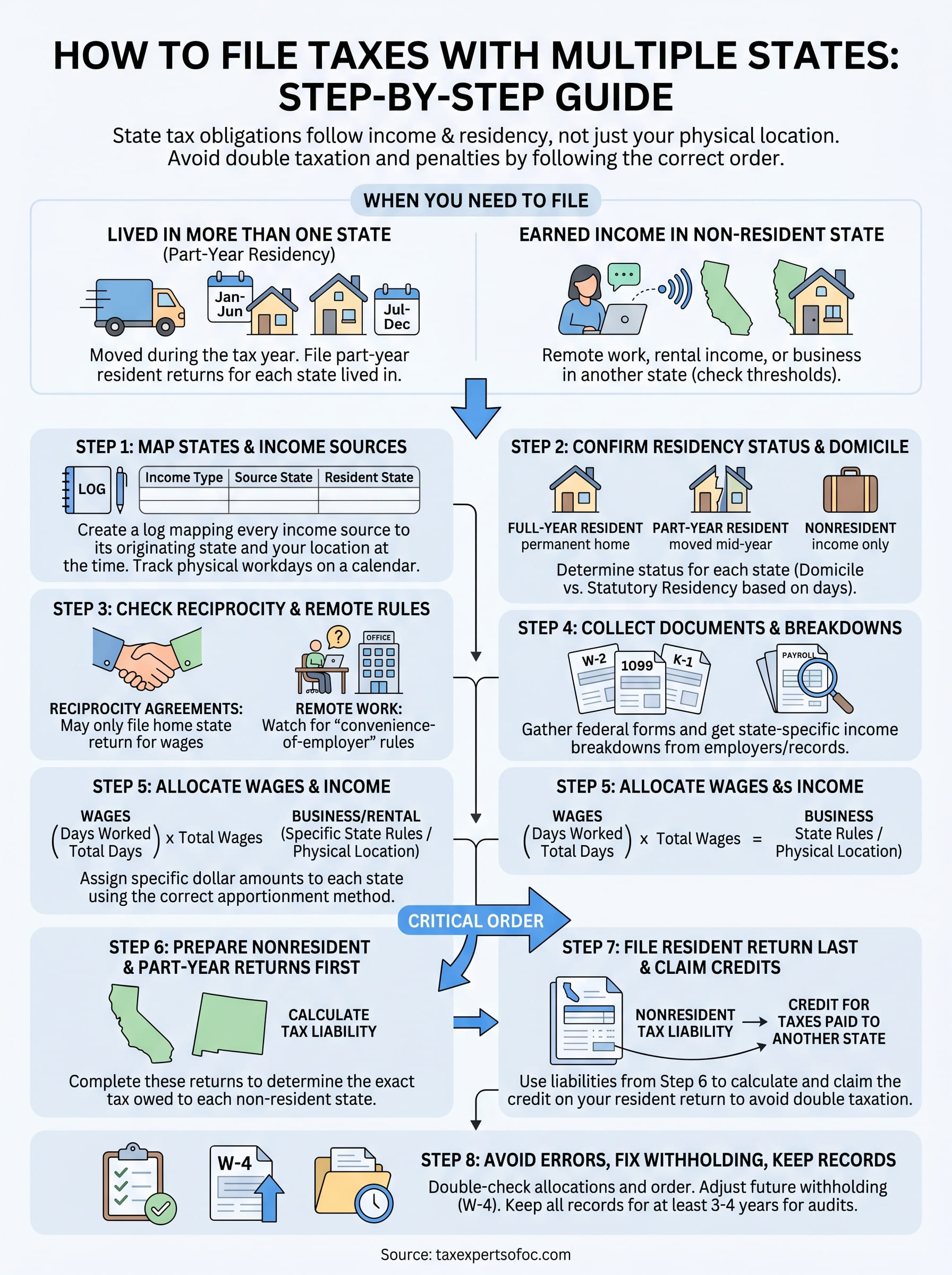

If you earned income in more than one state last year, you're not alone, and you're probably wondering how to file taxes with multiple states without overpaying or missing a deadline. Remote work, job relocations, freelance gigs across state lines, and investment properties in different states have all made multi-state filing increasingly common. The problem is that each state has its own rules about who owes taxes, how much, and when.

