When you work for yourself, nobody withholds taxes from your income. That means the IRS expects you to handle it on your own through quarterly tax payments self-employed individuals are required to make throughout the year. Miss a deadline or underpay, and you'll face penalties that add up faster than most people realize.

The system itself isn't complicated once you understand it. You estimate what you owe, divide it across four deadlines, and submit payments using IRS Form 1040-ES. But getting the numbers right, especially when your income fluctuates month to month, is where most self-employed taxpayers run into trouble.

This guide walks you through the full process: who needs to pay estimated taxes, how to calculate the correct amount, when each payment is due, and exactly how to submit them. At Tax Experts of OC, our CPAs and Enrolled Agents help self-employed clients across all 50 states stay ahead of their tax obligations instead of scrambling to catch up. Whether you're a freelancer, independent contractor, or small business owner, this is the straightforward breakdown you need to handle quarterly payments with confidence.

What quarterly estimated taxes cover

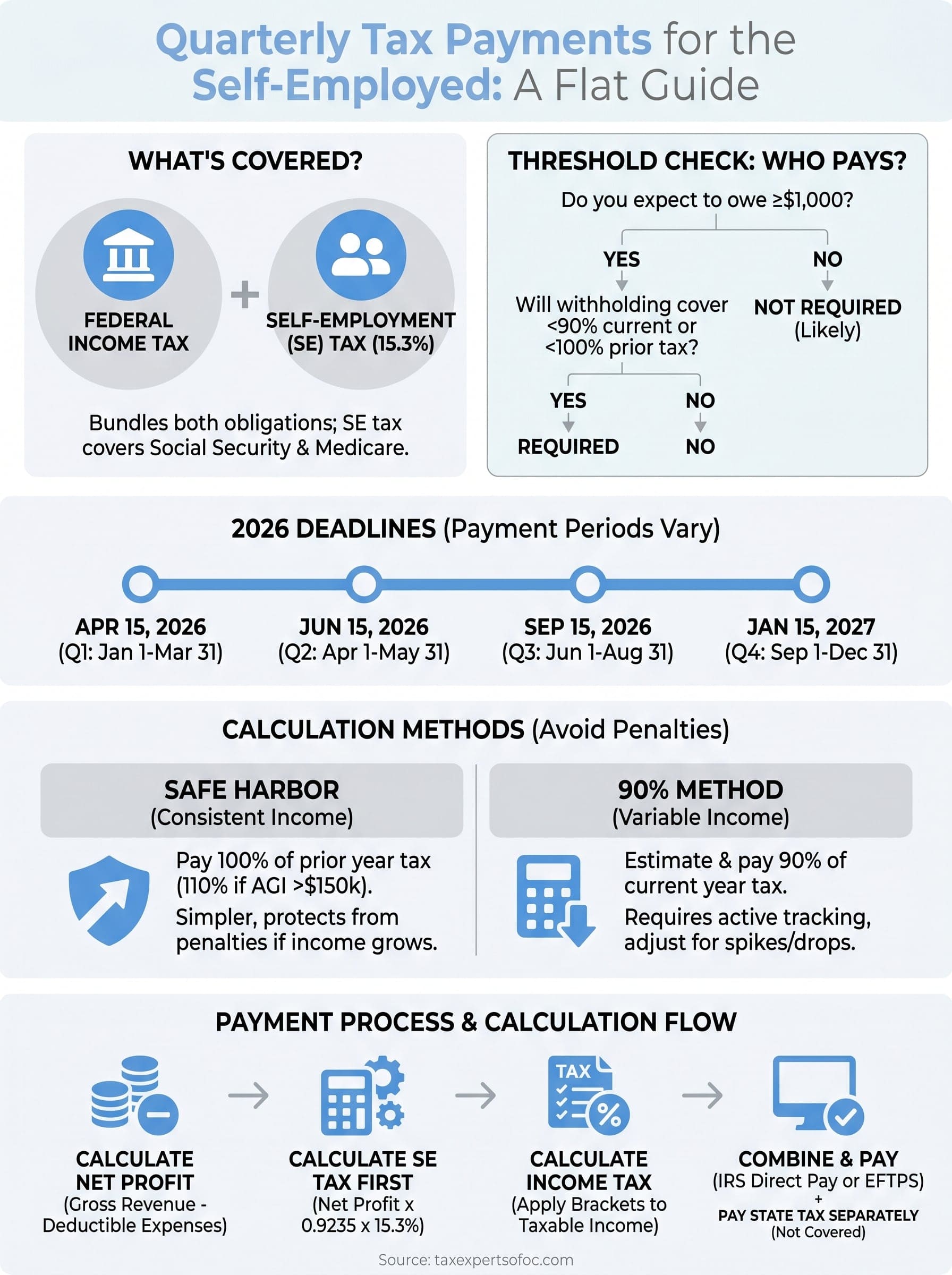

When you make quarterly tax payments self-employed filers are required to submit, you are not just paying federal income tax. Each payment you send to the IRS bundles together two separate obligations that most W-2 employees never think about because their employer handles both automatically. Understanding what goes into each payment is the foundation for calculating the correct amount, and skipping this step is how most self-employed people end up underpaying.

The two taxes bundled into one payment

Your estimated quarterly payment covers federal income tax and self-employment (SE) tax in a single submission. Federal income tax works the same way it does for any taxpayer: you owe a percentage of your taxable income based on the IRS tax brackets for your filing status. Self-employment tax is different. It exists because, as a self-employed person, you act as both the employer and the employee at the same time.

When someone works a traditional job, their employer pays 6.2% for Social Security and 1.45% for Medicare, and the employee pays the same rates through payroll withholding. That adds up to 15.3% total. Because you are your own employer, you owe the full 15.3% yourself on your net self-employment income. The IRS does allow you to deduct half of that SE tax when calculating your adjusted gross income, which softens the impact, but the base obligation is still significant.

