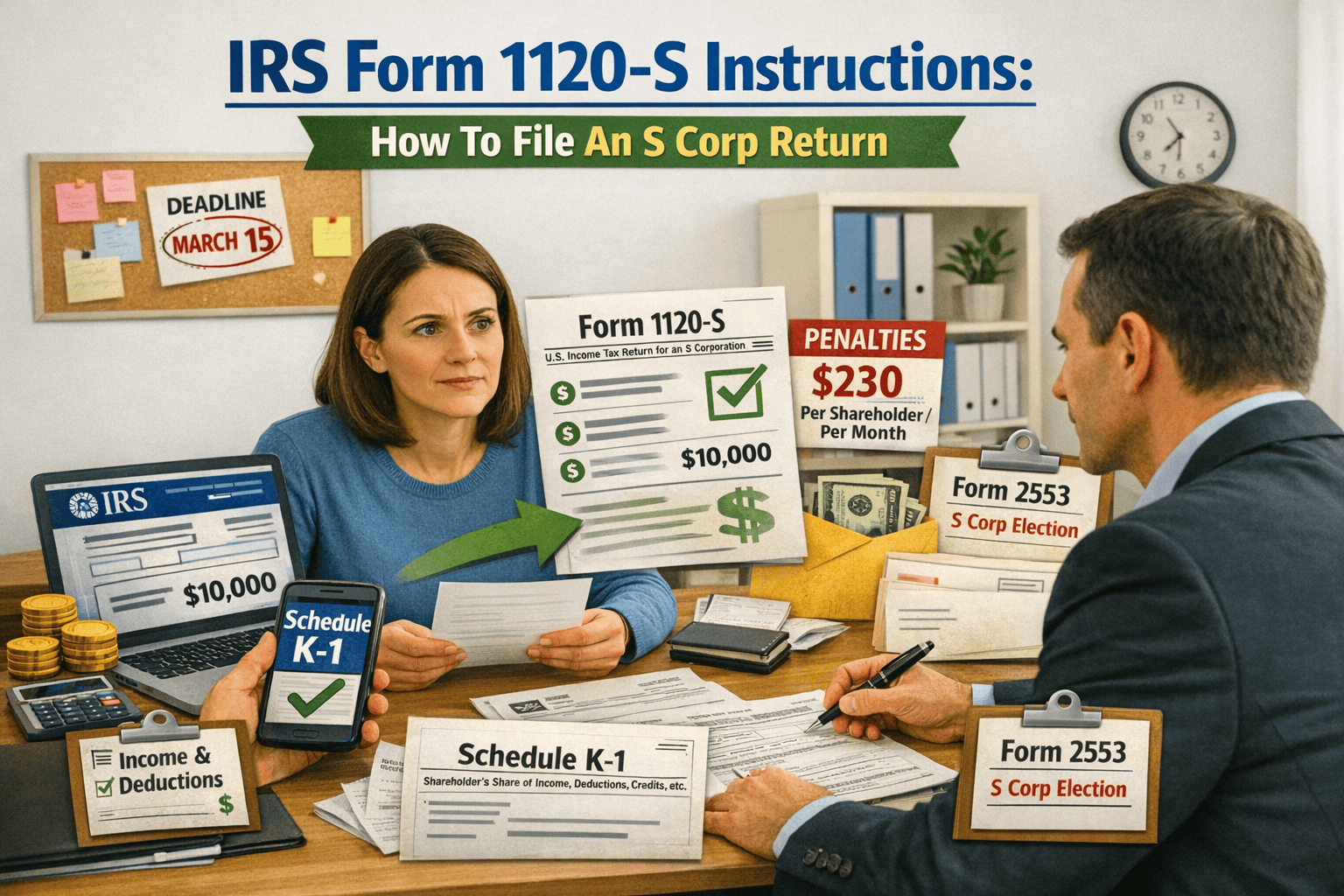

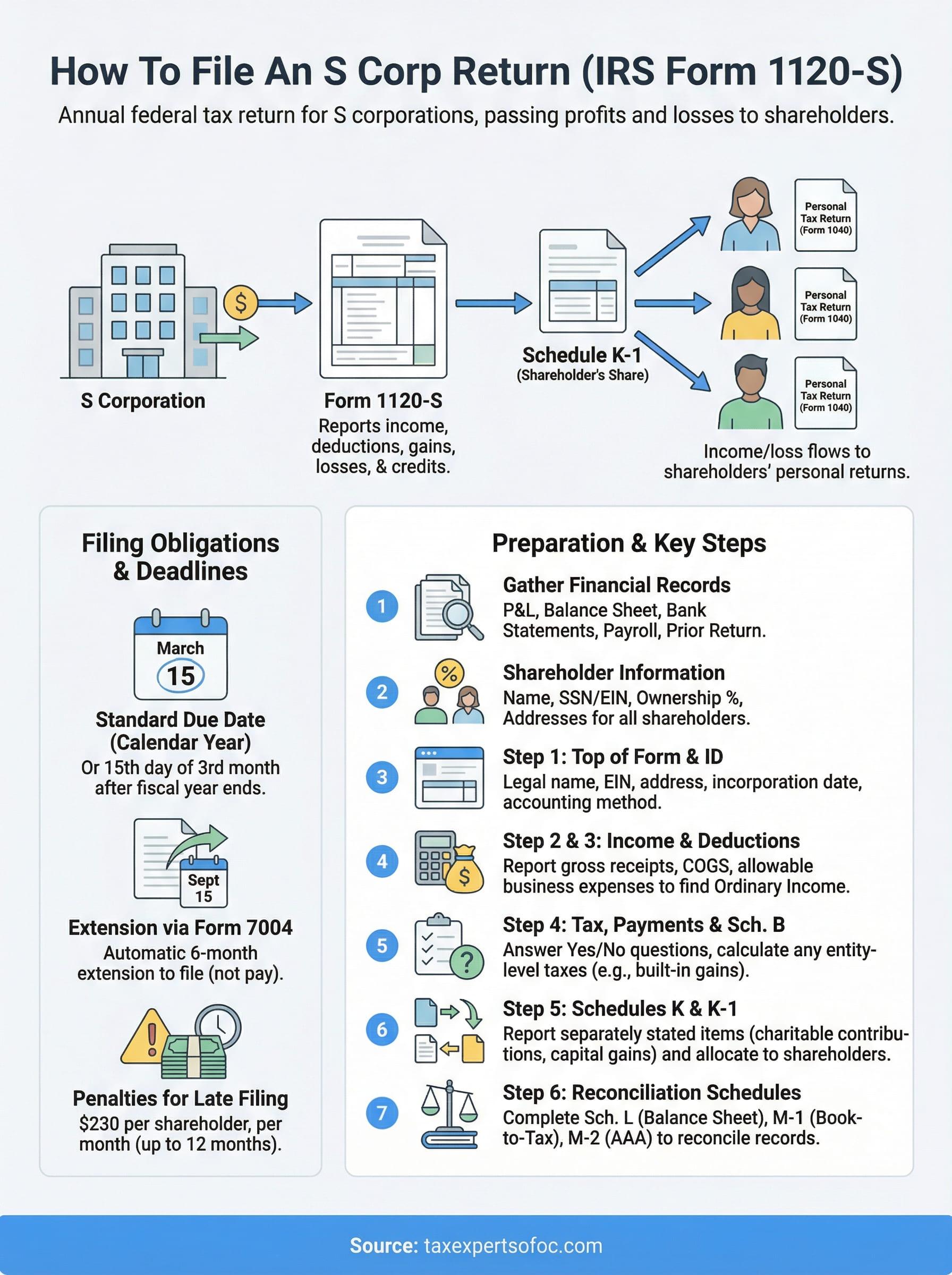

Every S corporation operating in the United States must file a federal return with the IRS each year, and that means working through IRS Form 1120-S instructions line by line. Whether your S corp generated a profit, broke even, or posted a loss, the filing obligation doesn't go away. Miss the deadline or report something incorrectly, and the penalties add up fast, $230 per shareholder, per month, under current rules.

Form 1120-S is the document that reports your S corporation's income, deductions, gains, losses, and credits to the IRS. It's also the form that generates each shareholder's Schedule K-1, which flows directly into their personal tax returns. Getting it right matters not just for the business, but for every individual with a stake in it.

At Tax Experts of OC, our CPAs and Enrolled Agents prepare and file S corp returns for businesses across all 50 states. We work with S corporation owners year-round, handling everything from first-time filings to amended returns and IRS notices. This guide walks you through the form section by section, so you know exactly what's required and where each number goes.

