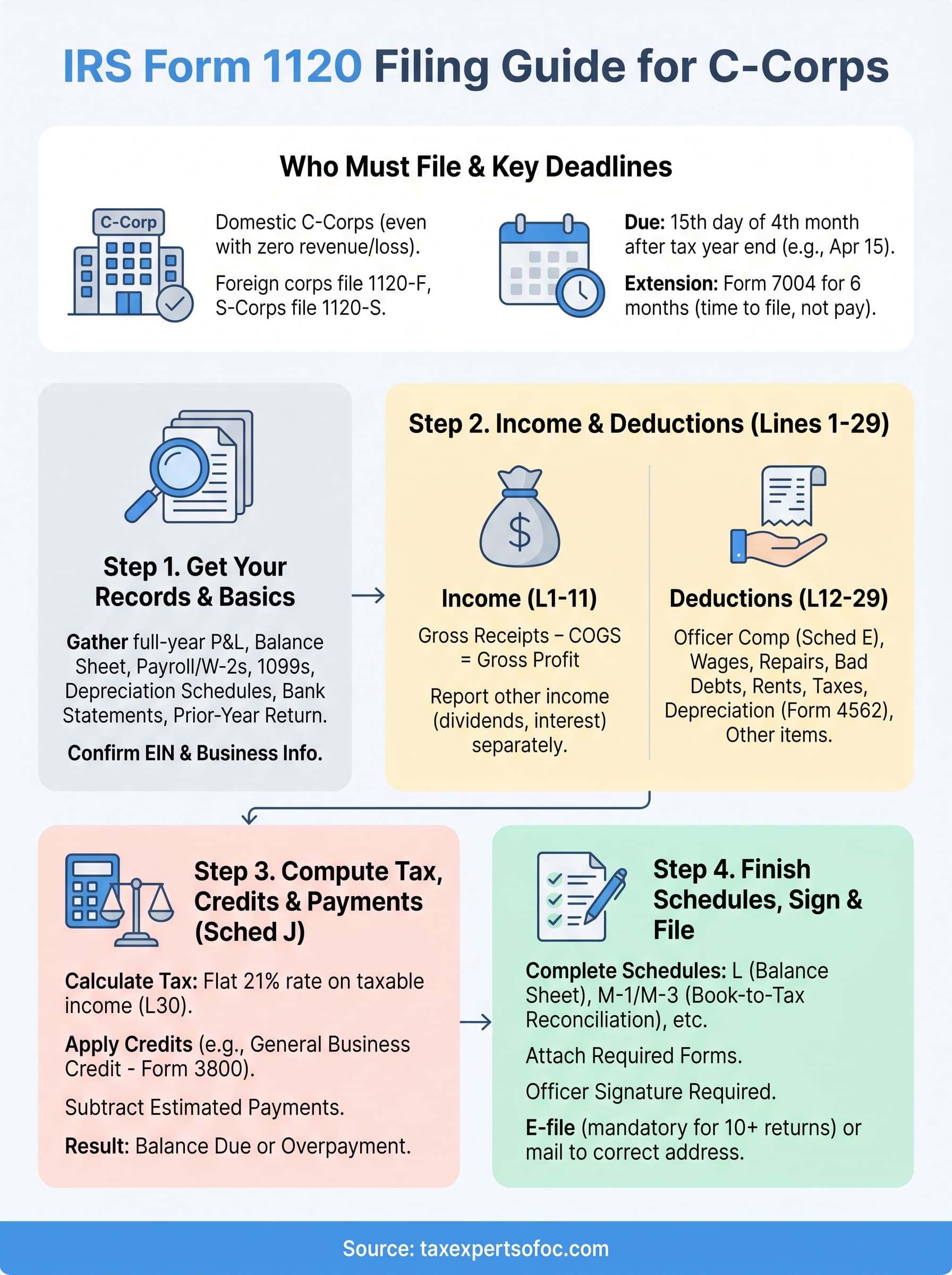

Every C corporation operating in the United States must file a federal income tax return with the IRS each year, and that means working through IRS Form 1120 instructions to report income, claim deductions, and calculate the tax owed. Whether this is your first filing or you've done it before, the form has enough moving parts to trip up even experienced business owners.

Form 1120 covers everything from gross receipts and cost of goods sold to officer compensation and tax credits. Miss a schedule, enter a figure on the wrong line, or overlook a required attachment, and you could face penalties, processing delays, or unwanted IRS attention. The official instructions alone run over 30 pages, which is why a clear, simplified walkthrough matters.