If you only budget for income tax and forget SE tax, you will consistently underpay and face penalties at the end of the year.

How the SE tax rate applies to your income

The 15.3% SE rate does not apply to every dollar you earn without a ceiling. For 2026, Social Security tax (12.4%) applies only to the first $176,100 of net self-employment income. Once your earnings exceed that threshold, you stop paying the Social Security portion on amounts above it. The Medicare portion (2.9%) has no cap and applies to all net self-employment income.

There is also an Additional Medicare Tax of 0.9% that applies if your total income exceeds $200,000 for single filers or $250,000 for married filing jointly. You do not pay this through your quarterly estimates automatically. The IRS reconciles it when you file your annual return, but you can add it to your quarterly payments voluntarily if you expect to cross that threshold.

Here is how the SE tax breaks down for a self-employed person with $80,000 in net profit for the year:

| Component | Rate | Amount |

|---|---|---|

| Social Security (12.4%) | 12.4% on $80,000 | $9,920 |

| Medicare (2.9%) | 2.9% on $80,000 | $2,320 |

| Total SE Tax | 15.3% | $12,240 |

| SE Tax Deduction (50%) | Reduces taxable income | -$6,120 |

After applying the deduction, you would calculate your income tax on approximately $73,880 rather than the full $80,000.

What your payments do not cover automatically

Your federal estimated payments go to the IRS, but they do not cover state income tax for the roughly 41 states that collect it. Most states require their own quarterly estimated payments on a separate schedule and through their own payment portals. California, for example, uses the Franchise Tax Board (FTB) and has different due dates than the federal system.

Your quarterly payments also do not automatically cover self-employed health insurance premiums or contributions to retirement accounts like a SEP-IRA or Solo 401(k), though both of those reduce the income you will eventually owe taxes on. These deductions affect your annual return, not the payment itself. Keeping clean, organized records of these expenses throughout the year makes it much easier to calculate accurate estimates each quarter and avoid overpaying.

Finally, your payments do not cover state-level self-employment taxes where they apply, franchise taxes, or any sales tax obligations your business might carry. Estimated quarterly payments are strictly about your personal income tax and SE tax liability. Separating these categories clearly from the start will save you from a chaotic scramble when you sit down to prepare each payment.

