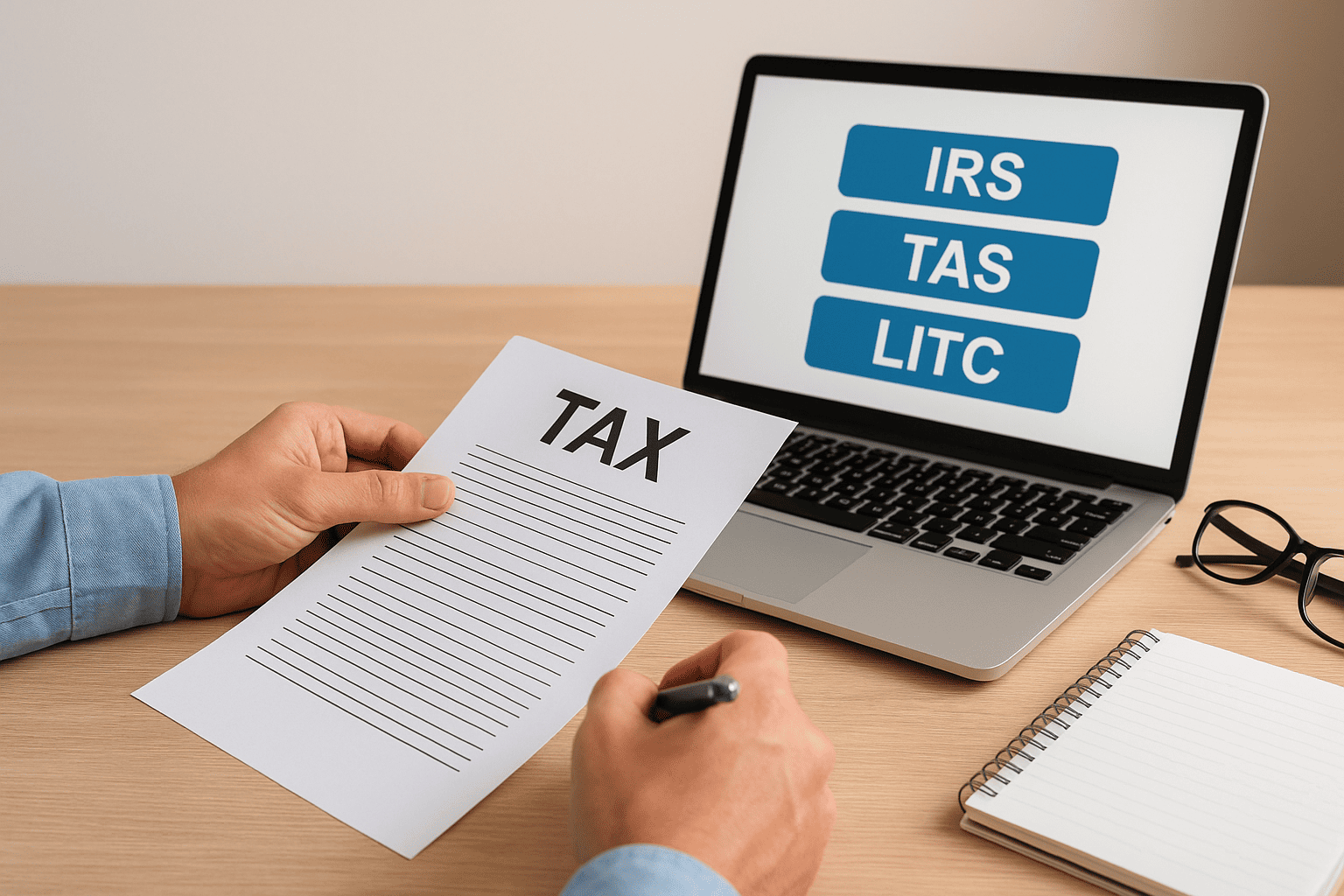

Know your options: IRS, TAS, LITC, and pros

Before you call anyone, you need to understand the four distinct channels available for resolving IRS problems. Each one serves a different purpose and carries different levels of authority. Knowing which channel fits your situation is one of the most important decisions you will make when seeking professional help for IRS issues.