Getting it wrong can mean double taxation, unexpected penalties, or a notice from a state tax agency you didn't even know had a claim on your income. Getting it right requires understanding your residency status, knowing which states have reciprocity agreements, and filing your returns in the correct order.

This guide walks you through the entire process step by step. And if your situation is complex, multiple income sources, part-year residency, or overlapping state obligations, Tax Experts of OC can handle multi-state filings for clients in all 50 states, with direct access to a CPA and Enrolled Agent who deal with exactly these issues every day.

When you need to file in more than one state

Not everyone who crosses a state line owes taxes in multiple states, but the trigger happens more often than most people expect. State tax obligations follow your income and your residency, not just where you physically sit when you sign your return. Before you figure out how to file taxes with multiple states, you need to confirm whether you actually have a filing obligation in each state, because filing when you don't need to wastes time, and failing to file when you do can result in penalties, interest, and collection notices from agencies you weren't even thinking about.

You lived in more than one state during the year

Moving from one state to another during the tax year automatically creates a multi-state filing requirement in most cases. Each state where you held part-year resident status will want to tax the income you earned while you lived there. For example, if you moved from Ohio to Texas in June, Ohio will tax the income you earned from January through May. Texas has no state income tax, so you won't file there, but Ohio will still require a part-year resident return covering those first five months of the year.

Here are the most common life events that create part-year residency:

- Job relocation that required you to move to a new state

- Attending college in a different state and establishing residency there

- Military permanent change of station (PCS) orders

- Retirement move to a lower-tax or no-tax state mid-year

- Divorce or a family situation that caused a change in your primary residence

You earned income in a state where you don't live

You can trigger a nonresident filing obligation without ever changing your home address. States generally tax income that originates within their borders, which means the source of the money, not your home address, determines where you owe. If you performed consulting work for a client based in California while living in Nevada, California may expect a nonresident return from you, even if you never set foot in the state during the year.

Most states use a filing threshold, either a minimum dollar amount earned or a number of days physically worked there, below which they won't require a nonresident return, so always check the specific state's rules before assuming you need to file.

Other situations that require a multi-state return

Several less obvious scenarios also create filing requirements across state lines. Remote workers whose employers are based in a different state often face this issue, especially in states that tax based on where work is sourced rather than where you physically perform it. Business owners with customers, employees, or property in multiple states may also owe taxes in each of those states depending on how each state defines economic nexus for income tax purposes.

Additional situations that commonly require multi-state filing include:

- Rental property income from a property located in another state

- Trust or estate income tied to assets held in a different state

- S-corporation or partnership income from a business operating in multiple states

- Gambling winnings earned at a casino located outside your home state

- Sale of real estate or a business interest physically located in another state

Understanding which of these categories applies to your situation is the essential first step before you gather a single document or open a single form. Each scenario follows different rules for how income gets allocated between states, which credits you can claim to avoid double taxation, and what order you need to file the returns in. Getting that foundation right from the start prevents you from having to go back and file amended returns after the fact.

Step 1. Map your states and income sources

Before you open any state tax form, you need a clear picture of every state that touched your money and every state where you spent significant time during the year. This mapping step is the foundation of how to file taxes with multiple states correctly. Skipping it leads to missed filings, unclaimed credits, and the kind of surprises that arrive as penalty notices months after you thought you were finished.