Check if you must pay quarterly taxes

Not every self-employed person is required to make quarterly payments, but most are. The IRS applies a straightforward threshold test to determine your obligation, and failing to check before the first deadline costs you money in penalties even if you pay everything in full at tax time. Run through this check at the start of each year, especially if your income or filing situation changed.

The IRS two-part threshold test

The IRS requires you to make quarterly tax payments self employed individuals owe when two conditions are both true. First, you expect to owe at least $1,000 in federal taxes after subtracting any withholding and credits from your total tax bill. Second, your withholding and refundable credits will cover less than the smaller of these two amounts: 90% of the tax you owe for the current year, or 100% of the tax shown on your prior year's return (110% if your prior year adjusted gross income exceeded $150,000).

If both conditions apply to you, you must make quarterly payments or face an underpayment penalty when you file your return.

Most self-employed people clear both thresholds easily because they have no employer withholding at all. Even modest freelance income of $5,000 to $10,000 net can generate a tax bill above $1,000 once you factor in SE tax. Here is a quick reference to see where you stand:

| Situation | Likely required to pay quarterly? |

|---|---|

| Sole proprietor, no other income | Yes |

| Freelancer with a W-2 job | Depends on withholding amount |

| Self-employed with under $400 net income | No |

| Partner in a partnership | Usually yes |

| S-Corp shareholder taking distributions | Often yes |

Exceptions that let you skip quarterly payments

A few situations allow you to avoid quarterly payments without penalty. If you owed no federal tax in the prior year and that year covered a full 12-month period, you are not required to pay estimates for the current year. This exception applies regardless of how much you earn in the current year, but it only protects you from the underpayment penalty, not from the tax itself.

You also avoid the requirement if your total tax liability for the year will be below $1,000 after withholding. If you have a W-2 job alongside your self-employment work, increasing your withholding on that W-2 through a new Form W-4 can sometimes cover enough of your combined tax bill to eliminate the need for separate quarterly payments entirely. Run the numbers before assuming that strategy will work for your income level.

Mark the 2026 federal due dates

The IRS does not send reminders when a quarterly tax payment deadline approaches. You are responsible for tracking these dates yourself, and the calendar does not follow the actual quarter boundaries you might expect. Knowing each deadline in advance lets you budget, gather records, and submit on time without any last-minute pressure.

The four 2026 deadlines

The federal estimated tax schedule covers four payment periods, but the due dates do not land at the end of each calendar quarter. The IRS staggers them in a way that trips up many first-time quarterly tax payments self employed filers who assume they follow a strict January, April, July, October pattern.

Missing even one deadline triggers a penalty calculated on that specific underpayment, so you owe the penalty for that period even if you catch up with the next payment.

Here are all four 2026 federal deadlines in one place:

| Payment Period | Income Earned | Due Date |

|---|---|---|

| Q1 | January 1 to March 31, 2026 | April 15, 2026 |

| Q2 | April 1 to May 31, 2026 | June 15, 2026 |

| Q3 | June 1 to August 31, 2026 | September 15, 2026 |

| Q4 | September 1 to December 31, 2026 | January 15, 2027 |

Notice that Q2 only covers two months, not three, and Q4 runs for four months. This is the IRS's standard structure, not a variation for 2026.

What happens when a deadline falls on a weekend or holiday

The IRS automatically shifts any deadline that falls on a Saturday, Sunday, or federal holiday to the next business day. For 2026, all four dates land on weekdays, so there are no automatic extensions this cycle. Do not count on a shift buying you extra time.

Submitting your payment on the deadline date itself is acceptable, but processing times vary depending on your payment method. If you mail a check, the IRS uses the postmark date to determine timeliness, so you need to mail it by the deadline, not just have it arrive by then.

Linking due dates to your recordkeeping

Each deadline gives you a natural checkpoint to review your income and expenses for the period. Treat the two weeks before each due date as your preparation window. Pull your invoices, total your net profit, run your SE tax calculation, and submit the payment before the deadline rather than on it. This approach catches any errors in your records before they become an underpayment problem.