The IRS itself: direct contact and self-help tools

The IRS offers several self-service tools that cover basic account management without requiring a professional. You can set up payment plans, view your account transcript, and respond to simple notices through the IRS website. Direct IRS contact works well when your issue is straightforward and you do not have a disputed balance or active collections.

If the IRS has already assigned a Revenue Officer to your case, handling it yourself almost always works against you.

The Taxpayer Advocate Service (TAS)

TAS is an independent organization within the IRS that helps taxpayers who are experiencing financial hardship or whose problems are not being resolved through normal IRS channels. You can contact TAS if you face an immediate threat to your livelihood, such as a bank levy or wage garnishment that will leave you unable to pay basic living expenses. TAS assigns you a personal advocate at no cost, but they do not replace a credentialed representative in complex disputes.

Here is when TAS is the right call:

- You have already contacted the IRS and your issue remains unresolved after an extended period

- You are facing an economic hardship caused directly by IRS collection action

- You believe the IRS is not following its own procedures on your case

Low Income Taxpayer Clinics (LITC)

LITCs are federally funded legal clinics that represent low-income taxpayers in disputes with the IRS, including audits, appeals, and collection matters. If your income falls at or below 250% of the federal poverty level, an LITC may represent you at little or no cost. These clinics are staffed by attorneys and supervised law students, making them a strong option when you cannot afford private representation.

Credentialed private professionals

When you need someone to negotiate directly with the IRS, handle complex returns, or represent you in an audit, you need a licensed CPA, Enrolled Agent, or tax attorney. These professionals hold power of attorney through Form 2848, which means the IRS deals with them instead of you. Enrolled Agents are federally licensed specifically for tax representation and can handle the full range of IRS resolution programs, making them one of the most practical choices for most taxpayers.

