Most startups don't fail because of a bad product. They fail because they run out of money, and a surprising number run out of money because they never had a clear picture of where it was going in the first place. That's where bookkeeping for startups comes in. Getting your financial records right from day one isn't just good hygiene, it's the difference between making decisions based on data and making them based on gut feelings and bank account balances.

But here's the problem: you're building a company, not studying accounting. You need a system that works now, when you have five transactions a week, and still holds up later when you're processing hundreds. You need to know whether to hire a bookkeeper, use software, or both, and you need honest answers about what each option actually costs. That's exactly what this guide covers, with practical steps you can act on whether you launched yesterday or a year ago.

At Tax Experts of OC, we work with startup founders across all 50 states on everything from entity formation and tax structuring to ongoing bookkeeping and accounting. We've seen firsthand what happens when businesses skip the financial foundation, and what becomes possible when they build it right. This article pulls from that experience to give you a clear, complete roadmap for setting up and scaling your bookkeeping as your startup grows.

Why clean books matter for startups

Running a startup means making dozens of decisions every week, and most of them carry financial consequences you can't fully see unless your books are accurate. Sloppy records don't just create headaches at tax time. They actively undermine your ability to manage cash flow, control expenses, and plan for growth. Getting your bookkeeping right early costs far less than reconstructing a year's worth of transactions from bank statements or fixing errors that have already triggered an IRS notice.

Your decisions depend on accurate data

When you're spending money on marketing, hiring, or software, you need to know whether those investments are working. Clean financial records give you a real-time view of your profit margins, your burn rate, and which parts of your business are actually generating a return. Without that data, you're making calls based on incomplete information, and that pattern catches up with you fast.

Consider a concrete example. Imagine you're a SaaS startup spending $3,000 per month on paid ads. Without accurate bookkeeping, you may not realize that your cost to acquire a customer has tripled over three months while your average contract value has stayed flat. That's the kind of signal that should trigger an immediate strategic shift. With disorganized records, you might not catch it until the damage is significant and harder to reverse.

Clean books aren't a back-office task. They're the primary tool you use to understand whether your business model actually works.

Investors and lenders need accurate financials

If you plan to raise capital at any point, your financial records will face serious scrutiny. Investors conduct due diligence before writing a check, and the first thing they ask for is a complete set of organized financial statements. A startup that can immediately hand over a clean profit and loss statement, a balance sheet, and a cash flow report signals that the founders understand how to run an operation, not just how to build a product.

Banks and alternative lenders hold to the same standard. Whether you're applying for an SBA loan or a business line of credit, lenders need to verify your revenue history, expense patterns, and cash position. Gaps in your records, inconsistencies between accounts, or missing months of data can delay funding or kill an application entirely. Investors and lenders want to back founders who are in control of their numbers.

Tax compliance starts on day one

Bookkeeping for startups isn't just an internal planning tool. Every transaction you record feeds directly into your tax filings. If you're structured as a corporation, you have estimated tax payments due quarterly. If you hire employees or pay contractors, you have payroll tax obligations that carry strict deadlines. If you collect sales tax across multiple states, you need to track that separately by jurisdiction because each state has its own rules and filing requirements.

Your monthly records also determine how smoothly your annual tax filing goes. When your books are accurate and current, a CPA or tax professional can prepare your return efficiently because they're working from clean data. When records are missing or inconsistent, that professional has to spend billable hours reconstructing transactions, and even then the results may contain errors that attract IRS attention. Staying on top of your books every month is the most practical way to keep your tax obligations manageable and stay out of trouble.