At Tax Experts of OC, our CPAs and Enrolled Agents prepare and review corporate returns for businesses across all 50 states. We built this guide to give you a practical, line-by-line understanding of Form 1120, what each section asks for, which schedules apply to your situation, and how to file accurately and on time for the current tax year.

What Form 1120 is and who must file

Form 1120, officially titled the U.S. Corporation Income Tax Return, is the federal tax form that C corporations use to report their income, deductions, credits, and calculated tax liability to the IRS each year. The form covers everything from gross receipts and cost of goods sold to officer salaries and depreciation. Unlike a pass-through entity, a C corporation pays income tax at the corporate level, which is why it requires its own dedicated return rather than passing income to owners' personal returns.

The IRS Form 1120 instructions also govern several related schedules attached to the main form, such as Schedule C for dividends and distributions, Schedule J for computing the tax, and Schedule K for additional information. Understanding the full scope of the form before you start filling it out saves you from having to backtrack, amend, or refile.

Who must file Form 1120

Every domestic C corporation incorporated in the United States must file Form 1120, regardless of whether it earned any income during the tax year. Even a corporation with zero revenue or one operating at a net loss still has a filing obligation. The IRS does not exempt inactive corporations from this requirement unless the entity has been formally dissolved with the state and the IRS.

A corporation that was formed but never opened for business still owes a Form 1120 filing for any tax year it remains legally incorporated.

Foreign corporations doing business in the United States file Form 1120-F instead, and S corporations file Form 1120-S. Confirm your entity classification before you proceed, since filing the wrong form creates processing delays and potential penalties. The table below shows which return applies to common entity types:

| Entity Type | Required Federal Return |

|---|---|

| C Corporation (domestic) | Form 1120 |

| S Corporation | Form 1120-S |

| Foreign Corporation (U.S. source income) | Form 1120-F |

| Partnership | Form 1065 |

| Single-member LLC (default status) | Schedule C on Form 1040 |

Key filing deadlines you need to know

The standard due date for Form 1120 is the 15th day of the fourth month following the close of the corporation's tax year. For a calendar-year corporation, that means the return is due April 15. If your corporation runs on a fiscal year ending on a date other than December 31, count forward four months from your year-end to find the correct deadline.

You can request a six-month extension by filing Form 7004 before the original due date, but the extension only gives you additional time to file, not additional time to pay. Any tax owed is still due on the original deadline. Underpayment of tax after that date accrues interest and may trigger a failure-to-pay penalty, so estimate your liability carefully before submitting the extension request. The current version of Form 1120 and the official instructions are available directly from the IRS website, where prior-year versions are also downloadable if you need to catch up on unfiled returns.

