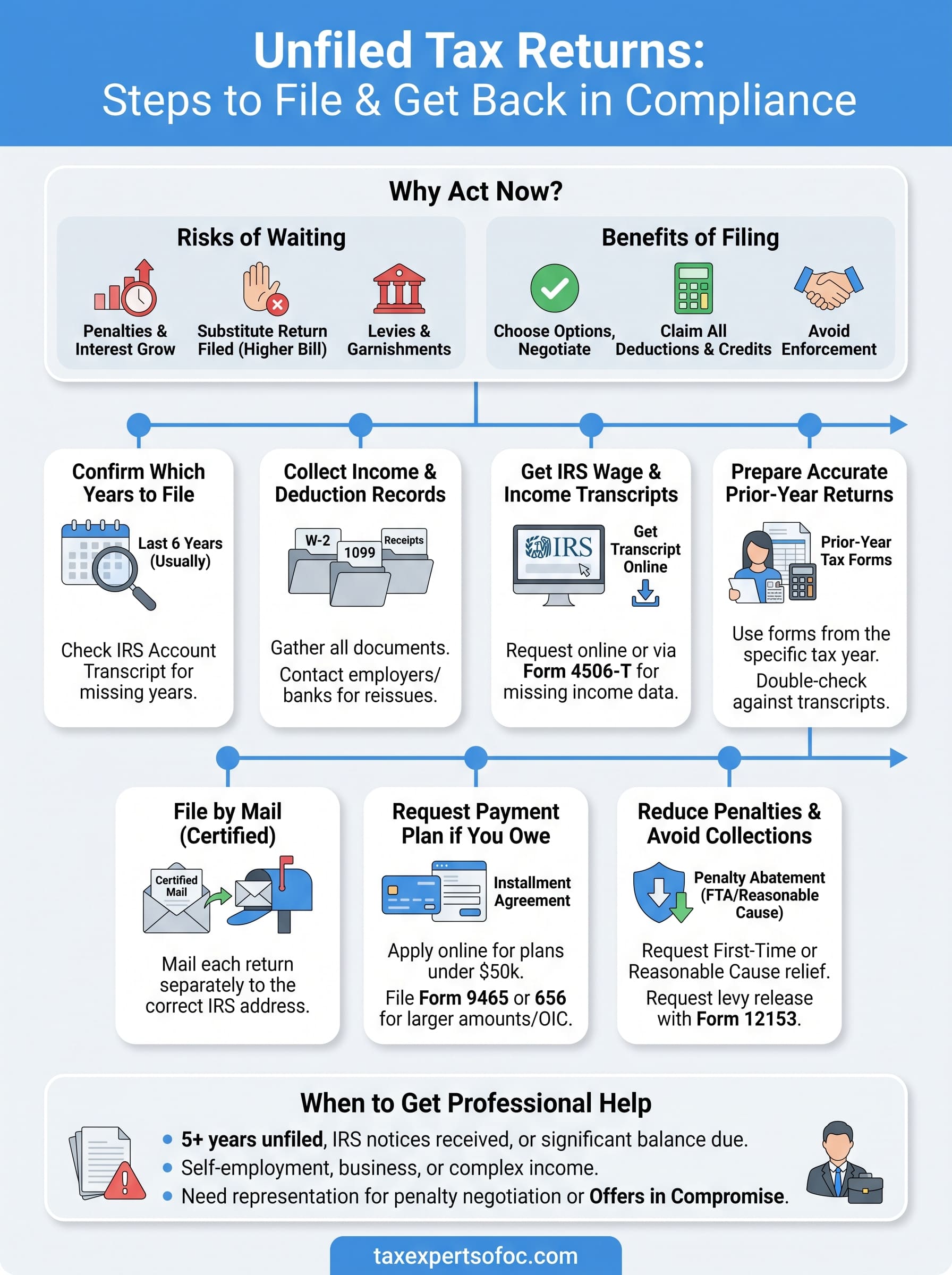

If you have one or more years of tax returns you never filed, you're not alone, and you're not out of options. Millions of Americans fall behind on their taxes for all kinds of reasons: job loss, illness, overwhelm, or simply not knowing where to start. Whatever brought you here, searching for unfiled tax returns help is the right first step. The IRS hasn't forgotten about those missing returns, but the good news is that you can still fix this before the consequences get worse.