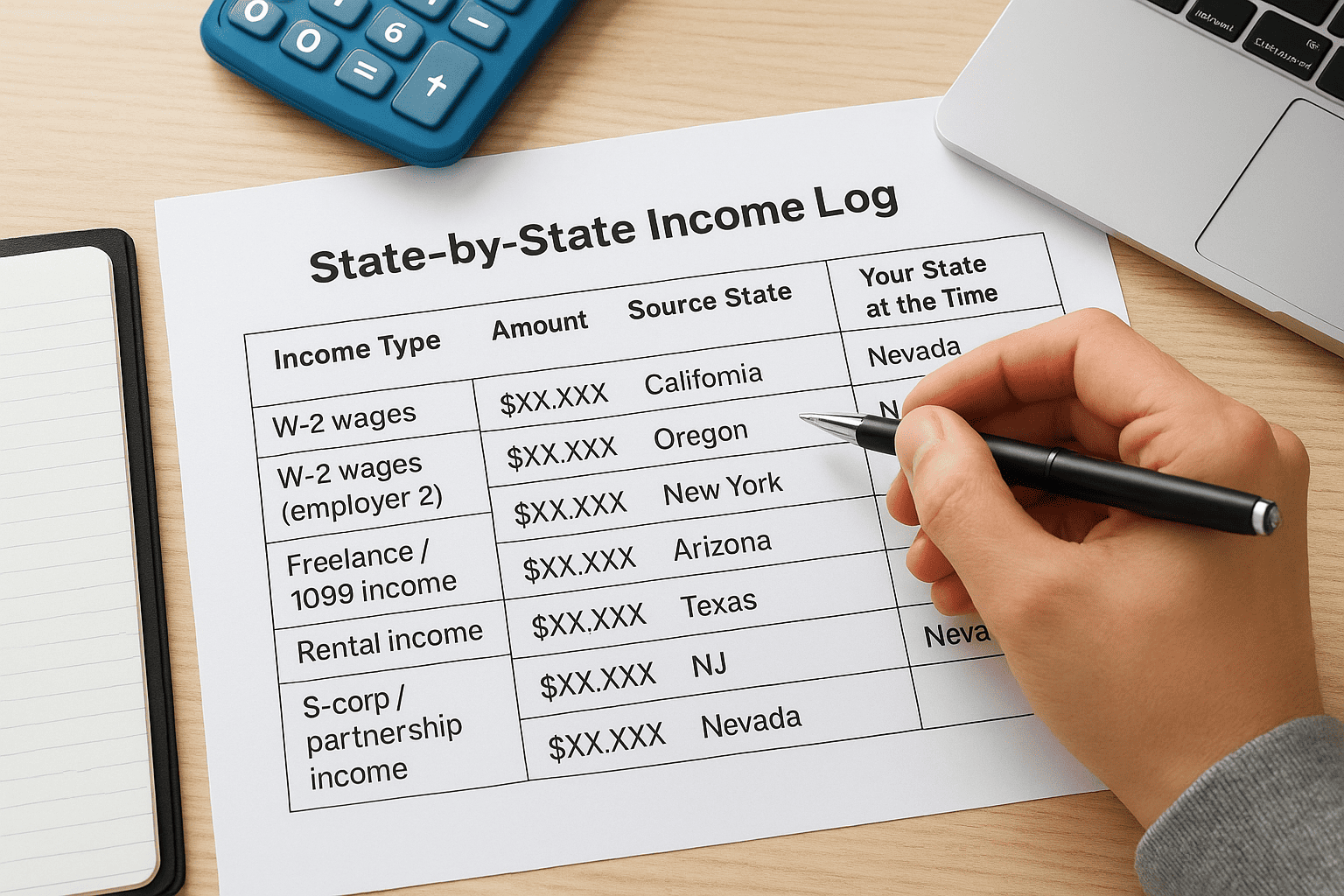

Build a state-by-state income log

Start by pulling together every income source you received during the year and identifying where it originated. Your goal is to create a simple log that maps each income type to its source state. This tells you which states have a potential claim on your income and gives you the raw material you need for every step that follows.