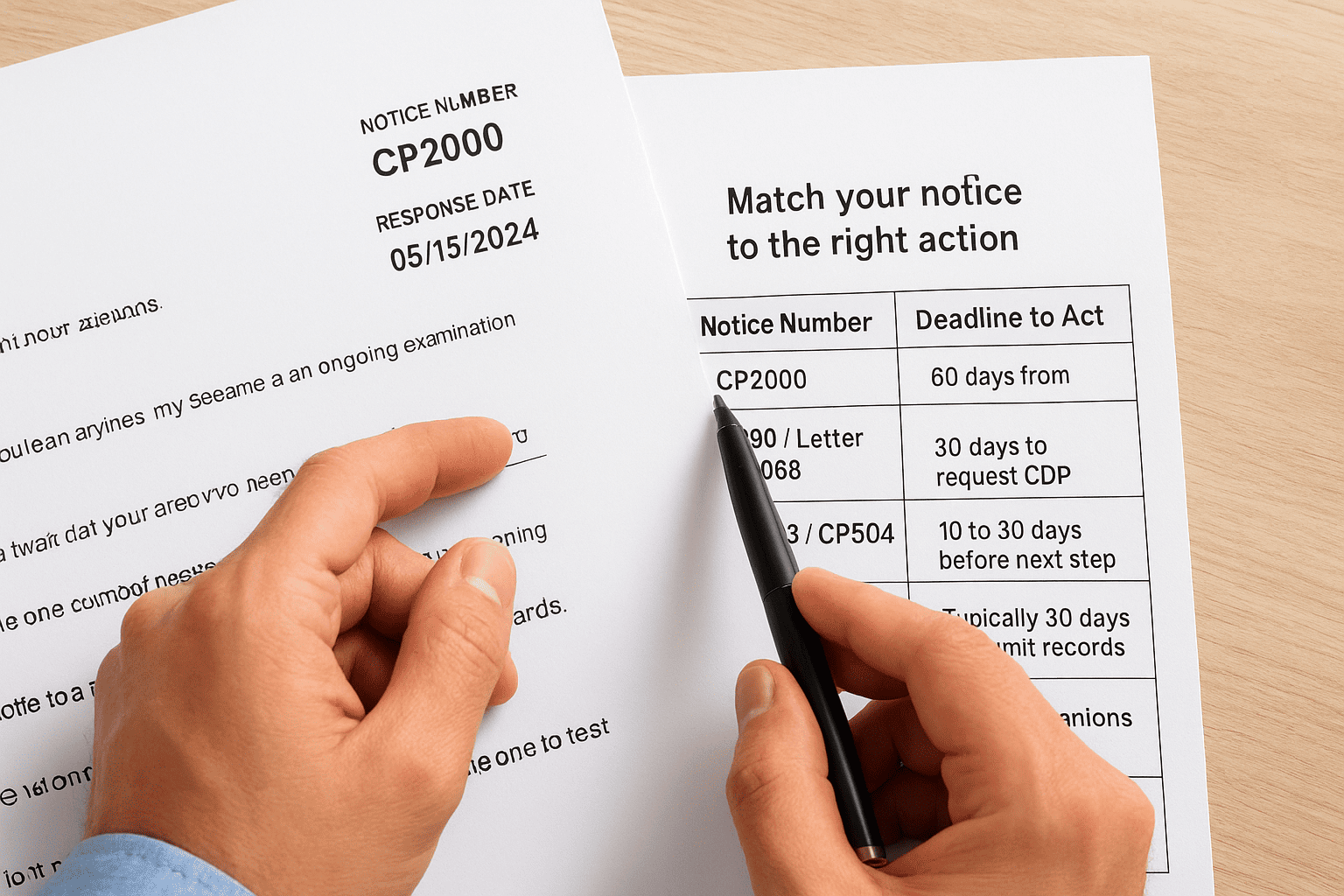

Step 1. Identify your IRS issue and deadlines

Before you call anyone or spend money on professional help for IRS issues, you need to know exactly what you are dealing with. Every IRS notice and letter carries a specific notice number in the upper right corner, and that number tells you the issue type, how serious it is, and how much time you have to respond. Skipping this step means you could pay for representation you do not need or, worse, miss a deadline that strips you of your appeal rights permanently.

Read the notice type and response deadline

Your first move is to locate the notice number and the response date printed on the letter. The response date is not a suggestion. For most collection notices, missing it results in the IRS proceeding with levies, liens, or garnishments without further warning. Read the notice once to understand what the IRS claims you owe or did wrong, then read it a second time specifically looking for dates, dollar amounts, and any reference to appeal rights.

If the letter references a "final notice" or a "notice of intent to levy," treat that date as a hard deadline and act within the same week.

Match your notice to the right action

Different notice types require different responses. Use the table below to identify your notice and the immediate action each one requires:

| Notice Number | What It Means | Deadline to Act |

|---|---|---|

| CP2000 | IRS proposes a change based on mismatched income documents | 60 days from notice date |

| CP90 / Letter 1058 | Final notice of intent to levy | 30 days to request CDP hearing |

| CP503 / CP504 | Balance due, escalating warnings | 10 to 30 days before next step |

| CP75 / CP75A | Audit of refund claim | Typically 30 days to submit records |

| Letter 531 | Notice of deficiency (90-day letter) | 90 days to petition Tax Court |

| CP297 | Notice of levy on federal payments | 30 days to request CDP hearing |

Once you match your notice to the table, write down the deadline on your calendar immediately. If your notice is a CP90, Letter 1058, or CP297, do not wait to consult a professional. Those three letters signal that the IRS is ready to seize your wages or bank accounts within 30 days. For a CP2000 or CP75, you typically have more time, but responding with accurate documentation early prevents the proposed change from becoming a final assessment.