What Form 1120-S is and when to file it

Form 1120-S is the annual federal tax return for S corporations, filed with the IRS to report the company's income, deductions, credits, and other financial activity for the tax year. Unlike a C corporation, an S corp doesn't pay federal income tax at the entity level. Instead, the corporation's profits and losses pass through to shareholders, who each report their allocated share on their own individual returns. Form 1120-S is the mechanism that makes that pass-through work correctly.

What the form actually does

The form has two main jobs. First, it calculates your S corporation's ordinary business income or loss, which is income from regular operations after subtracting eligible business expenses. Second, it separates out items that get special tax treatment, such as capital gains, rental income, Section 179 deductions, and charitable contributions. These separately stated items appear on Schedule K, and then flow to each shareholder through their individual Schedule K-1.

Each shareholder's K-1 shows their allocated share of every income and deduction category. That K-1 then gets reported on the shareholder's Form 1040, which is why errors on Form 1120-S ripple directly into personal tax returns. If you misclassify an item or omit a deduction on the corporate return, every shareholder's filing is affected.

The Schedule K-1 connects the S corporation return directly to each shareholder's personal taxes, so accuracy at the entity level is not optional.

Who must file and the S corp election

Any corporation with a valid S corporation election on file with the IRS must file Form 1120-S for every tax year the election remains in effect, even if the corporation had no income or activity during that year. The S corp election is made by filing Form 2553 with the IRS, and once approved, the 1120-S filing obligation starts immediately for that tax year.

Your obligation continues until the IRS formally terminates your S corp status. If your corporation loses its S election due to an eligibility violation, such as exceeding 100 shareholders or adding an ineligible owner, the IRS will treat the entity as a C corporation going forward. Following the IRS Form 1120-S instructions carefully each year helps you stay compliant and catch issues before they trigger an involuntary termination.

Filing deadlines and extension rules

The standard due date for Form 1120-S is March 15 for calendar-year S corporations. If your corporation uses a fiscal year, the return is due on the 15th day of the third month after the fiscal year ends. Missing this date triggers a penalty of $230 per shareholder per month for up to 12 months.

Filing Form 7004 before the original deadline gives you an automatic six-month extension, pushing your due date to September 15 for calendar-year filers. Keep in mind that an extension gives you more time to file, not more time to pay. If the corporation owes any taxes, such as the built-in gains tax or the excess net passive income tax, those amounts are still due by the original March 15 deadline.

| Filing scenario | Due date |

|---|---|

| Calendar-year S corp | March 15 |

| Calendar-year S corp with extension | September 15 |

| Fiscal-year S corp | 15th day of 3rd month after year-end |

| Fiscal-year S corp with extension | 15th day of 9th month after year-end |

What you need before you start

Before you open the form, gather everything you need in one place. Working through the IRS Form 1120-S instructions is much faster when you're not stopping to track down a missing number or reconcile a discrepancy mid-filing. Most errors on S corp returns come from incomplete records, not from misunderstanding the instructions themselves, so preparation is the most important step you can take.

Financial records and statements

Your starting point is a clean profit and loss statement and a reconciled balance sheet for the full tax year. These two documents drive the majority of what you enter on the return. Your P&L feeds the income and deduction sections, while your balance sheet populates Schedules L and M-2. If your books aren't finalized before you start, your return will reflect those gaps directly.

You'll also need the following records ready:

- Bank statements reconciled to your bookkeeping records for the full year

- Payroll records, including all W-2s filed and total wages paid to shareholder-employees

- Fixed asset schedule showing additions, disposals, and depreciation taken during the year

- Prior-year Form 1120-S to carry forward items such as unused losses or suspended deductions

- Loan records documenting any shareholder loans to or from the corporation

Shareholder basis tracking is one of the most commonly missed items in S corp filings, and overlooking it leads to incorrectly deducted losses on personal returns.

Shareholder information

You need complete and current information for every shareholder before you can prepare a single Schedule K-1. Each K-1 requires the shareholder's name, address, Social Security Number or EIN, and their exact ownership percentage for the tax year. If any shareholder's ownership changed during the year, document the specific transfer dates, because allocations must reflect the actual days each person held shares.