The penalties for not filing grow over time. So does the risk of the IRS filing a substitute return on your behalf, one that almost certainly won't include deductions or credits you're entitled to. Wage garnishments, bank levies, and even criminal prosecution are all on the table the longer you wait. But here's what most people don't realize: the IRS generally works with taxpayers who come forward voluntarily, and there are clear steps you can follow to get back into compliance.

At Tax Experts of OC, our CPAs and Enrolled Agents help clients across all 50 states resolve exactly this kind of problem, from gathering old records and preparing past-due returns to negotiating directly with the IRS on penalties and payment arrangements. This guide walks you through the full process of filing back taxes, including which forms you'll need, how far back you may need to file, and when it makes sense to bring in a qualified tax professional rather than going it alone.

What unfiled tax returns mean and why to act now

An unfiled tax return is simply a return for a tax year in which you had a filing requirement but never submitted one. If your income exceeded the IRS filing threshold for that year, you were legally required to file. Not doing so does not erase that obligation. The IRS tracks W-2s, 1099s, and other income documents that third parties report, so they already know you had income, even if you never sent in a return.

What the IRS does when you don't file

When you skip filing, the IRS does not simply wait indefinitely. After a period of inactivity, the IRS can file a Substitute for Return (SFR) on your behalf under Internal Revenue Code Section 6020(b). An SFR uses only the income data the IRS already has. It does not account for your deductions, exemptions, credits, or filing status adjustments that could significantly lower your bill.

If the IRS files an SFR for you, the resulting tax bill is almost always higher than what you would owe if you filed the return yourself with all applicable deductions included.

Once the IRS issues an SFR-based assessment, the collection process can begin. That means the IRS can issue a tax lien against your property, levy your bank accounts, or garnish your wages without first going to court. These actions can happen faster than most people expect, and reversing them requires navigating IRS procedures that are difficult to handle without experience.

The penalties and interest that build up

Every month you do not file, two separate penalties can stack against you. The failure-to-file penalty is 5% of your unpaid tax per month, up to a maximum of 25%. On top of that, a failure-to-pay penalty of 0.5% per month also accrues. Interest compounds daily on the unpaid balance at a rate tied to the federal short-term rate plus 3%.

Here is a quick breakdown of what those penalties look like over time on a $5,000 tax liability:

| Months Unfiled | Failure-to-File Penalty | Failure-to-Pay Penalty | Estimated Total Owed |

|---|---|---|---|

| 1 month | $250 | $25 | $5,275 |

| 3 months | $750 | $75 | $5,825 |

| 5 months | $1,250 | $125 | $6,375 |

| 12 months | $1,250 (capped) | $300 | $6,550+ |

Note: Interest continues to compound after penalties reach their cap, so the actual amount owed keeps climbing regardless.

Why coming forward now works in your favor

Seeking unfiled tax returns help before the IRS contacts you puts you in a much stronger position. Taxpayers who file voluntarily, before the IRS opens a formal examination or sends a notice of deficiency, have far more options available to them. You can choose your correct filing status, claim all deductions you qualify for, and negotiate a payment plan or penalty relief on your own terms rather than reacting to IRS enforcement.

The IRS also has programs specifically designed to help people who come forward on their own, including penalty abatement for first-time filers and installment agreement options for those who cannot pay in full right away. Waiting until the IRS initiates contact removes many of these options and generally produces a worse financial outcome. The sooner you take action, the more control you keep over how this gets resolved.

Step 1. Confirm which tax years you must file

Before you prepare a single form, you need to know exactly which years you have a return due for. Many people assume they must file for every year going back a decade or more, but that is not always accurate. The IRS's standard requirement under the Internal Revenue Manual (IRM 5.19.2) is that delinquent taxpayers typically need to file the last six years of missing returns to be considered in compliance. However, your specific situation may require more or fewer years depending on whether the IRS has already filed SFRs, issued notices, or opened a collection case against you.