Use this template as your starting point:

| Income Type | Amount | Source State | Your State at the Time |

|---|---|---|---|

| W-2 wages (employer 1) | $XX,XXX | California | Nevada |

| W-2 wages (employer 2) | $XX,XXX | Oregon | Oregon |

| Freelance / 1099 income | $XX,XXX | New York | Nevada |

| Rental income | $XX,XXX | Arizona | Nevada |

| S-corp / partnership income | $XX,XXX | Texas | Nevada |

| Gambling winnings | $XX,XXX | New Jersey | Nevada |

Fill in every row that applies to your situation. If you worked remotely for a company headquartered in another state, list both the state where your employer is based and the state where you physically performed the work, because some states tax based on where work is sourced rather than where you sat at your desk.

Track the states where you physically worked or lived

Beyond income sources, you also need to log every state where you physically worked, even temporarily. A two-week project in Illinois or a month at a client site in Georgia can create a nonresident filing obligation depending on each state's specific threshold rules.

Keep a running calendar of workdays by state throughout the year. Reconstructing your location history after the fact is difficult and often inaccurate, which can create problems if a state ever questions your return.

Go through your email records, travel receipts, hotel stays, and employer records to confirm where you worked each month. Once you have both your income log and your location log complete, you have everything you need to move into the next step.