Pick a calculation method that avoids penalties

The IRS does not penalize you for guessing wrong on your income, but it does penalize you for paying too little. Two approved calculation methods let you make quarterly tax payments self employed filers can rely on without triggering an underpayment penalty. Choosing the right one for your situation depends on whether your income is stable or unpredictable from year to year.

Use the safe harbor method when income is consistent

The safe harbor method is the simpler option. You base your payments on what you owed last year instead of trying to project the current year. If your prior year adjusted gross income (AGI) was $150,000 or less, you pay 100% of last year's total tax liability spread evenly across four payments. If your prior year AGI exceeded $150,000, you pay 110% of last year's total tax liability instead.

Using safe harbor protects you from underpayment penalties no matter how much your income grows in the current year.

To apply this method, pull your prior year Form 1040 and find the "Total Tax" line. Divide that number by four. That is your payment for each quarter. Here is an example for a filer with a prior year total tax of $9,200 and AGI under $150,000:

| Quarter | Calculation | Payment Due |

|---|---|---|

| Q1 | $9,200 / 4 | $2,300 |

| Q2 | $9,200 / 4 | $2,300 |

| Q3 | $9,200 / 4 | $2,300 |

| Q4 | $9,200 / 4 | $2,300 |

This method works well when your income this year will be similar to or higher than the prior year. If your income drops significantly, you may overpay and simply receive a refund at filing.

Use the 90% method when income is lower or variable

If you expect to earn significantly less this year than last year, the safe harbor method will have you overpaying every quarter. In that case, use the 90% method instead. You estimate your actual current year net income, calculate your expected total tax, and make sure your payments cover at least 90% of that amount by the end of the year.

This method requires more active tracking. You recalculate your expected annual income each quarter using your actual results so far, then adjust your remaining payments to stay on track. If your revenue spikes in one quarter, increase your next payment to compensate. If a slow quarter reduces your projected annual income, you can lower the next payment without penalty as long as your cumulative payments still cover 90% of the final bill.

Combining both methods is also valid. Start with safe harbor amounts early in the year, then switch to the 90% method mid-year if your actual income turns out to be lower than expected.

Estimate your net income for the quarter

Every accurate quarterly tax payment self employed filers submit starts with one number: your net profit for the period. Net profit is not your total revenue. It is what remains after you subtract legitimate business expenses from your gross income. Getting this number right each quarter is the single most important step in avoiding both underpayment penalties and unnecessary overpayments.

Start with your gross revenue

Your gross revenue includes every dollar your business received during the payment period, regardless of whether a client has paid their invoice yet. If you use cash-basis accounting, which most freelancers and small businesses do, you count income only when payment actually hits your account, not when you issue the invoice. Pull your bank statements, payment processor reports, and any cash receipts to build a complete picture of deposits during the quarter.

This is also a good time to separate personal deposits from business income. Transferring money between your own accounts, receiving a tax refund, or repaying yourself for a business expense you covered out of pocket are not income. Only client payments and business revenue count toward your gross total.

Subtract your allowable business deductions

Once you have your gross revenue, subtract every ordinary and necessary business expense you paid during the quarter. The IRS allows deductions for costs that are directly related to running your business, and these can significantly reduce the net income you owe tax on.

Common deductible expenses include:

- Home office costs (if the space is used exclusively and regularly for business)

- Business-use portion of your phone and internet bill

- Software subscriptions and online tools you use for work

- Professional development, courses, and industry publications

- Vehicle mileage or actual vehicle expenses for business travel

- Business insurance premiums

- Contractor or subcontractor payments you made

Keeping a dedicated business checking account and tracking expenses in a simple spreadsheet each month makes this calculation take minutes instead of hours before each deadline.

Apply the result to your payment calculation

After subtracting deductions from gross revenue, you have your estimated net profit for the quarter. Use this number as the base for all your tax calculations in the next section. If you earn inconsistently, multiply your quarterly net profit by four to project an estimated annual net income, then compare that projection to your prior year income to decide which calculation method, safe harbor or 90%, produces the lower required payment.