How far back the IRS requires you to file

The six-year rule is the IRS's general compliance benchmark, not a legal statute of limitations on filing. The IRS can technically require returns for any year you had a filing obligation. That said, in practice, most voluntary compliance cases focus on the six most recent tax years unless your case involves fraud, large unpaid balances, or a criminal investigation. If you owe significant amounts from years outside that window, a tax professional can help you determine whether filing those older returns works for or against you financially.

Voluntarily filing six years of back returns is often the minimum needed to stop active IRS collection activity and qualify for installment agreements or other payment options.

Here is a quick reference for standard IRS filing thresholds by filing status. You were required to file if your gross income exceeded these amounts:

| Filing Status | 2023 Threshold | 2022 Threshold | 2021 Threshold |

|---|---|---|---|

| Single (under 65) | $13,850 | $12,950 | $12,550 |

| Married Filing Jointly (both under 65) | $27,700 | $25,900 | $25,100 |

| Head of Household (under 65) | $20,800 | $19,400 | $18,800 |

| Self-Employed (any status) | $400 net | $400 net | $400 net |

How to check your own filing history

Pulling your IRS account transcript is the fastest way to confirm which years you actually filed. Log into your IRS online account at IRS.gov and look for a Tax Return Transcript for each year in question. If no transcript appears, the IRS has no record of a filed return for that year. Your account will also show any SFRs the IRS assessed on your behalf, which appear as a balance due without a corresponding filed return from you.

Getting unfiled tax returns help starts with building this clear list of missing filing years. Once you know exactly which years need returns, you can move forward systematically with gathering the income records you need.

Step 2. Collect your income and deduction records

Once you know which years you need to file, your next task is gathering the actual financial records for each one. This step often feels overwhelming, but breaking it down by document type makes it manageable. For each missing tax year, you need two categories of information: proof of every income source you received, and documentation of any deductions or credits you plan to claim. Missing either category means you either underreport income (which creates legal exposure) or overpay taxes you don't actually owe.

Income documents to track down

Start by listing every source of money you received in each tax year. Employers, banks, and financial institutions are required to keep records for several years, so you can often request duplicate copies of documents you no longer have. Contact your former employers directly for W-2 reissues, and reach out to financial institutions for 1099 forms covering interest, dividends, or distributions.

Common income documents you need for each missing year include:

- W-2: wages and salary from each employer

- 1099-NEC or 1099-MISC: freelance, contract, or self-employment income

- 1099-INT: bank interest income

- 1099-DIV: dividend income from investments

- 1099-B: proceeds from stock or asset sales

- 1099-R: retirement account distributions or pension income

- 1099-G: unemployment compensation or state tax refunds

- Schedule K-1: income passed through from a partnership, S-corp, or trust

If you cannot locate original documents, the IRS Wage and Income Transcript (covered in the next step) will show most of what third parties reported under your Social Security number.

Deduction records worth gathering

Deductions are what most people lose when they ignore unfiled tax returns help and let the IRS file a Substitute for Return instead. An SFR gives you the standard deduction at best and ignores everything else. Pulling your own deduction records lets you claim every dollar you're entitled to, which can dramatically lower what you owe.

Gather the following for each tax year where applicable:

- Mortgage interest statements (Form 1098) from your lender

- Charitable contribution receipts for donations over $250

- Business expense records such as receipts, mileage logs, and invoices

- Medical expense documentation if costs exceeded the IRS threshold for that year

- Student loan interest statements (Form 1098-E)

- Self-employment health insurance premium records

Organize these by year in separate folders, either physical or digital. A clear, year-by-year system saves significant time when you or a tax professional begin preparing the actual returns.