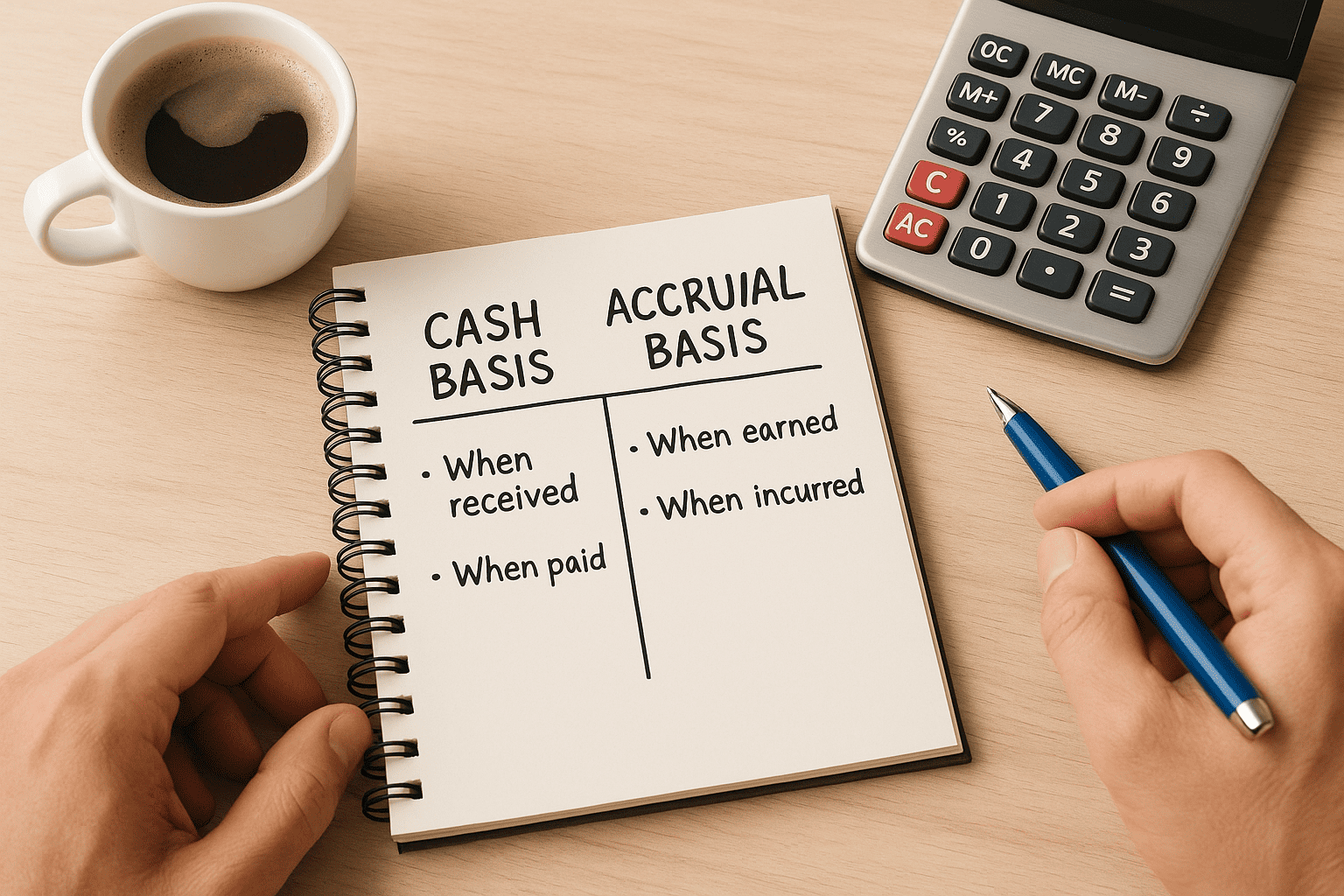

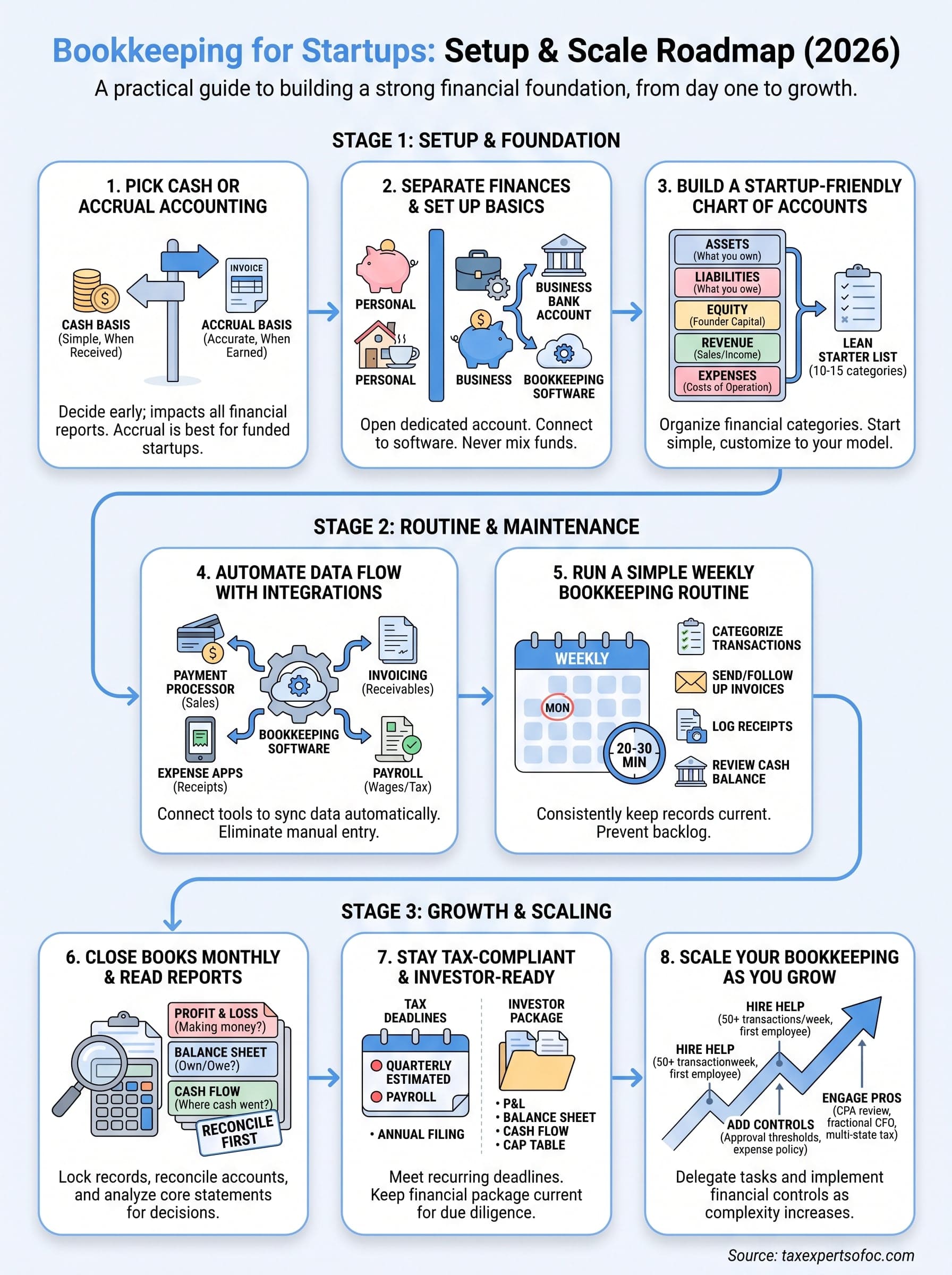

Step 1. Pick cash or accrual accounting

The first accounting decision you make affects every financial report you'll produce from this point forward. Cash or accrual accounting determines when you record income and expenses, and choosing the wrong method for your stage creates problems that compound over time. Most startups can make this decision in about five minutes once they understand what each method actually means in practice.

Cash basis accounting

Cash basis is straightforward: you record income when money arrives in your bank account and record expenses when you actually pay them. If a client pays you in January for work you completed in December, that revenue shows up in January's records. This method works well for early-stage startups with simple, consistent transactions, sole proprietors, and service businesses that don't carry inventory. The IRS generally allows businesses with average annual gross receipts under $30 million to use cash basis, which covers the vast majority of startups.

Accrual basis accounting

Accrual accounting records income when you earn it and expenses when you incur them, regardless of when cash actually moves. If you send an invoice in March and collect payment in May, the revenue posts in March. This method gives you a more accurate picture of your financial performance over any given period, which matters more as your operation grows in complexity. Investors and lenders typically expect accrual-based financial statements, and if you plan to raise a Series A or apply for a substantial credit line, you'll need this method in place before those conversations start.

If you expect to raise venture capital or carry significant accounts receivable within the next 12 months, start with accrual accounting from day one. Switching mid-stream is tedious and creates inconsistencies across your historical records.

Use this comparison to make the call:

| Factor | Cash Basis | Accrual Basis |

|---|---|---|

| Revenue recorded | When received | When earned |

| Expenses recorded | When paid | When incurred |

| Best for | Early-stage, service businesses | Funded startups, product companies |

| Investor ready | Rarely | Yes |

| Complexity | Low | Moderate |

Strong bookkeeping for startups begins with locking in this choice before you record your first transaction. If you're genuinely unsure which method fits your specific model, a CPA can review your projected revenue and business structure and give you a direct answer in a single short consultation rather than leaving you guessing.