Here is a simple template to capture your quarterly estimate:

| Line Item | Amount |

|---|---|

| Gross revenue received this quarter | $ |

| Total deductible business expenses | $ |

| Estimated net profit (gross minus expenses) | $ |

| Annualized estimate (net profit x 4) | $ |

Calculate self-employment tax and income tax

Once you have your estimated net profit, you run two separate calculations before you know what to pay. The order matters: you calculate self-employment (SE) tax first, then use the deduction it produces to reduce the income you run through the federal tax brackets. Skipping that sequence leads to overstating your income tax every single time.

Calculate your SE tax first

Your SE tax applies to 92.35% of your net profit, not the full amount. The IRS allows this adjustment because employees do not pay SE tax on their employer's matching share. Multiply your net profit by 0.9235 to get your net earnings from self-employment, then multiply that result by 15.3% to get your SE tax.

Here is a worked example using $50,000 in annual net profit:

| Step | Calculation | Result |

|---|---|---|

| Net profit | Starting figure | $50,000 |

| Net earnings (x 0.9235) | $50,000 x 0.9235 | $46,175 |

| SE tax (x 15.3%) | $46,175 x 0.153 | $7,065 |

| SE tax deduction (50%) | $7,065 / 2 | $3,533 |

Take the SE tax deduction seriously because it directly reduces the taxable income you feed into the bracket calculation in the next step.

Apply the income tax brackets

Subtract the SE tax deduction from your estimated annual net profit to get your adjusted income. Then subtract your standard deduction (or itemized deductions if they are higher). For 2026, the standard deduction is $15,000 for single filers and $30,000 for married filing jointly. The amount left after both deductions is your estimated taxable income, which you run through the IRS brackets.

Continuing the example above for a single filer using the standard deduction:

| Step | Calculation | Result |

|---|---|---|

| Net profit | $50,000 | |

| Less SE deduction | -$3,533 | $46,467 |

| Less standard deduction | -$15,000 | $31,467 |

| Taxable income | $31,467 | |

| Estimated income tax (12% bracket) | $31,467 x 12% | $3,776 |

Combine both taxes and divide by four

Add your SE tax and estimated income tax together to get your total annual estimated tax liability. For making quarterly tax payments self employed filers need to submit, divide that combined total by four to get each installment.

Using the same example:

| Component | Amount |

|---|---|

| SE tax | $7,065 |

| Estimated income tax | $3,776 |

| Total annual estimated tax | $10,841 |

| Quarterly payment (divide by 4) | $2,710 |

Run this calculation at the start of each year and revisit it any time your income changes significantly mid-year. Recalculating takes less than 15 minutes once you have your net profit figure ready.

Pay the IRS and your state

Once you have your quarterly payment amount, you need to submit it through the right channel before each deadline. The IRS gives you several payment options, and most self-employed filers will find the electronic methods faster and easier to track than mailing a check. Your state also requires its own separate payment, and those two submissions are completely independent of each other.

Submit federal payments through IRS Direct Pay

The IRS offers a free online tool called IRS Direct Pay that pulls funds directly from your checking or savings account with no fees attached. You do not need to create an account to use it. Select "Estimated Tax" as the reason for payment, choose Form 1040-ES, select the applicable tax year, and enter your bank details. The IRS confirms your payment immediately and sends a confirmation number you should save for your records.

Always save your Direct Pay confirmation number and match it against your bank statement to confirm the funds cleared before the deadline.

If you prefer to pay by card, the IRS works with third-party processors that charge a small convenience fee, typically around 1.85% for credit cards. The IRS Electronic Federal Tax Payment System (EFTPS) at eftps.gov is another option that requires upfront enrollment but lets you schedule payments in advance, which is useful if you want to automate your quarterly submissions. Mailing a check with a completed Form 1040-ES voucher is still accepted, but the postmark date must be on or before the deadline, and you carry the risk of delays.