Pull together the following for each shareholder before you begin:

| Information needed | Where to find it |

|---|---|

| Full legal name | Corporate records or ownership agreement |

| SSN or EIN | Prior-year K-1 or onboarding documents |

| Ownership percentage | Stock ledger or shareholder agreement |

| Beginning and ending share count | Corporate minute book |

| Shareholder loans to the corporation | Loan agreements and bank records |

Having this table filled in for every shareholder keeps your K-1 allocations accurate from the start and prevents you from circling back to fix errors after you've already completed the rest of the return.

Step 1. Fill out the top of Form 1120-S

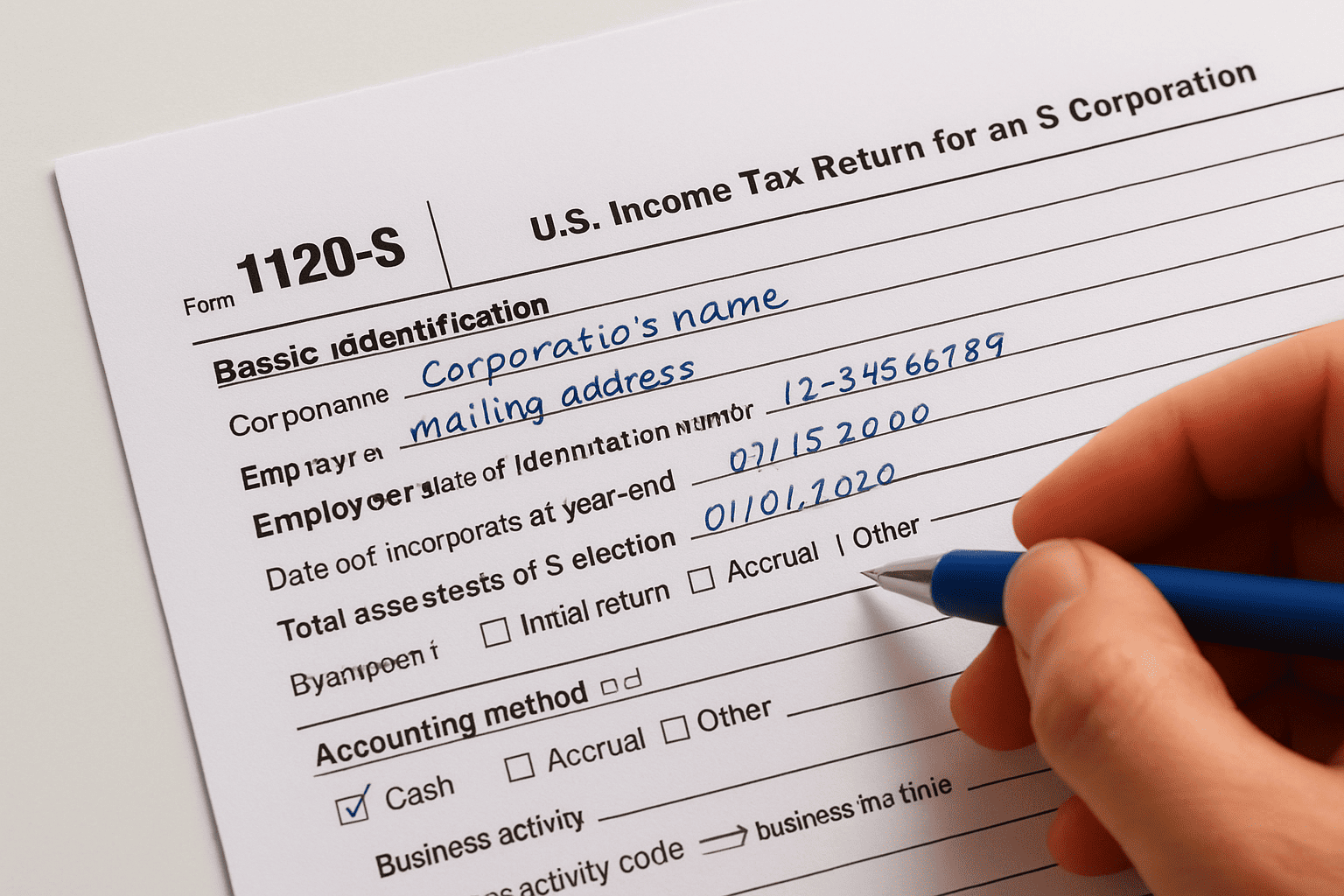

The top section of Form 1120-S collects identifying information about your corporation before you record a single dollar of income or expense. This part looks straightforward, but small errors here, such as a mismatched EIN or an incorrect tax year, can cause the IRS to reject the return or misapply your payment. Work through each field in order and cross-reference your details against your IRS CP 261 confirmation letter, which acknowledged your S election.