Step 2. Separate finances and set up the basics

The single fastest way to make bookkeeping for startups harder than it needs to be is mixing personal and business money in one account. When you pay a vendor from your personal card and reimburse yourself weeks later, you create a paper trail that requires twice the work to untangle. Separating your finances from the moment you start spending on your business saves hours every month and keeps your records defensible if you're ever audited.

Open a dedicated business bank account

Your first move is opening a business checking account in your company's legal name. Most major banks offer business checking with low or no monthly fees for accounts that maintain a minimum balance. Bring the following when you apply:

- Your EIN (Employer Identification Number) from the IRS

- Your formation documents (Articles of Incorporation or LLC Operating Agreement)

- A government-issued photo ID

- An initial deposit (requirements vary by bank, but $100 is typical)

Once the account is open, route all business revenue into it and pay all business expenses from it. Never use this account for personal purchases. That single rule eliminates the most common source of bookkeeping errors in early-stage companies.

Your business bank account is the foundation every other financial record builds on. Get this right before you touch anything else.

Connect your account to bookkeeping software

After you open the account, link it directly to your bookkeeping software through a bank feed integration. QuickBooks Online, Xero, and Wave all support direct bank connections that pull transactions automatically each day. This means you're not manually entering data, you're categorizing transactions that already appear in your system.

Apply the same approach to any business credit card you open. A dedicated card lets you track spending by expense category, build business credit history, and separate operating costs from capital purchases without any extra reconciliation effort. Set the card to autopay from your business checking account each month to avoid interest charges that complicate your expense records.

Together, a dedicated bank account, a business credit card, and connected software form the operational core of your financial system. Every subsequent step in this guide builds directly on this foundation, so taking 30 minutes now to get these pieces in place pays dividends every month going forward.