Here is a quick comparison of your federal payment options:

| Method | Cost | Processing Time | Best For |

|---|---|---|---|

| IRS Direct Pay | Free | Same day | Most self-employed filers |

| EFTPS | Free | Requires enrollment | Those who want to schedule ahead |

| Credit/debit card | 1.85% to 2% fee | Same day | Filers short on cash flow |

| Check with 1040-ES | Free | Postmark dependent | Those without online access |

Pay your state estimated taxes separately

Your federal payment to the IRS does not cover state income tax, and most states collect estimated taxes on their own schedule using their own payment portal. California filers pay through the Franchise Tax Board website, while other states use their own department of revenue systems. Search your state's department of revenue website directly to find the correct portal and confirm your state's specific quarterly deadlines, since several states use different dates than the federal schedule.

Set up separate calendar reminders for your federal and state due dates so you treat them as two distinct obligations. Missing one because you assumed the other covered both is a common and avoidable mistake for new self-employed filers making their first round of quarterly tax payments self employed individuals owe each year.

Adjust, catch up, and handle missed payments

Your income as a self-employed person rarely follows a straight line, and the IRS built the estimated tax system to accommodate that reality. If your revenue spikes in one quarter or drops sharply because of a slow month, a lost client, or a large deductible expense, you can adjust your remaining payments without starting over. The key is catching the change early and recalculating before the next deadline rather than waiting until you file your annual return.

Recalculate when your income shifts significantly

When your actual net profit for the year looks meaningfully different from what you originally projected, run a fresh calculation using your real numbers to date. Total your actual net profit year-to-date, project the remaining quarters based on current trends, and compare that revised annual estimate to both your safe harbor amount and the 90% threshold. Use whichever method produces the lower required payment for the quarters you still have left.

Here is a quick mid-year adjustment template to work through:

| Line Item | Amount |

|---|---|

| Actual net profit (Q1 through current quarter) | $ |

| Projected net profit (remaining quarters) | $ |

| Revised estimated annual net profit | $ |

| Revised SE tax (net profit x 0.9235 x 0.153) | $ |

| Revised income tax (apply brackets after deductions) | $ |

| Revised total annual estimated tax | $ |

| Payments already submitted this year | $ |

| Remaining balance to cover across future quarters | $ |

Divide the remaining balance by the number of payment periods you have left to get your adjusted quarterly payment. This approach keeps you on track without overpaying during a slow stretch.

What happens when you miss a deadline

Missing a deadline for quarterly tax payments self employed individuals owe does not result in a criminal penalty, but it does trigger an underpayment penalty calculated on the amount you should have paid. The IRS charges interest on that shortfall from the due date until you actually pay it, and the rate adjusts quarterly based on federal interest rates. For most filers, the penalty is relatively small, but it compounds the longer you wait.

If you missed a payment, submit it as soon as possible rather than waiting for the next scheduled deadline, because the penalty clock keeps running on the unpaid amount.

You can use IRS Direct Pay to catch up on a late or missed payment at any time. When you file your annual return, Form 2210 is the document the IRS uses to calculate the exact underpayment penalty for the year. In some cases, you can request a penalty waiver if the underpayment resulted from a casualty, disaster, or circumstances beyond your control, but routine income fluctuations generally do not qualify.

Wrap it up and stay compliant

Making quarterly tax payments self employed individuals owe each year comes down to four repeatable steps: confirm your obligation, mark your deadlines, calculate your net profit and combined tax, and submit on time through IRS Direct Pay or EFTPS. Each deadline is a checkpoint to review your income, adjust your projections, and keep penalties off the table. Build a simple calendar reminder two weeks before each due date and treat that window as your preparation time, not your filing time.

Staying compliant gets easier once the process becomes routine, but the numbers get harder to manage when your income grows, your deductions become more complex, or the IRS sends a notice. At that point, working with a professional saves you more than it costs. If you want a CPA or Enrolled Agent to review your situation and help you build a payment plan that works, schedule a free consultation with Tax Experts of OC today.