Basic identification fields

Enter your corporation's legal name exactly as it appears on file with the IRS, your mailing address, and your Employer Identification Number. If the corporation moved during the tax year, use the current address. Next, enter the date your corporation was incorporated and the total assets at year-end from your balance sheet. Total assets come directly from Schedule L, so if you haven't completed that schedule yet, leave this field blank and return to it after you finish the back of the form.

Below those fields, enter the date your S election became effective, which you can confirm on your CP 261 letter. If you cannot locate that letter, you can request a copy by calling the IRS Business and Specialty Tax line or by checking a prior-year return where this date was already recorded.

If your EIN on the return does not match what the IRS has on file, processing will stall and you may receive a notice before any tax liability is even reviewed.

Check boxes and accounting method

The next row of check boxes tells the IRS whether this is an initial return, final return, name change, address change, or amended return. Mark every box that applies. If you are filing an amended Form 1120-S, check that box and attach a written statement explaining what changed and why.

Following the IRS Form 1120-S instructions, you'll reach a field for your accounting method, either cash, accrual, or other. Choose the method your books actually use throughout the year, because it must match how you record income and expenses everywhere else on the return. Then enter your business activity code, a six-digit number that best describes your primary revenue source. A complete reference list appears directly in the Form 1120-S instruction booklet published by the IRS.

Step 2. Report income and cost of goods sold

Lines 1 through 6 on page one of Form 1120-S cover your corporation's total income, starting with gross receipts and working down through other income categories to produce a net income figure that feeds into the deductions section. Read through each line before entering numbers, because the IRS Form 1120-S instructions define terms like "gross receipts" more narrowly than you might expect.

Lines 1 through 6: gross receipts and other income

Line 1a is where you enter your corporation's total gross receipts or sales for the year, before returns and allowances. On line 1b, subtract any returns, allowances, or discounts your business granted to customers. The result on line 1c is your net receipts figure, which you carry into line 5 unless you have cost of goods sold to report first.

Lines 2 through 5 work together to get you to gross profit. Enter cost of goods sold on line 2 (from Schedule A on page 2), then calculate gross profit on line 3. Line 4 captures net gain or loss from Form 4797 if your corporation sold business property during the year. Line 5 combines other income sources such as interest, rents, or royalties that don't belong on Schedule K. Once you complete all these lines, add them up to arrive at your total income on line 6.

If you have any income that receives special tax treatment, such as capital gains or rental income from non-trading activity, do not enter it on lines 1 through 6. Those items belong on Schedule K.

Schedule A: cost of goods sold

If your S corporation sells physical products, you must complete Schedule A on page 2 before you can finish line 2. Schedule A walks you through your beginning inventory, purchases, labor, and other production costs, then subtracts ending inventory to produce your cost of goods sold figure.

You also need to select an inventory valuation method on Schedule A, either cost, lower of cost or market, or another approved method. Choose the method that matches your actual accounting practice and confirm it's consistent with prior years. If you changed methods, attach Form 3115 to the return and note the change on Schedule A. Consistency here protects you if the IRS questions your inventory reporting later.

Step 3. Enter deductions and compute ordinary income

Lines 7 through 20 on page one of Form 1120-S capture your S corporation's allowable business deductions, which you subtract from total income to arrive at ordinary business income or loss on line 21. This section is where most of the judgment calls happen, because not every expense your corporation paid during the year belongs here. Some items, such as charitable contributions and Section 179 deductions, are separately stated items that go on Schedule K instead, not in this deductions section.

Lines 7 through 20: allowable deductions

Work through each line in order, entering only amounts that qualify as ordinary and necessary business expenses under the IRS rules. Following the irs form 1120-s instructions carefully here prevents you from accidentally moving a Schedule K item into the deductions section, which would distort both the ordinary income calculation and every shareholder's K-1.