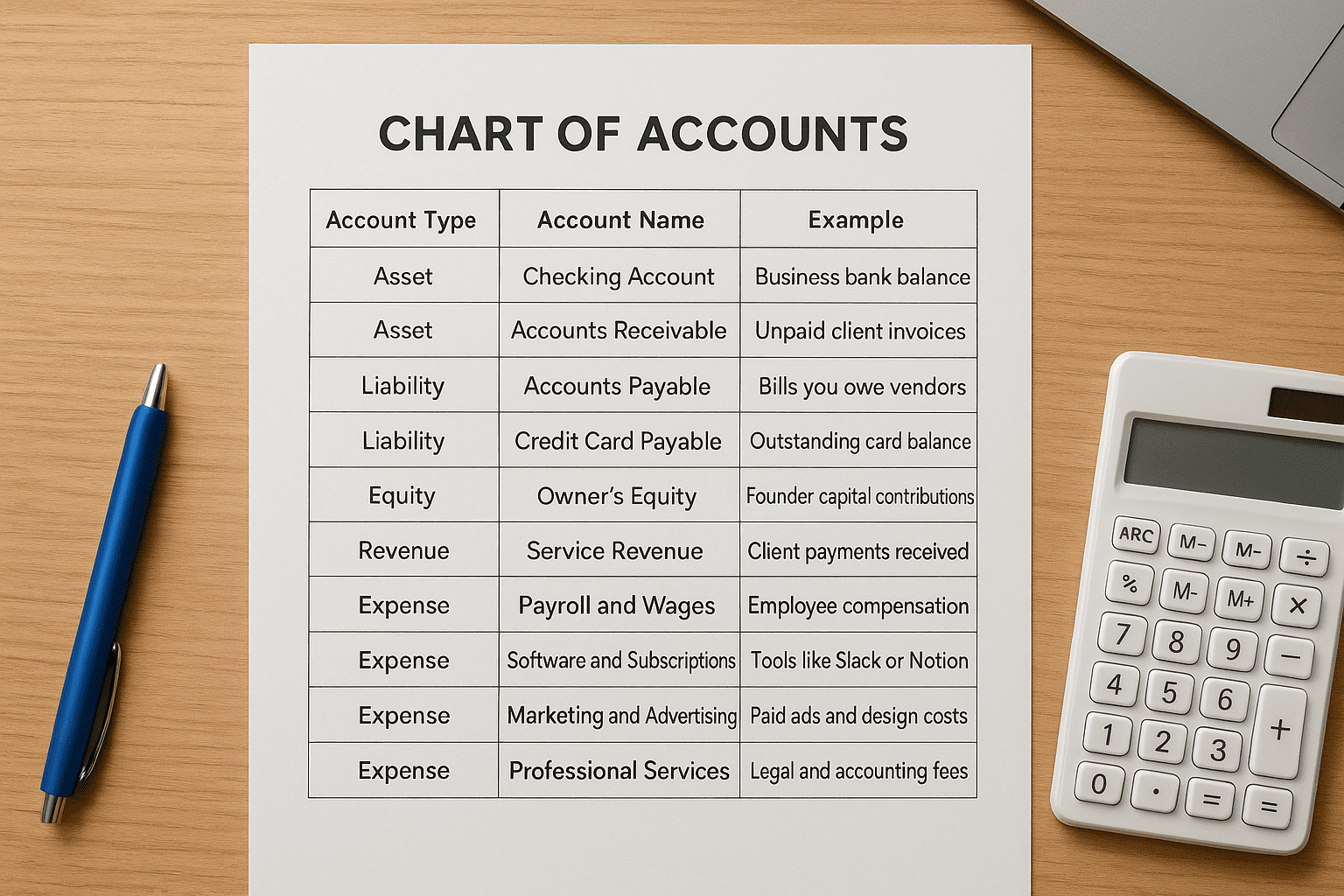

Step 3. Build a startup-friendly chart of accounts

A chart of accounts is the master list of every financial category your business uses to record transactions. Think of it as the filing system behind your bookkeeping software. Every time you categorize a bank transaction or create an invoice, you assign it to a specific line in this list. Getting the structure right early means your financial reports actually reflect how your business operates, rather than dumping everything into vague buckets like "miscellaneous expense" that tell you nothing useful when you're trying to manage spending.

What a chart of accounts includes

Your chart of accounts organizes into five core groups: assets, liabilities, equity, revenue, and expenses. Each group contains specific sub-accounts that you customize to match your business model. A SaaS startup needs different expense categories than a product company carrying physical inventory, so the starting point is understanding your own transaction patterns. Below is a clean starter chart of accounts built for an early-stage startup:

| Account Type | Account Name | Example |

|---|---|---|

| Asset | Checking Account | Business bank balance |

| Asset | Accounts Receivable | Unpaid client invoices |

| Liability | Accounts Payable | Bills you owe vendors |

| Liability | Credit Card Payable | Outstanding card balance |

| Equity | Owner's Equity | Founder capital contributions |

| Revenue | Service Revenue | Client payments received |

| Expense | Payroll and Wages | Employee compensation |

| Expense | Software and Subscriptions | Tools like Slack or Notion |

| Expense | Marketing and Advertising | Paid ads and design costs |

| Expense | Professional Services | Legal and accounting fees |

| Expense | Rent and Utilities | Office or coworking costs |

Your chart of accounts shapes every financial report you'll ever pull. Build it to reflect your actual business, not a generic template someone else created for a completely different industry.

Keep it lean at the start

The most common mistake in bookkeeping for startups is creating too many sub-accounts from the beginning. When you split expenses into 40 narrow categories, you spend more time deciding where to put each transaction than actually reviewing the data those categories produce. Start with 10 to 15 expense accounts that map directly to your real spending patterns and resist the urge to over-engineer it upfront.

You can always add new accounts later when a spending category grows large enough to justify tracking separately. Most bookkeeping software handles this in under two minutes. The goal at this stage is consistency, because a chart of accounts you use correctly every week outperforms an elaborate structure you abandon after the first month.