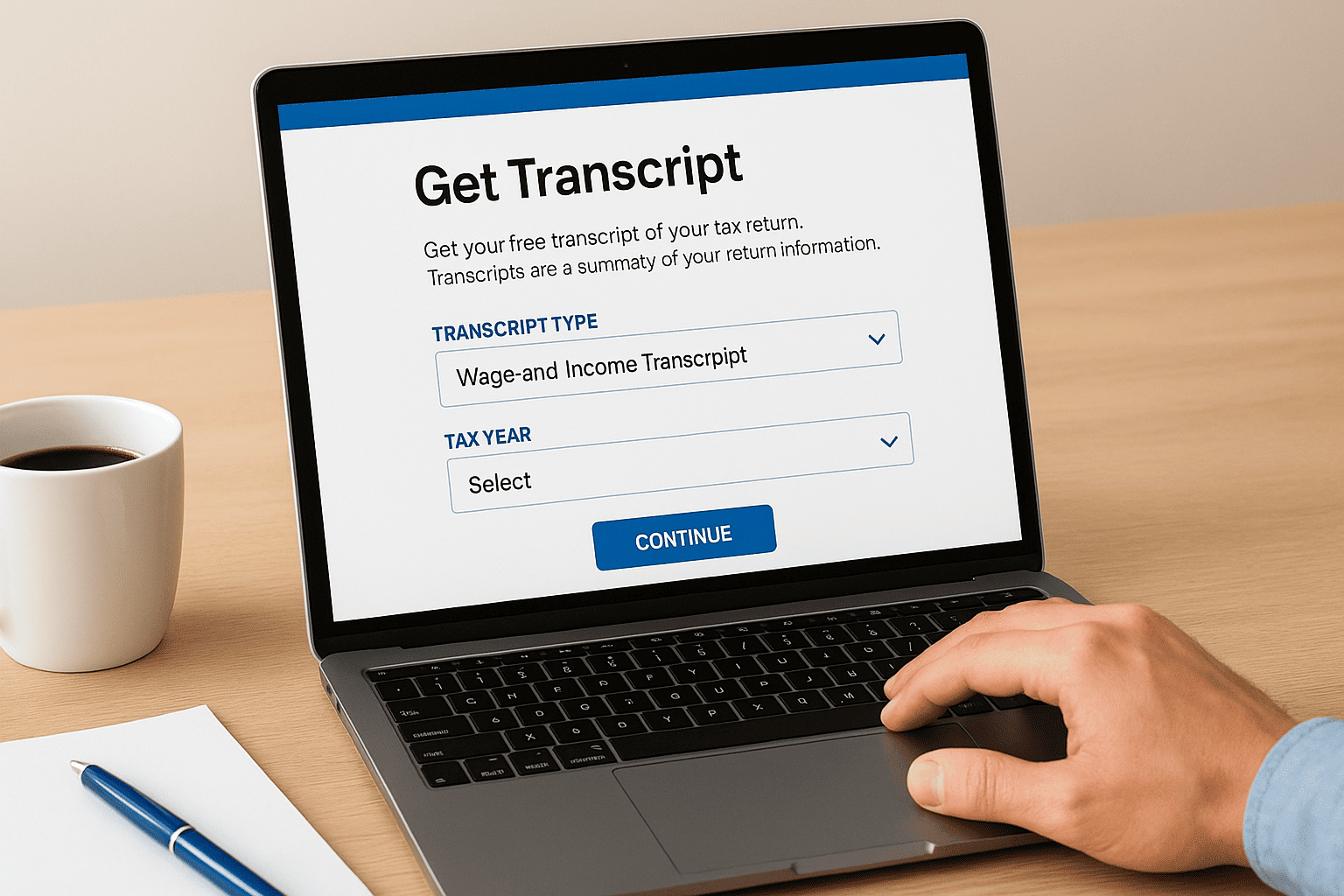

Step 3. Get IRS wage and income transcripts

Even if you have lost every W-2 and 1099 from years past, the IRS keeps records of what third parties reported under your Social Security number. Wage and Income Transcripts pull together all of that data into one document per tax year, covering employers, banks, brokerages, and any other entity that submitted information returns to the IRS. Getting these transcripts is one of the most reliable parts of finding missing income information when gathering records for unfiled tax returns help.