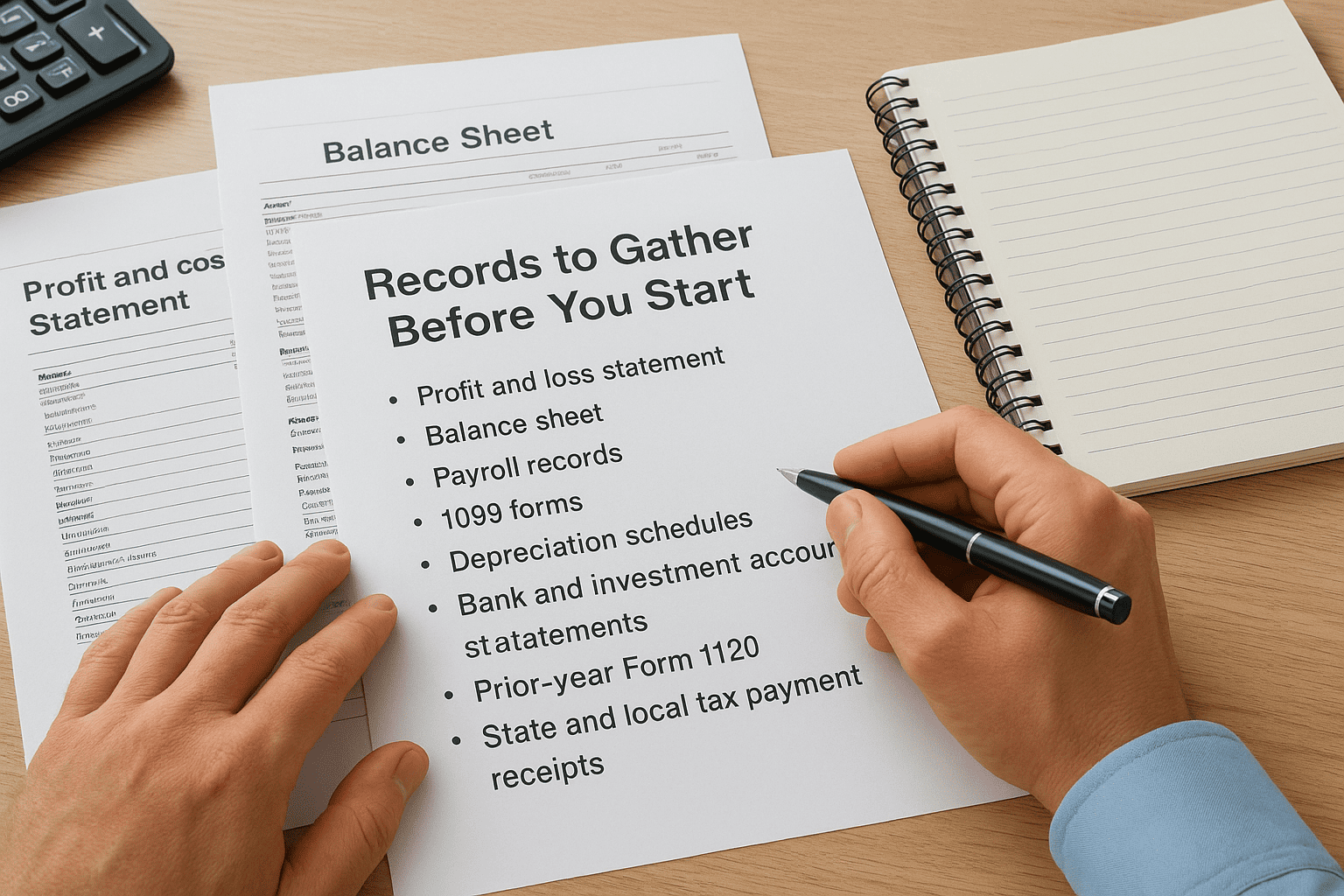

Step 1. Get your records and filing basics

Before you open the form, pull together everything your return depends on. The irs form 1120 instructions are clear that corporations must report on a full-year basis, so you need complete financial records from the first day to the last day of your tax year. Starting with organized records cuts your preparation time significantly and reduces the chance of errors.

Records to gather before you start

Having the right documents in front of you before you touch Line 1 makes the entire process faster. Missing a single figure mid-way through forces you to stop, track down records, and risk entering a placeholder that gets overlooked at review.

Collect the following before you begin:

- Profit and loss statement for the full tax year

- Balance sheet as of the last day of the tax year

- Payroll records, including W-2s issued to employees and officer compensation summaries

- 1099 forms received for interest, dividends, or other income

- Depreciation schedules for all assets placed in service

- Bank and investment account statements reconciled to your books

- Prior-year Form 1120 for reference on carryforward items like net operating losses or capital loss carryovers

- State and local tax payment receipts, which are deductible on the federal return

Reconcile your books to your bank statements before you start filling out the form. Discrepancies found mid-filing create delays that are harder to fix under deadline pressure.

Filing identification details to confirm

The top section of Form 1120 asks for basic identification data, and errors here cause IRS processing rejections. Verify the following details before entering them on the form.

Confirm your Employer Identification Number (EIN) matches what the IRS has on file exactly. Check that the corporation's legal name matches the name registered with the IRS when the EIN was assigned. Enter the correct tax year dates, the incorporation state, and the business activity code from the IRS Principal Business Activity Codes list included in the official instructions.

Step 2. Fill out income and deductions

Lines 1 through 29 of Form 1120 cover the bulk of your corporate activity for the year. The irs form 1120 instructions walk through each line in order, but understanding the logic behind the two sections, income and deductions, helps you move through them faster and with fewer mistakes.

Reporting income on Lines 1 through 11

Line 1a is where you enter gross receipts or sales from your core business operations, then subtract returns and allowances on Line 1b to reach net sales on Line 1c. If your corporation sells physical products, Line 2 captures your cost of goods sold, which flows in from Schedule A. Subtract cost of goods sold from net sales to arrive at your gross profit on Line 3.

The remaining income lines, 4 through 10, collect other income items including dividends, interest, rents, royalties, and capital gains. Enter each type on its designated line rather than combining them, since the IRS matches these figures against third-party reporting documents like 1099s.

Report every income category on a separate line. Combining income types is a common error that triggers IRS correspondence and delays processing.