Step 2. Confirm residency status and domicile

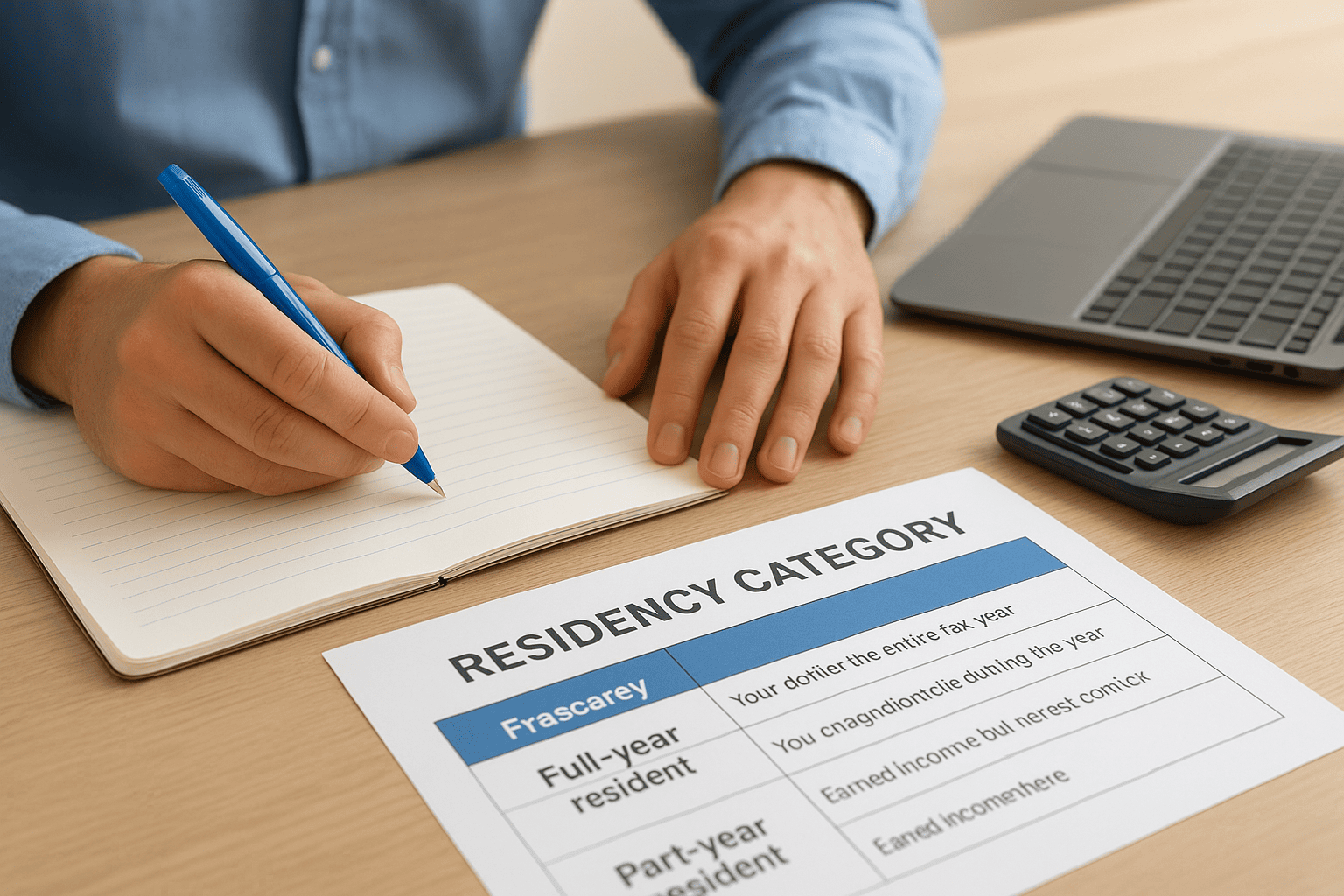

Knowing where your income came from is only half the picture. Residency status determines how much of your income each state can actually tax, and getting it wrong is one of the most common mistakes people make when figuring out how to file taxes with multiple states. States recognize three categories: full-year resident, part-year resident, and nonresident, and each category carries a different scope of taxable income and a different set of forms.

Understanding domicile vs. statutory residency

These two terms sound similar but they mean different things, and states use both when deciding whether you owe taxes there. Your domicile is the state you treat as your permanent home, the place you intend to return to even when you travel or temporarily live somewhere else. Statutory residency, on the other hand, is a rule that some states apply to people who spend a significant number of days inside the state, regardless of where their domicile actually is.

New York is one of the most aggressive states on this point: if you maintain a permanent place of abode in New York and spend more than 183 days there in a year, New York treats you as a statutory resident and taxes your entire income, even if your legal domicile is in another state.

States look at several specific factors when evaluating a domicile claim:

- Location of your primary home and where you sleep most nights

- State where you hold a driver's license and register your vehicles

- Location of your bank accounts, doctors, and professional affiliations

- Where your immediate family lives full-time

- State where you vote and hold active professional licenses

How to determine your residency category

Once you understand domicile, you need to assign yourself a residency category for each state on your list from Step 1. Pull up your location log and apply the following framework to each state you identified as a potential filing obligation.

| Residency Category | Definition | Tax Scope |

|---|---|---|

| Full-year resident | Your domicile for the entire tax year | All income from all sources worldwide |

| Part-year resident | You changed your domicile during the year | Income earned while domiciled in that state |

| Nonresident | Earned income there but never established domicile | Only income sourced within that state |

Write the correct category next to each state on your list. This single classification drives every calculation that follows, including how you allocate income between states and which credits your resident state will allow you to claim against taxes you paid elsewhere.