How to request your transcripts online

The fastest method is through the IRS's Get Transcript tool at IRS.gov. You create or log into an existing IRS account, select "Wage and Income Transcript," and choose the tax year you need. The IRS makes these transcripts available online for the previous 10 tax years, which covers most of the years you are likely to need. Download a separate transcript for each missing year and save each one in the year-by-year folder system you built in Step 2.

Wage and Income Transcripts show what the IRS already knows about your income, so any return you file needs to account for every item listed or you risk receiving an immediate discrepancy notice.

One important limitation to be aware of: transcripts for the most recent tax year may not be fully populated until late summer, since many third-party filers have until March 31 to submit electronic information returns. If you are filing for a very recent year, wait a few extra months before assuming the transcript is complete rather than filing with incomplete data.

How to request transcripts by mail

If you cannot verify your identity online, you can submit Form 4506-T (Request for Transcript of Tax Return) by mail or fax. The IRS typically processes these requests within 5 to 10 business days, and you can download the form directly from IRS.gov. Request one form submission per transcript type, and list each tax year you need on Line 9.

Fill in the following fields on Form 4506-T:

- Line 1a: Your full legal name as it appears on your tax return

- Line 2: Your Social Security Number

- Line 3: Your current mailing address

- Line 6: Check the box for "Wage and Income Transcript"

- Line 9: Enter each tax year needed (for example, 12/31/2021)

Send the completed form to the IRS address listed in the form's instructions for your state.

Step 4. Prepare accurate prior-year tax returns

With your transcripts and records in hand, you are ready to prepare each missing return. The most important rule here is to use the tax forms from the actual year you are filing for, not the current year's forms. The IRS requires prior-year returns to be filed on the forms that were in effect during that tax year, because deduction limits, credit amounts, and standard deduction figures all change annually.

Use prior-year tax forms and software

Prior-year tax forms are available directly on the IRS website at IRS.gov under the Forms and Publications section. You can download Form 1040 for each specific year along with any supporting schedules you need, such as Schedule C for self-employment income or Schedule A for itemized deductions. If you prefer to use tax software, note that most commercial software does not support filing for years older than three years, so you may need to prepare older returns manually using the downloaded IRS forms.

Filing on the wrong year's form can cause the IRS to reject your return or flag it for manual review, which adds processing delays to an already slow resolution process.

Work through each return year by year

Getting real unfiled tax returns help means treating each year as its own separate project rather than trying to complete everything at once. Start with the oldest year you need to file, since that year's refund or balance due can sometimes affect subsequent years through carryforward provisions like net operating losses or capital loss carryovers.

For each year, work through these steps in order:

- Enter all income from your Wage and Income Transcript and any additional records you gathered

- Select your correct filing status for that specific year based on your household situation at the time

- Apply the standard deduction for that year's filing status, or itemize if your documented deductions exceed it

- Claim all credits you qualify for, including the Earned Income Tax Credit, Child Tax Credit, or education credits

- Calculate your tax liability or refund and verify the math before moving to the next year

Double-check before you finalize

Before you set any return aside as ready to file, compare your reported income line by line against your Wage and Income Transcript. Any discrepancy between what you report and what the IRS already has on record will trigger a notice. Check your Social Security number, your name, and your address on every return as well, since a data entry error on a prior-year return can delay processing by months.

Step 5. File each return to the correct IRS address

Once each return is complete and double-checked, you need to mail it to the right IRS processing center. Prior-year returns cannot be e-filed through most standard tax software, which means the overwhelming majority of back returns must go out by paper mail. Sending a return to the wrong address delays processing significantly, since the IRS must then manually reroute it, adding weeks or months to your resolution timeline.

Why you generally cannot e-file prior-year returns

The IRS e-file system only accepts returns for the current tax year and, in some cases, the immediately prior year. If you are filing for 2022 or earlier, you almost certainly need to submit a paper return. This is one of the most common frustrations people encounter when seeking unfiled tax returns help on their own, since they expect to use the same software process as a current-year filing. Each paper return must be signed and dated before mailing, and a return without a signature is treated as unfiled regardless of whether it arrives at the correct address.