Claiming deductions on Lines 12 through 29

Officer compensation goes on Line 12 and must match the detail you provide on Schedule E, which requires each officer's name, Social Security number, percentage of stock ownership, and compensation amount. Salaries and wages for all other employees go on Line 13, separate from officer pay.

Lines 14 through 26 cover specific deduction categories. Use the table below as a quick reference for the most common lines:

| Line | Deduction Category |

|---|---|

| 14 | Repairs and maintenance |

| 15 | Bad debts |

| 16 | Rents |

| 17 | Taxes and licenses |

| 20 | Depreciation (from Form 4562) |

| 26 | Other deductions (attach schedule) |

Depreciation on Line 20 must match your Form 4562, which you attach to the return. Any amount you enter on Line 26 for other deductions requires a separate schedule listing each item and its dollar amount, so prepare that itemized list before you finalize this section.

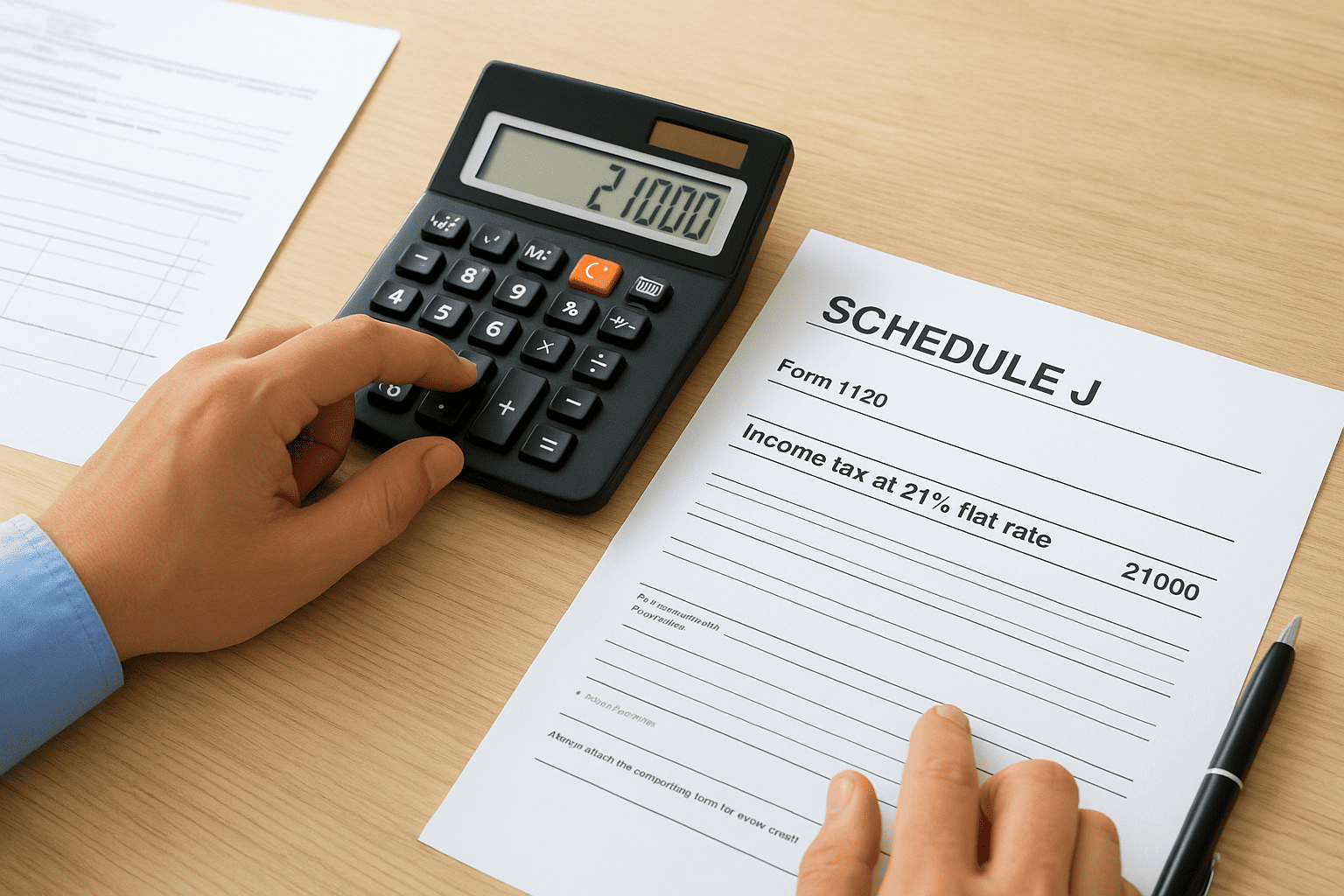

Step 3. Compute tax, credits, and payments

Once you finish the income and deductions section, you move into Schedule J, where the irs form 1120 instructions direct you to calculate the actual tax your corporation owes. Your taxable income from Line 30 feeds into this computation, and credits along with prior payments reduce your final balance due.