Step 3. Check reciprocity and remote-work rules

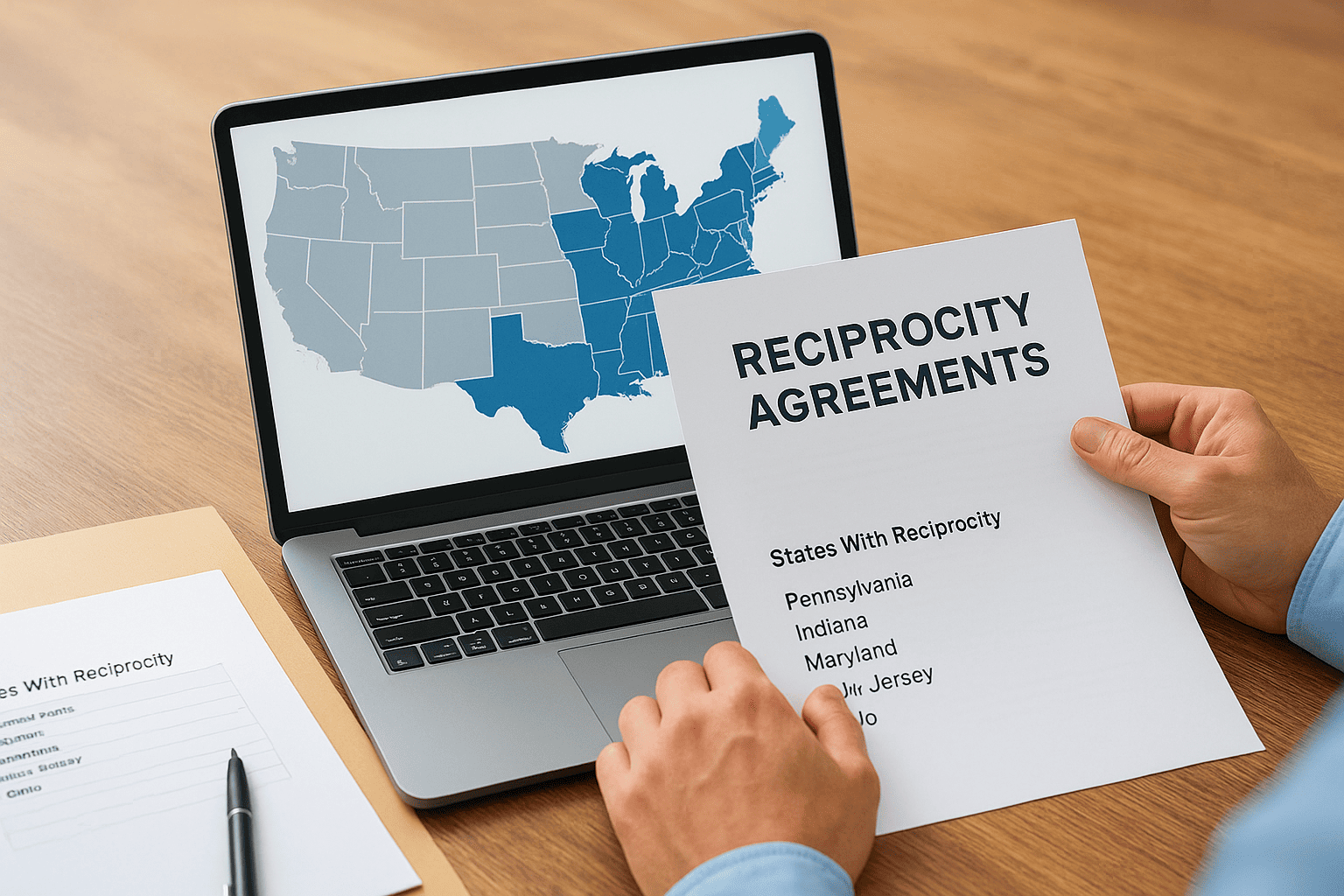

Once you know your residency category for each state, verify whether any reciprocity agreements apply to your situation before you start pulling forms. These agreements can eliminate the need to file a nonresident return entirely, which is one of the most useful shortcuts in figuring out how to file taxes with multiple states correctly.

How reciprocity agreements work

Reciprocity agreements are contracts between neighboring states that let you pay income tax only to your home state, even if you earn wages in the other state. Your employer in the work state withholds taxes for your resident state instead, and you file one resident return rather than a resident return plus a nonresident return. Not every state participates, and agreements only cover earned wages, not rental income, business income, or capital gains.

Here are some of the most common reciprocity pairs currently in effect:

| State You Work In | States With Reciprocity |

|---|---|

| Pennsylvania | Indiana, Maryland, New Jersey, Ohio, Virginia, West Virginia |

| Maryland | Pennsylvania, Virginia, West Virginia, Washington D.C. |

| Michigan | Illinois, Indiana, Kentucky, Minnesota, Ohio, Wisconsin |

| Virginia | Kentucky, Maryland, Pennsylvania, West Virginia |

| New Jersey | Pennsylvania |

If your employer withheld taxes for the wrong state, file a nonresident return to claim a full refund from the work state, then pay the correct amount to your home state. Skipping that refund request means you pay tax twice on the same wages.