Never mail multiple years of back returns in a single envelope. The IRS requires each tax year to be submitted separately so returns reach the correct department and get processed individually.

Where to mail prior-year returns

The correct IRS mailing address depends on your state of residence and whether you are including a payment. The IRS updates these addresses periodically, so always verify the current address for your state directly on the IRS.gov "Where to File" page before mailing. Below is a sample of common destinations for individual Form 1040 filers:

| State of Residence | No Payment Enclosed | Payment Enclosed |

|---|---|---|

| California, Oregon, Washington | IRS, Fresno, CA 93888-0002 | IRS, Fresno, CA 93888-0102 |

| Texas, Louisiana, Mississippi | IRS, Austin, TX 73301-0002 | IRS, Austin, TX 73301-0102 |

| New York, New Jersey, Connecticut | IRS, Kansas City, MO 64999-0002 | IRS, Kansas City, MO 64999-0102 |

| Florida, Georgia, South Carolina | IRS, Atlanta, GA 39901-0002 | IRS, Atlanta, GA 39901-0102 |

How to protect yourself after mailing

Always send each return using certified mail with return receipt through the United States Postal Service. This gives you a postmarked timestamp and a delivery confirmation the IRS cannot dispute. Keep copies of every return you mail, along with the certified mail receipts, in a dedicated file. If the IRS later claims it never received a return, your mailing proof is the only documentation that protects you.

Step 6. If you owe and cannot pay in full

Filing your back returns is the right move even if you cannot pay the full balance right now. The IRS separates the obligation to file from the obligation to pay, so submitting your returns immediately stops the failure-to-file penalty from growing, regardless of whether a check comes with them. The failure-to-file penalty is ten times more expensive per month than the failure-to-pay penalty, so getting your returns in as soon as possible saves real money even when your bank account is empty.

Filing without payment is always better than not filing at all. The IRS will work with you on what you owe, but it cannot offer you any resolution options until your returns are on record.