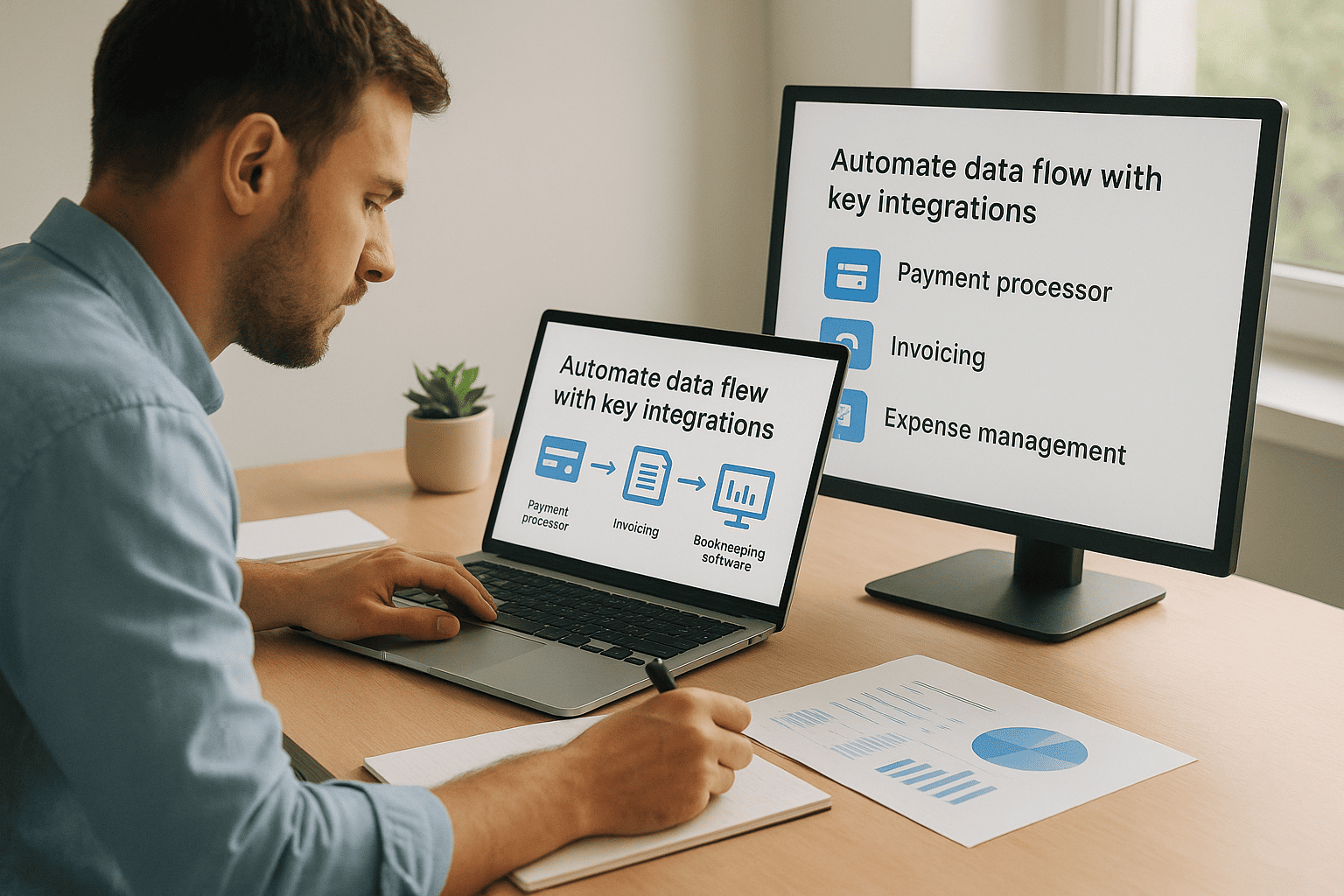

Step 4. Automate data flow with key integrations

Manual data entry is the fastest way to introduce errors into your books. Every time you type a number by hand, you create an opportunity for a typo, a duplicate, or a missed transaction. Bookkeeping for startups works best when your financial tools talk to each other automatically, pulling data between systems without requiring you to touch it. Setting up these integrations early takes a few hours and then runs quietly in the background while you focus on building the business.

Connect your payment and invoicing tools

Your payment processor is where real money moves, so it should connect directly to your bookkeeping software. Most major platforms offer native integrations that push transaction data automatically as sales occur. When a payment clears, it appears in your books, categorized and ready to review, with no manual entry required.

Automating your payment-to-books connection eliminates the most common source of revenue recording errors in early-stage startups.

The same logic applies to your invoicing workflow. When you send an invoice through your bookkeeping platform and a client pays it, the software automatically marks it as paid and updates your accounts receivable balance. Below are the core integrations worth setting up in your first 30 days:

| Tool Category | What It Automates | Where It Posts |

|---|---|---|

| Payment processor | Sales and refunds | Revenue accounts |

| Invoicing | Invoice status updates | Accounts receivable |

| Expense management | Receipt capture and coding | Expense accounts |

| Payroll | Wage and tax entries | Payroll expense accounts |

| E-commerce platform | Order revenue and fees | Revenue and cost accounts |

Set up expense tracking for receipts and cards

Receipts are the piece of bookkeeping documentation most founders handle poorly. Paper receipts get lost, digital ones pile up in email, and by month-end you're guessing what a charge was for. The fix is connecting a receipt-capture tool to your bookkeeping software so that every purchase feeds into your records immediately.