Here is a quick reference for the key deduction lines and what each one captures:

| Line | Deduction category | Notes |

|---|---|---|

| 7 | Compensation of officers | Shareholder-employees must receive reasonable W-2 wages |

| 8 | Salaries and wages | Exclude amounts already on line 7 |

| 9 | Repairs and maintenance | Routine repairs only; capitalize improvements |

| 10 | Bad debts | Accrual-method filers only in most cases |

| 12 | Taxes and licenses | Includes payroll taxes and state business taxes |

| 13 | Interest expense | Only business-purpose debt; personal interest is excluded |

| 14 | Depreciation | From Form 4562; exclude any Section 179 claimed on Schedule K |

| 17 | Pension and profit-sharing plans | Qualified retirement plan contributions for employees |

| 19 | Other deductions | Attach a separate schedule listing each item |

Line 7 is one of the most audited lines on the return, because the IRS scrutinizes whether shareholder-employees received reasonable compensation before any distributions were made.

Line 21: ordinary business income or loss

Once you've entered every allowable deduction on lines 7 through 20, add them together to get your total deductions figure. Subtract that total from the income on line 6, and the result is your ordinary business income or loss on line 21. A positive number means profit; a negative number is an ordinary loss.

This line 21 figure flows directly to Schedule K and then to each shareholder's K-1 as their share of ordinary business income or loss. Shareholders can only deduct their allocated loss to the extent they have sufficient basis in the corporation, so an accurate line 21 calculation has real consequences at the individual tax level.

Step 4. Complete tax, payments, and Schedule B

Page two of Form 1120-S contains Schedule B, a series of yes-or-no questions the IRS uses to collect additional information about your corporation's structure and activity. After finishing Schedule B, you'll move to the tax and payments section on page one, where you report any entity-level taxes your S corp owes and reconcile what you've already paid against your total liability. Most S corps end up with zero tax due here, but you still need to complete every applicable line.

Schedule B: Yes-or-No Questions

Schedule B runs from question 1 through question 17, and following the irs form 1120-s instructions means reading each question carefully before you mark your answer. Several questions have real filing consequences. For example, question 4 asks whether the corporation had more than one class of stock outstanding during the year. If you answer yes, your S election may be at risk, because having two classes of stock is a disqualifying event. Question 8 asks whether the corporation was a shareholder in a C corporation or owned a subsidiary, which triggers additional disclosure requirements.

Answering Schedule B questions inaccurately is one of the most common ways S corps invite IRS scrutiny, so confirm each answer against your corporate records before moving on.

Work through every question in order and attach any required statements when a question calls for one. If a question does not apply to your corporation, mark it accordingly rather than leaving it blank.

Entity-Level Taxes

Most S corporations pass all income through to shareholders and pay no federal income tax at the entity level. However, two situations do create a tax obligation directly on the S corp: the built-in gains tax and the excess net passive income tax. The built-in gains tax applies when your corporation converted from a C corp and sold appreciated assets within the recognition period, currently five years. The excess net passive income tax applies when your S corp has accumulated earnings and profits from C corp years and more than 25 percent of gross receipts comes from passive sources.

| Entity-level tax | When it applies | Form to use |

|---|---|---|

| Built-in gains tax | Asset sale within 5-year recognition period | Schedule D and Form 1120-S, line 22a |

| Excess net passive income tax | Passive income exceeds 25% of gross receipts with AE&P | Line 22c and supporting worksheet |

Enter any calculated tax amounts on lines 22a through 22e, then add estimated tax payments, prior-year overpayments applied, and tax deposited with Form 7004 on lines 23 through 26. Subtract total payments from total tax to reach the amount owed or the overpayment on lines 27 and 28.

Step 5. Prepare Schedule K and Schedule K-1s

Schedule K pulls together every separately stated item from your S corporation's activity for the year, and Schedule K-1 distributes each shareholder's allocated share of those items. You complete Schedule K on page three of Form 1120-S before you prepare any K-1s, because the K-1 totals must add up exactly to the Schedule K totals. If they don't match, the IRS will flag the discrepancy during processing.

What Schedule K covers

Schedule K runs through income, deductions, credits, and other items that receive special tax treatment at the shareholder level. The irs form 1120-s instructions break Schedule K into several categories, and each line feeds a corresponding box on every shareholder's K-1. Work through each category in order:

| Schedule K category | Examples |

|---|---|

| Ordinary business income or loss | Flows from line 21, page one |

| Rental income or loss | Passive rental activity net results |

| Interest, dividends, and royalties | Investment-type income |

| Capital gains and losses | Short-term and long-term transactions |

| Section 179 deduction | Elected expensing on qualifying assets |

| Charitable contributions | Cash and non-cash donations |

| Credits | Low-income housing, work opportunity, others |

Do not duplicate items on Schedule K that you already deducted on lines 7 through 20, such as depreciation that belongs on line 14 rather than as a Section 179 item on Schedule K.