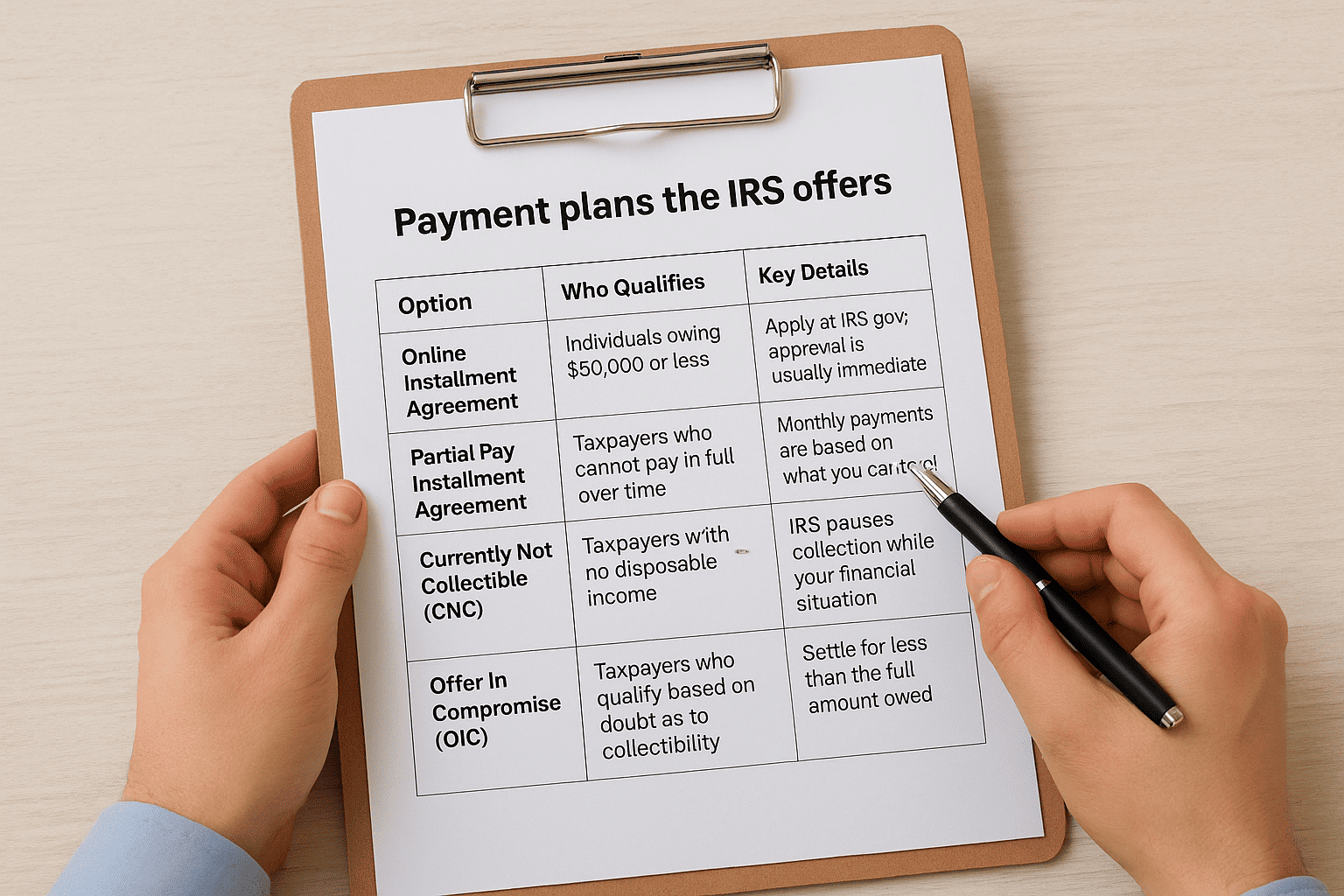

Payment plans the IRS offers

Once your back returns are filed and processed, the IRS makes several formal payment options available depending on how much you owe and your current financial situation.

| Option | Who Qualifies | Key Details |

|---|---|---|

| Online Installment Agreement | Individuals owing $50,000 or less | Apply at IRS.gov; approval is usually immediate |

| Partial Pay Installment Agreement | Taxpayers who cannot pay in full over time | Monthly payments are based on what you can actually afford |

| Currently Not Collectible (CNC) | Taxpayers with no disposable income | IRS pauses collection while your financial situation is reviewed |

| Offer in Compromise (OIC) | Taxpayers who qualify based on doubt as to collectibility | Settle for less than the full amount owed |

How to request a payment plan

The fastest way to set up a payment plan is through the IRS Online Payment Agreement tool at IRS.gov. If you owe $50,000 or less in combined tax, penalties, and interest, you can apply directly without speaking to an agent. The system walks you through selecting a monthly payment amount and start date without requiring a call to the IRS.

For balances above $50,000, or if you are pursuing an Offer in Compromise, you need to submit Form 9465 (Installment Agreement Request) or Form 656 (Offer in Compromise) by mail. Both forms are available directly at IRS.gov. When seeking unfiled tax returns help, a CPA or Enrolled Agent can evaluate which option gives you the best financial outcome before you commit to any arrangement with the IRS.

Step 7. Reduce penalties and avoid collections

Filing your back returns gets you into compliance, but it does not automatically erase the penalties and interest that built up while those returns were missing. The IRS offers formal penalty relief programs that many taxpayers never pursue simply because they do not know they exist. Taking the time to request relief after you file can significantly reduce the total amount you owe, and in some cases, the IRS will remove the failure-to-file penalty entirely.

First-time penalty abatement

First-Time Penalty Abatement (FTA) is the most accessible penalty relief option the IRS offers, and you do not need to prove hardship to qualify. You simply need a clean compliance history: no penalties assessed in the three tax years before the year you are requesting relief for, all required returns filed or on extension, and any tax owed paid or arranged through an installment agreement. If you meet those criteria, the IRS will remove the failure-to-file and failure-to-pay penalties for that year.