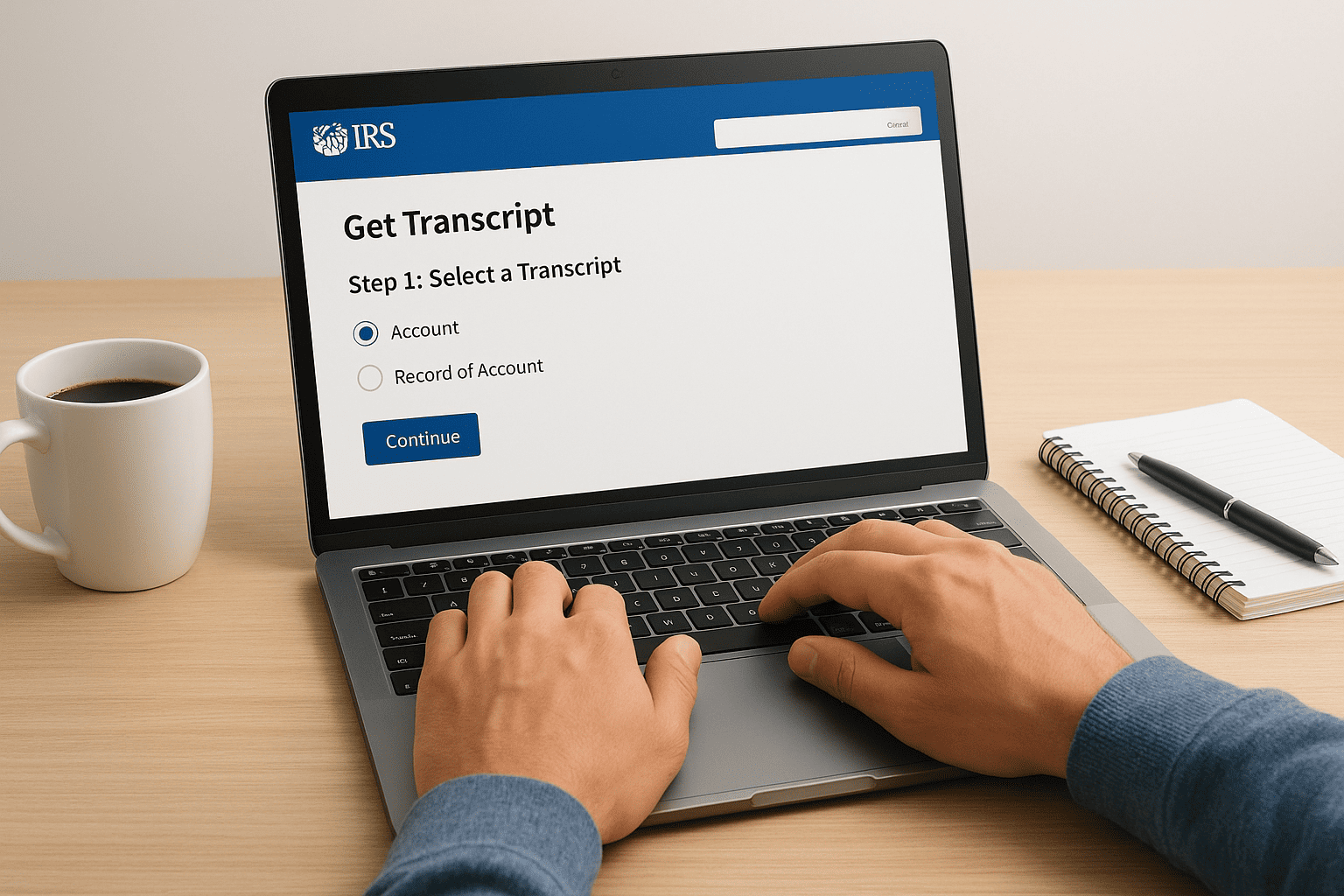

Step 2. Gather records and pull IRS transcripts

Before you call the IRS or hire anyone for professional help for IRS issues, you need to know what the IRS knows about you. Your account transcript is the most important document in any resolution process because it shows every return filed, every payment posted, every penalty assessed, and every notice the IRS claims to have sent. Walking into a negotiation without this information is like disputing a bank charge without seeing the statement.

Pull your transcripts before your first consultation with any professional, so you are not paying for time spent on discovery you could have gathered yourself.