Remote-work rules and the convenience-of-employer doctrine

Remote work adds a complication that reciprocity agreements do not address. Some states apply the convenience-of-employer doctrine, which taxes your wages based on where your employer is located rather than where you physically worked. New York is the most prominent example of this: if your employer is a New York company and your remote arrangement exists for your own convenience rather than a business necessity of the employer, New York claims the right to tax your income even if you never worked inside the state all year.

States that currently apply this doctrine include New York, Delaware, Nebraska, Pennsylvania, and Connecticut. If your employer is headquartered in any of these states, verify your withholding situation with that state's department of revenue or a qualified tax professional before you assume your wages are taxable only where you sat at your desk. Misreading this rule consistently produces unexpected tax bills and penalty notices.

Step 4. Collect documents and state income details

Gathering the right documents before you open a single state form is what separates a smooth filing process from one that requires multiple revisions. When you're working through how to file taxes with multiple states, missing one document can force you to estimate figures and then file amended returns later, which costs you time and money. Pull everything together first, organize it by state, and then start preparing your returns in the correct sequence.

Gather your federal and state withholding forms

Your W-2s are the starting point for every state filing you need to complete. Each W-2 your employer issues should list state wages and state income tax withheld in boxes 15 through 17, and some W-2s cover multiple states on the same form if your employer ran payroll across state lines during the year. If you received 1099-NEC or 1099-MISC forms for freelance or contract work, check whether the payer reported state withholding in the bottom section of the form, because many do not withhold for nonresident states, which means you may owe a balance when you file.

If your W-2 shows the wrong state in box 15, contact your employer's payroll department before filing, because correcting it requires a W-2c and potentially amended state returns in every state involved.

Here are the core documents to collect for every state on your list:

- W-2 forms from all employers, including any that show multiple states in boxes 15 through 17

- 1099-NEC, 1099-MISC, and 1099-K forms for freelance or platform income

- 1099-G forms if you received state unemployment benefits in any state

- K-1 forms from any partnership, S-corp, or trust with multi-state activity

- Schedule E records and lease agreements tied to out-of-state rental properties

- Gambling winnings statements (W-2G) showing the specific state where you won

Pull state-specific allocation details

Once you have your federal documents, you need state-level income breakdowns that your federal forms alone will not provide. For each state where you earned income, you need the exact dollar amount belonging to that state, not just your total annual income figure. Your employer's payroll records are the best source for this, and you can request a pay-period-by-period breakdown showing which wages were allocated to which state throughout the year.

For rental properties, pull your gross rents, depreciation schedules, and mortgage interest statements tied to each property's specific state. For business income, gather profit-and-loss statements separated by state if your accounting software tracks location-based revenue. Having these precise figures ready now prevents guesswork when you move into the income allocation step.

Step 5. Allocate wages, business, and other income

With your documents organized, you now need to assign specific dollar amounts to each state on your list. Income allocation is where most multi-state filers make calculation errors, because the total income on your federal return gets divided between states using different formulas depending on the income type. Understanding which method applies to each category is the core mechanical task of how to file taxes with multiple states correctly.

Allocating W-2 wages across states

W-2 wages are allocated based on the days or weeks you physically performed work in each state, unless a convenience-of-employer rule or reciprocity agreement changes that calculation. Most states use a day-count apportionment formula: divide the number of days worked in that state by your total workdays for the year, then multiply by your total wages.

Here is the formula laid out in plain terms:

| Variable | How to Find It |

|---|---|

| Days worked in State A | Count from your workday calendar log |

| Total workdays in the year | All days you performed paid work |

| Total W-2 wages | Box 1 of your W-2 |

| State A wages | (Days in State A / Total workdays) x Total wages |

For example, if you worked 200 total days and spent 60 of those days performing work physically inside Illinois, Illinois can tax 30 percent of your wages. Apply this calculation separately for each state on your list, and confirm that your allocations add up to your total W-2 wages so nothing gets double-counted or missed.