First-time penalty abatement is not automatic. You must request it directly, either by calling the IRS at 1-800-829-1040 or by submitting a written request to the address on your notice.

You can make the FTA request by phone after your return has been processed and a balance appears on your account. Have your tax identification number, the specific tax year, and the penalty amount ready before you call. The IRS representative can approve the abatement during the same call if your account history qualifies.

Reasonable cause penalty relief

If you do not qualify for first-time abatement, you can still request reasonable cause relief by explaining the specific circumstances that prevented you from filing on time. The IRS evaluates these requests case by case, and the burden is on you to provide documentation that supports your explanation.

Qualifying circumstances the IRS recognizes include:

- Serious illness or injury affecting you or an immediate family member

- A natural disaster that destroyed your records or made filing impossible

- Demonstrated reliance on incorrect advice from a tax professional

- Death of a close family member during the filing period

How to stop IRS collection actions

Once your returns are filed and you have a payment arrangement in place, the IRS is required to suspend most active collection activity such as wage garnishments and bank levies. If a levy is already in place, you can request its release by submitting Form 12153 (Request for a Collection Due Process Hearing) within 30 days of receiving the levy notice. Getting unfiled tax returns help from an Enrolled Agent gives you someone who can contact the IRS directly on your behalf to expedite that release while your case is being resolved.

When to get professional help with unfiled returns

Filing one or two missing returns on your own is manageable if your income came from a single employer and your financial situation was straightforward. However, many people seeking unfiled tax returns help are dealing with situations that go well beyond a simple W-2 and standard deduction. If your case involves multiple missing years, business income, IRS notices already in play, or significant balances due, working with a CPA or Enrolled Agent is not just convenient, it is often the difference between a bad outcome and a manageable one.

Signs your situation is too complex to handle alone

Certain circumstances make self-filing a genuine risk rather than just a hassle. The cost of getting it wrong, whether through missed deductions, incorrect income reporting, or filing on the wrong form, typically exceeds whatever you might spend on professional fees. If any of the following apply to your situation, you should get qualified help before you mail a single return:

- You have five or more years of unfiled returns that need to be prepared and submitted

- You received IRS notices, a notice of deficiency, or a levy notice before you started filing

- Your income included self-employment earnings, rental property, investments, or foreign accounts

- The IRS has already filed a Substitute for Return for one or more of your missing years

- You face a combined tax debt across years exceeding $25,000

- Your situation involves potential criminal exposure, such as willful non-filing over many years

An Enrolled Agent has the legal authority to represent you directly before the IRS, which means they can speak to IRS agents on your behalf, respond to notices, and negotiate payment arrangements without you ever picking up the phone.

What a CPA or Enrolled Agent does that software cannot

A qualified tax professional does more than fill in boxes. They review your entire financial history across all missing years to identify deductions, credits, and elections you would likely miss on your own. They also know how to sequence the filing of multiple back returns to minimize total penalties and avoid triggering additional scrutiny.

Beyond preparation, a CPA or Enrolled Agent can negotiate directly with the IRS on penalty abatement, installment agreements, and Offers in Compromise once your returns are filed. At Tax Experts of OC, our team handles exactly this kind of multi-year resolution work for clients in all 50 states, starting with a free 30-minute consultation so you understand your options before committing to anything.

Next steps

You now have a complete roadmap for resolving years of missing returns, from confirming which years you owe to reducing penalties after you file. The most important thing you can do right now is take the first concrete step: pull your IRS transcripts, list your missing years, and start building your records folder. Every month you delay adds more penalty charges to an already growing balance, so starting today costs you less than starting next month.

If your situation involves multiple missing years, IRS notices, or business income, getting qualified unfiled tax returns help from a licensed professional protects you from costly mistakes. At Tax Experts of OC, our CPAs and Enrolled Agents handle multi-year back filing and IRS negotiations for clients across all 50 states. Schedule your free 30-minute consultation today and find out exactly where you stand before you make another move: talk to a tax resolution expert.