Which records to collect before any meeting

Having the right documents ready speeds up every step that follows and prevents delays caused by missing information. Gather the following before contacting the IRS or any representative:

- Tax returns for all open or disputed years, including any amended returns

- W-2s, 1099s, and K-1s for each year in question

- Bank statements covering income and deductible expenses for disputed periods

- IRS notices and letters you have received, organized by date

- Prior payment records, including any installment agreement statements

- Business financial records if the dispute involves self-employment or a business entity

How to pull your IRS account transcripts

Your IRS account transcript is the single most useful document you can access before taking any action. It shows what the IRS has on file for your account, including balances, penalties, and credits, organized by tax year. You can get it free through the official transcript tool at IRS.gov.

There are four transcript types worth knowing:

| Transcript Type | What It Shows |

|---|---|

| Account Transcript | Payments, penalties, adjustments, and notices by tax year |

| Return Transcript | A copy of the tax return as originally filed |

| Wage and Income Transcript | Income documents the IRS received from employers and payers |

| Record of Account | A combined summary of the return and account activity |

For most IRS disputes, request the Account Transcript and the Wage and Income Transcript for each year involved. Download all years in question, not just the most recent one. If you cannot access the online tool, submit IRS Form 4506-T by mail to request transcripts directly, though that process can take several weeks and may slow your response timeline if a deadline is approaching.

Step 3. Contact the IRS the right way

Once you have your transcripts and records in hand, you are ready to contact the IRS. This step requires deliberate preparation before you ever dial a number, because what you say during an IRS call becomes part of your account history. If you have hired professional help for IRS issues, your representative should make this call on your behalf using Form 2848. If you are handling it yourself, follow the steps below exactly.

Choose the right IRS phone line

The IRS has separate phone lines for different issue types, and calling the wrong one wastes significant time. Using the number printed on your specific notice is almost always faster than calling the general helpline, because it routes you to the unit that already has your case.

Here are the most commonly used IRS contact numbers:

| Issue Type | Phone Number |

|---|---|

| Individual accounts and notices | 800-829-1040 |

| Business accounts | 800-829-4933 |

| Installment agreements | 800-829-7650 |

| Taxpayer Advocate Service | 877-777-4778 |

| Number on your specific notice | Listed on your letter |

Call early in the morning on Tuesday, Wednesday, or Thursday to reach an agent faster. Monday mornings and the days around tax deadlines carry the highest call volumes and the longest wait times.

What to say and document during the call

Before you dial, write down your Social Security number, the notice number, the tax years in question, and the dollar amount the IRS is claiming. Have your account transcript open so you can reference specific line items if the agent disputes anything. Never agree to a payment amount during the first call without reviewing your full financial picture first.

Ask the agent to read back the resolution discussed and note the name, employee ID, and timestamp of every IRS representative you speak with.

Use this call script as your starting point:

"My name is [your name]. My SSN is [number].

I am calling about notice [number] for tax year [year].

I want to understand the balance and my options

for resolving this account.

Can you confirm the current balance, including penalties

and interest, and tell me what resolution programs

I may qualify for?"

Write down everything the agent tells you, including any reference numbers or case notes they add to your account. If the agent offers a resolution, ask for the terms in writing before you agree to anything.

Step 4. Get immediate relief from collections

When the IRS is actively garnishing your wages or has levied your bank account, your immediate goal is to stop the bleeding before negotiating a long-term resolution. This is the step where getting professional help for IRS issues pays for itself fastest, because a credentialed representative can contact the IRS Automated Collection System directly and request a hold while a formal resolution gets established. Every day without action is another day the IRS can take money.

A collection hold gives you breathing room, but it is not a permanent fix. Use the time it buys to move quickly on a formal resolution.

Request a collection hold through hardship or pending resolution

You can request a temporary collection hold by calling the IRS and stating that you are in economic hardship or that a resolution is actively being prepared. The IRS can mark your account as "pending resolution" and pause levy or garnishment action while you submit paperwork. To request this, call the number on your notice and state the following clearly:

"I am calling to request a temporary hold on collection

activity for SSN [number], tax year [year].

I am [currently working with a representative /

experiencing economic hardship] and need time to

submit a formal resolution request.