Most expense management apps let you photograph a receipt the moment you make a purchase. The app reads the amount and merchant, suggests a category, and syncs the transaction to your books automatically. Your business credit card transactions flow in alongside those receipts, so reconciling the two takes minutes rather than hours. Set this up before you accumulate a backlog because going back to match old receipts against card statements is time-consuming and error-prone.

Step 5. Run a simple weekly bookkeeping routine

Most bookkeeping problems don't come from complicated accounting decisions. They come from letting small tasks pile up until the backlog feels impossible to tackle. A weekly routine fixes that by keeping your records current at all times. When you spend 20 to 30 minutes every week on a consistent set of tasks, your books stay accurate without requiring large blocks of time you don't have.

What to do in your weekly session

Your weekly session follows the same checklist every time. Consistency in the sequence matters because skipping steps in one session means you carry the work forward and double the effort next week. Use this template as your standard weekly routine:

- Categorize new transactions: Review any bank or card transactions your software pulled in since your last session and assign each one to the correct account in your chart of accounts.

- Send or follow up on invoices: Create new invoices for work completed during the week and send a payment reminder on any invoice that is 7 or more days past its due date.

- Log receipts: Match any physical or digital receipts to their corresponding card transactions and confirm the category is correct before moving on.

- Review your cash balance: Check your actual bank balance against what your software shows and flag any discrepancy immediately rather than letting it sit.

- Note anything unusual: If you see a charge you don't recognize or a payment that came in without a matching invoice, write it down and resolve it before your next session.

Letting a single unresolved transaction sit for a month is how one small question turns into a full audit of your own records.

Keep sessions short and consistent

Pick one specific day and time each week for your bookkeeping session and treat it as a fixed appointment. Most founders find that Monday morning or Friday afternoon works well because it either sets the financial tone for the week or closes it out cleanly. The actual day matters less than the habit. Skipping sessions is the primary reason bookkeeping for startups fails early, so protect this time the same way you'd protect a meeting with an investor or a key client.

When your session runs longer than 30 minutes, that's a signal that your integrations or categorization rules need adjustment. Well-configured software handles the data entry automatically, leaving you to review and confirm rather than type.

Step 6. Close your books monthly and read the reports

A monthly close is the process of locking your records for the previous period so you have a verified, accurate snapshot of your financial position. This isn't optional busywork. It's the step that transforms raw transaction data into reliable financial statements you can actually use to make decisions, file taxes, and show investors. Most founders skip it and rely on running totals, which means they're always looking at a moving target rather than a confirmed number.

Reconcile every account before you close

Reconciliation means comparing your bookkeeping records against your actual bank and credit card statements to confirm they match exactly. Every transaction in your software should appear on your bank statement, and nothing should be missing or duplicated. When you find a discrepancy, you resolve it before moving on. This step catches errors, duplicate entries, and fraudulent charges before they compound into larger problems.

Work through this checklist at the end of every month:

- Checking account: Match every transaction in your software against your bank statement line by line.

- Credit card accounts: Confirm all charges in your software match your statement and that the closing balance is identical.

- Accounts receivable: Review all open invoices and confirm that paid ones are marked correctly in your system.

- Accounts payable: Verify that all vendor bills are recorded and that payments are applied to the correct bill.

A reconciliation that takes more than an hour usually means your weekly routine slipped. Keep weekly sessions current and the monthly close stays fast.

Read the three core financial statements

Once your accounts reconcile cleanly, pull your three core reports and read them actively rather than filing them away. Each statement answers a specific question about your business, and together they give you a complete financial picture for the period.

Bookkeeping for startups only pays off when you actually study the output. Here's what each report tells you and where to focus your attention:

| Report | What It Answers | Key Line to Watch |

|---|---|---|

| Profit and Loss | Are you making money this month? | Net income |

| Balance Sheet | What do you own and owe? | Total equity |

| Cash Flow Statement | Where did cash actually go? | Net cash from operations |

Spend 10 minutes reviewing each report for trends, anomalies, or categories that moved unexpectedly. If your marketing spend doubled without a matching revenue increase, that signal shows up here first, before it becomes a cash problem you're scrambling to solve.

Step 7. Stay tax-compliant and investor-ready

Clean books only protect you if you actually use them to stay current on your tax obligations and reporting requirements. Most startup founders understand they need to file an annual return, but compliance runs on a much tighter schedule than that. Missing a quarterly payment or failing to file a required form doesn't just generate a penalty: it creates a compliance record that can complicate funding conversations and IRS interactions for years.