How to complete each Schedule K-1

Each shareholder receives a separate Schedule K-1 that shows their allocated share of every Schedule K line. Start by entering the corporation's name, EIN, and tax year at the top of each K-1, followed by the shareholder's personal information, including their name, address, and SSN or EIN. Then enter their ownership percentage and their share of each income and deduction category, calculated based on the percentage they held throughout the year.

Use this template structure as a checklist when completing each K-1:

- Box 1: Ordinary business income or loss (shareholder's percentage of line 21)

- Box 2 or 3: Net rental real estate income or other rental income

- Box 5: Interest income

- Box 8 or 9: Net short-term or long-term capital gain or loss

- Box 11: Section 179 deduction

- Box 12: Charitable contributions, broken out by rate category

- Box 16: Basis information required under current IRS rules

Send each shareholder their completed K-1 by the same date you file the return. Shareholders need the K-1 figures to complete their personal returns, so late delivery creates problems downstream for everyone with an ownership stake.

Step 6. Finish schedules L, M-1, and M-2

Schedules L, M-1, and M-2 sit at the back of Form 1120-S, and many filers treat them as an afterthought. That's a mistake. These three schedules verify that your books and your tax return agree, and they give the IRS a clear picture of your corporation's financial position. Completing them accurately also protects you if the IRS ever questions how you calculated shareholder distributions or deferred expenses.

Schedule L: Balance Sheet Per Books

Schedule L is a standard balance sheet pulled directly from your accounting records, reported as of the first and last day of your tax year. You enter your assets on the top half and your liabilities and equity on the bottom half. The total assets figure from line 15, column d is the same number you entered on page one of the return, so if those two figures don't match, you have a discrepancy to resolve before you file.

Use your year-end balance sheet from your bookkeeping software as the source for every line. Enter beginning-of-year balances in column b and end-of-year balances in column d. Do not adjust the figures for tax purposes here. Schedule L reflects your books as maintained, not your tax-adjusted numbers.

You only need to complete Schedule L if your S corporation had total receipts of $250,000 or more, or total assets of $250,000 or more at year-end. Smaller filers can skip it, but completing it anyway strengthens your records.

Schedule M-1: Reconciling Book Income to Tax Income

Schedule M-1 explains the difference between your net income per books and your ordinary income per the tax return. These two numbers rarely match, and that's expected. Common adjustments include meals and entertainment disallowed for tax purposes, depreciation differences, and tax-exempt income recorded in your books.

Work through lines 1 through 8 in order. Start with your net income per books on line 1, add back non-deductible expenses, subtract income not recorded on the books for tax purposes, and arrive at the income reported on line 21 of the return on line 8. If those figures reconcile, you're done with M-1.

Schedule M-2: Accumulated Adjustments Account

Schedule M-2 tracks your corporation's Accumulated Adjustments Account, commonly called the AAA. The AAA starts with your beginning balance, adds ordinary income from the current year, subtracts distributions made to shareholders, and accounts for any losses or non-deductible expenses. Following the irs form 1120-s instructions for M-2 keeps your AAA balance current, which matters when shareholders receive distributions, because distributions paid from the AAA are generally tax-free up to the shareholder's basis.

Wrap up and next steps

Filing Form 1120-S correctly means working through each section in order, from the identification fields at the top to the reconciliation schedules at the back. Every number you enter on the corporate return flows directly into your shareholders' personal returns through the K-1, so accuracy at every step is not optional. Following the irs form 1120-s instructions line by line, with clean books and complete shareholder records in hand, gives you the best shot at a complete and penalty-free filing.

S corp returns have more moving parts than most business owners expect the first time through. If your situation includes shareholder loans, built-in gains, passive income, or mid-year ownership changes, the complexity increases quickly. That's where professional help pays for itself. The CPAs and Enrolled Agents at Tax Experts of OC prepare S corp returns for businesses across all 50 states and can handle your filing from start to finish.