Can you note my account and confirm the hold period?"

Write down the employee ID and confirmation number from that call. Without documentation, the hold may not reflect in your account.

Apply for Currently Not Collectible status

If your income barely covers basic living expenses, the IRS may classify your account as Currently Not Collectible (CNC). CNC status pauses all active collection action, including levies and garnishments, without requiring a payment plan. To qualify, you submit IRS Form 433-A (for individuals) or Form 433-B (for businesses), which documents your income, expenses, and assets. The IRS then compares your allowable living expenses against its national standards to determine whether you have any disposable income available to pay the debt.

Release a wage garnishment or bank levy

A levy release is possible even after the IRS has already taken action. Your representative contacts the ACS unit or assigned Revenue Officer and provides documentation showing hardship, a pending installment agreement, or an error in the levy itself. The IRS must release a levy if it creates an economic hardship under Internal Revenue Code Section 6343. Submit your hardship documentation the same day you request the release, because the IRS typically requires it before issuing a formal release letter to your employer or bank.

Step 5. Choose the best resolution program

Once you have stopped active collection action, you need to commit to a permanent resolution rather than staying on hold indefinitely. The IRS offers several formal programs, and choosing the right one depends on your income, your assets, and how much of the balance you can realistically pay. Getting professional help for IRS issues at this stage helps you avoid applying for the wrong program and delays that add more penalties to your account.

Installment agreements

An installment agreement lets you pay your balance in monthly installments over time, typically up to 72 months for balances under $50,000. If your balance is under that threshold, you can apply online through the IRS payment plan portal without submitting financial statements. For balances over $50,000, the IRS requires a Form 433-A or 433-F, which documents your income and expenses so the IRS can calculate what it considers an affordable payment.

Use this template when requesting an installment agreement by phone:

"I am calling to set up an installment agreement for

SSN [number], tax years [list years].

The total balance is approximately $[amount].

I would like to request a [72-month / partial pay]

installment agreement based on my financial situation.

Can you confirm the minimum payment required and

the terms for keeping the agreement in place?"

Offer in Compromise

An Offer in Compromise (OIC) allows you to settle your tax debt for less than the full amount if paying in full would create a genuine economic hardship. The IRS calculates your "reasonable collection potential" based on your assets and future income. You submit your offer using IRS Form 656, along with Form 433-A (OIC) and a $205 application fee. The IRS accepts roughly 30 to 40 percent of OIC applications each year, so your numbers need to genuinely support the offer amount before you apply.

Do not submit an OIC as a delay tactic. The IRS flags weak offers quickly, and a rejected application resets your timeline without stopping interest from accumulating.

Penalty abatement

First-time penalty abatement is one of the most underused relief options available. If you have a clean compliance history for the three years prior to the year in question, the IRS will typically remove failure-to-file and failure-to-pay penalties without requiring any financial documentation. Call the IRS and request first-time abatement after your balance is fully paid or after you have set up an installment agreement, because the IRS will not grant it while your account shows unpaid penalties still accruing.

Step 6. Handle audits and exams with representation

An IRS audit does not automatically mean you did something wrong, but it does mean the IRS wants documentation that supports what you reported. Whether the audit arrives as a letter requesting records or as a full office exam with an agent, handling it without qualified representation significantly increases your risk of paying more than you actually owe. This is where professional help for IRS issues carries the most direct financial value, because a credentialed CPA or Enrolled Agent knows exactly what the IRS can and cannot demand from you.

Never respond to an audit notice by sending more documents than the IRS specifically requested, because extra records often open new lines of inquiry.

Know what type of audit you are facing

The IRS conducts three types of audits, and each one requires a different response strategy. Identifying your audit type from the notice determines how quickly you need to act and what level of representation you need.

| Audit Type | How It Works | Typical Timeline |

|---|---|---|

| Correspondence audit | IRS requests specific documents by mail | 30 to 60 days to respond |

| Office audit | You or your representative meet at an IRS office | Scheduled appointment |

| Field audit | Revenue Agent visits your home or business | Assigned by Revenue Officer |

Correspondence audits are the most common and often the most manageable. Office and field audits involve direct agent contact, which means your representative needs to attend in your place using Form 2848 to prevent you from making statements that could expand the scope of the exam.