Meet your recurring tax deadlines

Your federal and state tax obligations repeat on a fixed calendar, which means you can plan for them in advance rather than scrambling when they arrive. Build these dates into your scheduling system at the start of each year so nothing catches you off guard.

Here are the core recurring deadlines most startups need to track:

| Obligation | Frequency | Who It Applies To |

|---|---|---|

| Federal estimated taxes | Quarterly | LLCs, S-corps, sole proprietors |

| Payroll tax deposits | Monthly or semi-weekly | Any business with employees |

| Sales tax filings | Monthly, quarterly, or annually | Businesses with nexus in applicable states |

| Annual federal return | Once per year | All business entities |

| 1099 forms | Annually (January 31) | Businesses paying contractors $600+ |

Missing an estimated tax payment doesn't just cost you a penalty: it signals to the IRS that your financial management needs attention, which increases your audit risk.

Keep your records investor-ready at all times

Bookkeeping for startups pays off most visibly when you can hand a complete financial package to an investor or lender within 24 hours of being asked. That requires keeping three specific documents current every single month, not just at year-end.

Your investor-ready financial package should include:

- Profit and Loss statement: Covering at least the last 12 months with clear revenue and expense breakdowns by category.

- Balance sheet: Dated to the most recent month-end close with all accounts reconciled before sharing.

- Cash flow statement: Showing operating, investing, and financing activity separately so investors can see exactly how you're managing liquidity.

- Cap table: A current record of equity ownership, including all founder shares, option pools, and any convertible instruments outstanding.

Maintain these documents inside a secure, organized folder that you update at the end of every monthly close. When a due diligence request arrives, you respond immediately instead of spending two weeks reconstructing data under pressure.

Step 8. Scale your bookkeeping as you grow

The system you built in steps one through seven works well at low transaction volume, but it needs deliberate upgrades as your startup adds revenue, headcount, and complexity. Bookkeeping for startups at the early stage is mostly about consistency and discipline. At the growth stage, it becomes about adding the right people, processes, and controls before the gaps become expensive. Waiting until your books are already behind to make these changes costs significantly more than addressing them proactively.

Know when to hire a bookkeeper or accountant

Your current workload is the clearest signal that it's time to bring in outside help. If your weekly bookkeeping session regularly runs longer than an hour, or if you're closing the month late more often than on time, you've passed the point where a solo founder can manage the function efficiently. Hiring a dedicated bookkeeper frees you from transaction-level work so you can focus on the decisions those records support.

Use these benchmarks to decide when to escalate your support:

| Trigger | Recommended Action |

|---|---|

| 50+ transactions per week | Hire a part-time bookkeeper |

| First W-2 employee | Add dedicated payroll management |

| Revenue exceeds $500K annually | Engage a CPA for monthly review |

| Preparing for a funding round | Bring in a fractional CFO |

| Multi-state sales tax obligations | Work with a state and local tax specialist |

Bringing in a professional before you hit capacity means they learn your business when the records are clean, not when they're behind and under pressure.

Add financial controls as your team grows

More team members means more people touching your finances, which increases the risk of errors and unauthorized spending. The fix is adding basic internal controls that separate duties and create a clear approval chain. When one person requests a purchase, a different person approves it, and a third person records it, mistakes surface quickly because no single error passes unreviewed.

Build these controls into your process as your team expands:

- Spending approval thresholds: Require manager sign-off on any purchase above a set dollar amount, such as $500, before payment is made.

- Expense policy documentation: Write down which categories are reimbursable, what documentation is required, and the deadline for submitting receipts.

- Monthly financial review meeting: Schedule a standing 30-minute meeting with your leadership team to walk through the three core financial statements and flag anything that needs action before the next period closes.

What to do next

You now have a complete system for bookkeeping for startups, from picking your accounting method on day one to adding financial controls as your team grows. Each step in this guide builds on the one before it, so the fastest path forward is starting at step one and working through the checklist in order, even if your startup is already past the early stage. Consistency over the next 90 days matters more than perfection in any single week.

Most founders find they can handle the routine work themselves in the early months, but eventually hit a point where the complexity outgrows a solo effort. When that moment arrives, working with a qualified professional makes a measurable difference. At Tax Experts of OC, our CPAs and Enrolled Agents help startups across all 50 states get their books right and stay compliant year-round. Schedule a free 30-minute consultation with our team at Tax Experts of OC to talk through your specific situation.