Calculating your tax on Schedule J

Schedule J walks you through computing the income tax on your corporation's taxable income. The current flat corporate tax rate is 21 percent, established by the Tax Cuts and Jobs Act of 2017. Multiply your taxable income from Line 30 by 21 percent and enter the result on Schedule J, Line 2. If your corporation owes the alternative minimum tax or other additional taxes, those amounts stack on top of the base tax and feed into Line 9.

Use this breakdown as a quick reference for the key Schedule J lines:

| Schedule J Line | What Goes Here |

|---|---|

| Line 2 | Income tax at 21% flat rate |

| Line 5a | Base erosion minimum tax (if applicable) |

| Line 9 | Total tax (sum of all applicable lines) |

Applying credits and payments

Tax credits reduce the tax you calculated on Schedule J before you determine what you owe. Common credits that flow into this section include the general business credit from Form 3800 and the credit for prior-year minimum tax. Enter each credit on its designated line and carry the total forward to reduce your computed tax figure.

Always attach the supporting form for every credit you claim. Missing documentation is one of the most common reasons the IRS adjusts corporate returns after filing.

After credits, report estimated tax payments your corporation made throughout the year on Schedule J, Line 14. Include any overpayment applied from the prior-year return as well. Subtract total payments from total tax to determine whether your corporation carries a balance due or an overpayment. A balance due goes on Line 35, while an overpayment goes on Line 36, where you also indicate whether you want it refunded or credited to the next year's estimated tax.

Step 4. Finish schedules, sign, and file

With your income, deductions, and tax computation complete, the final step in following the irs form 1120 instructions is to verify your schedules, apply any required attachments, and submit a properly signed return. Rushing this part is where many corporations introduce errors that trigger IRS correspondence months after filing.

Complete the remaining required schedules

Several schedules may apply to your corporation depending on its activity during the year. Schedule L is a balance sheet comparison showing assets, liabilities, and shareholder equity at the beginning and end of the tax year. Schedule M-1 reconciles the difference between your book income and your taxable income, which the IRS uses to verify that your return is internally consistent.

If your corporation has total assets of $10 million or more, you must complete Schedule M-3 instead of Schedule M-1, and additional disclosure requirements apply.

Use this checklist to confirm which schedules you need to attach before filing:

- Schedule C: Required if your corporation received dividends

- Schedule E: Required to detail officer compensation from Line 12

- Schedule J: Always required to compute the tax

- Schedule L: Required unless the corporation is exempt under the total receipts and assets threshold

- Schedule M-1 or M-3: Required based on total asset size

- Form 4562: Required if you claimed depreciation on Line 20

- Form 3800: Required if you claimed any general business credit

Sign and submit your return

A Form 1120 is not valid without a signature from a corporate officer authorized to sign, typically the president, vice president, treasurer, or chief financial officer. The officer must sign and date the return under penalty of perjury, and if a paid preparer completed the return, that preparer must also sign and include their Preparer Tax Identification Number (PTIN).

You can file electronically through the IRS e-file system, which is required for corporations filing 10 or more returns annually. Paper filers must mail the completed return to the IRS address listed in the instructions for your state. Confirm the correct mailing address in the current-year instructions before sending, as addresses vary by state and total asset size.

Wrap Up and When To Get Help

Following the irs form 1120 instructions from start to finish requires accurate records, careful attention to each schedule, and a valid signature before you submit. If your corporation has multiple income streams, credits, or prior-year carryforwards, the complexity adds up quickly and small mistakes can become expensive problems.

Consider working with a professional when your return involves officer compensation reporting, depreciation recapture, back taxes, or an IRS notice. Missing schedules and mismatched figures are among the most common triggers for IRS correspondence, and fixing those problems after the fact costs significantly more time and money than getting the return right the first time.

The team at Tax Experts of OC includes CPAs and Enrolled Agents who prepare and review corporate returns for businesses across all 50 states. If you want accurate filing and qualified professional representation if the IRS has questions, schedule a free consultation with Tax Experts of OC today.