Prepare your documentation before the audit date

Your representative will request a specific list of documents tied to the items the IRS flagged. Pull together receipts, bank statements, mileage logs, or business records that directly support each line item under review. Gaps in records do not automatically mean the IRS wins, because your representative can use alternative documentation methods, such as bank deposit analysis or reconstructed records, to support your position.

Use this response template when submitting audit documents by mail:

[Your Name]

[Your Address]

[Date]

Re: Response to Audit Notice [Notice Number]

SSN: [Your SSN]

Tax Year: [Year]

Dear IRS Examiner,

Enclosed are the documents requested in your notice

dated [date], supporting the items listed below:

1. [Document Type] - supporting [Line Item / Schedule]

2. [Document Type] - supporting [Line Item / Schedule]

Please contact my authorized representative

[Name, Credential] at [Phone Number] for any

additional questions.

Sincerely,

[Your Name]

Send everything by certified mail with return receipt so you have proof of delivery and a timestamp that protects you if the IRS claims it never received your response.

Step 7. Vet and hire a tax pro without getting scammed

The tax resolution industry includes legitimate credentialed professionals and outright fraudsters who collect large upfront fees and disappear without filing a single form. When you search for professional help for IRS issues, the quality of who you hire determines whether your problem gets solved or compounds. Verifying credentials before signing anything takes under ten minutes and protects you from paying thousands of dollars to someone who has no legal authority to represent you before the IRS.

Check credentials before paying anything

Every professional who can represent you before the IRS holds one of three specific credentials: CPA, Enrolled Agent, or tax attorney. You can verify all three through official public databases at no cost. Confirm a CPA's license through your state's board of accountancy. Verify an Enrolled Agent's active status directly through the IRS website. Check a tax attorney's bar membership through your state bar association's public directory.

Run through this checklist before signing any agreement:

- Confirm their license or credential is active and in good standing

- Verify their business address is a real office, not a P.O. box

- Check the Better Business Bureau for unresolved complaints

- Confirm they will file Form 2848 to formally represent you

- Get a written fee agreement before making any payment

Red flags that signal a scam operation

Guaranteed outcomes and large upfront fees with no written contract are the two clearest warning signs in the tax resolution space. No legitimate professional can promise the IRS will accept an Offer in Compromise or remove a specific penalty before reviewing your full financial picture. Any firm that promises a specific result before pulling your transcripts is making a claim they cannot support.

If a firm cannot name the specific credentialed professional who will handle your case and demands the full fee upfront, stop the conversation immediately.

Watch for these behaviors before committing:

- Refuses to share their license or EA number when asked directly

- Collects a retainer but never files Form 2848 on your behalf

- Pressures you to sign before you have read the full contract

- Claims affiliation with the IRS or any government agency

Ask these questions before signing anything

Before you commit to any representation, ask the professional three direct questions that reveal whether they are qualified and operating honestly. Write down their answers so you can compare them against what you verified independently through official sources.

1. What is your credential, and can I have your

license or EA number to verify it myself?

2. Who specifically will handle my case, and will

they sign Form 2848 as my representative?

3. What is your fee structure, and what happens

if the IRS rejects the resolution we pursue?

A clear path forward

Resolving an IRS problem is not a single phone call or a one-form fix. It is a sequence of deliberate steps, starting with reading your notice, pulling your transcripts, and identifying your deadlines before you contact anyone. Each step in this guide builds on the last, and skipping any of them often creates delays that cost you more money in penalties and interest. The type of professional help for IRS issues you need depends entirely on what the IRS is claiming, how much you owe, and whether active collection action is already in motion.

Your situation is specific, and a generic approach rarely produces the best outcome. Whether you are facing a wage garnishment, an audit, or years of unfiled returns, the right move is to work with credentialed professionals who deal with the IRS every day. Schedule your free 30-minute consultation with Tax Experts of OC and get a clear answer about where you stand.