Keep your workday calendar from Step 1 next to you during this calculation, because one wrong day count can shift hundreds of dollars between states.

Allocating business and rental income

Business income follows different rules than wages, and the specific formula depends on your entity type and each state's apportionment method. For sole proprietors and single-member LLCs, most states use a sales factor: the percentage of your revenue earned from customers located in that state divided by your total revenue nationwide. Multiply that percentage by your net business profit to get the amount taxable in that state.

Rental income is the most straightforward to allocate because rental income belongs entirely to the state where the property sits. If you own a rental in Colorado and live in California, every dollar of net rental income from that property goes on your Colorado nonresident return, not your California resident return. Pull your Schedule E figures for each property and assign the full net amount to its physical location before moving to the next step.

Step 6. Prepare nonresident and part-year returns

Once you have your income allocated by state, you prepare nonresident and part-year returns before you touch your resident return. This order is deliberate, and it is the part of how to file taxes with multiple states that most filers get wrong. Your home state needs the exact tax liability from each nonresident return before it can calculate the credit that prevents double taxation, so working in the wrong sequence means you end up guessing at credit amounts and filing amended returns to fix them.

Complete each nonresident return separately

Every state where you earned income but did not live requires its own nonresident return, and each state uses a slightly different form. Most nonresident returns follow the same basic structure: you report your total income from all sources, then apply an apportionment percentage that limits the state's tax to only the portion you earned within its borders. The taxable amount you calculated in Step 5 feeds directly into this line.

Keep a printed or saved copy of every completed nonresident return before you move to Step 7, because your resident state will ask for the exact tax liability shown on each of these returns when you calculate your credit for taxes paid elsewhere.

Here is the standard flow you follow for each nonresident state:

- Enter your total federal adjusted gross income on the nonresident return

- Apply the apportionment percentage (state-source income divided by total income)

- Calculate the state tax on the apportioned amount

- Apply any nonresident-specific deductions or exemptions the state allows

- Subtract withholding already paid to confirm your balance due or refund

Prepare part-year resident returns

Part-year returns combine elements of both a resident and a nonresident return, which makes them the most detailed forms in a multi-state filing. For the period you lived in the state, you report income from all sources worldwide. For the period before you arrived or after you left, you report only income sourced within that state. Most states use a single form with separate columns or schedules to separate the two periods cleanly.

Your move date from the location log you built in Step 1 serves as the dividing line for every income item. Each amount gets assigned to either the resident period or the nonresident period based on when you received it, not when you earned it, unless the state's instructions specify otherwise. Read the instructions for each specific state carefully on this point before entering any figures, because getting this split wrong changes your tax liability in both states.

Step 7. File your resident return and claim credits

Your resident return is the last return you prepare, and it pulls together every figure you calculated in the previous steps. This sequencing is the single most important structural rule in figuring out how to file taxes with multiple states, because your resident state taxes all of your worldwide income and then offers a credit to offset what you already paid to other states. Without the completed nonresident returns sitting in front of you, you cannot accurately calculate that credit.

File after your nonresident returns are complete

Open your resident state return only after you have finalized the tax liability on every nonresident and part-year return from Step 6. Your resident state requires the exact amount of tax you owed to each other state, not the amount withheld or the amount you paid, but the actual computed tax liability shown on those returns. If you prepare your resident return first and estimate that figure, you will almost certainly file an amended return later to correct it.

Pull the "tax liability" line from each nonresident return and write it on a separate sheet before you open your resident return, so you can transfer the numbers without flipping back and forth between forms.

Enter your full federal adjusted gross income on your resident return, including every income source regardless of which state it came from. Your resident state starts from your total income and then reduces the tax you owe through the credit mechanism, not by excluding out-of-state income from the calculation entirely.

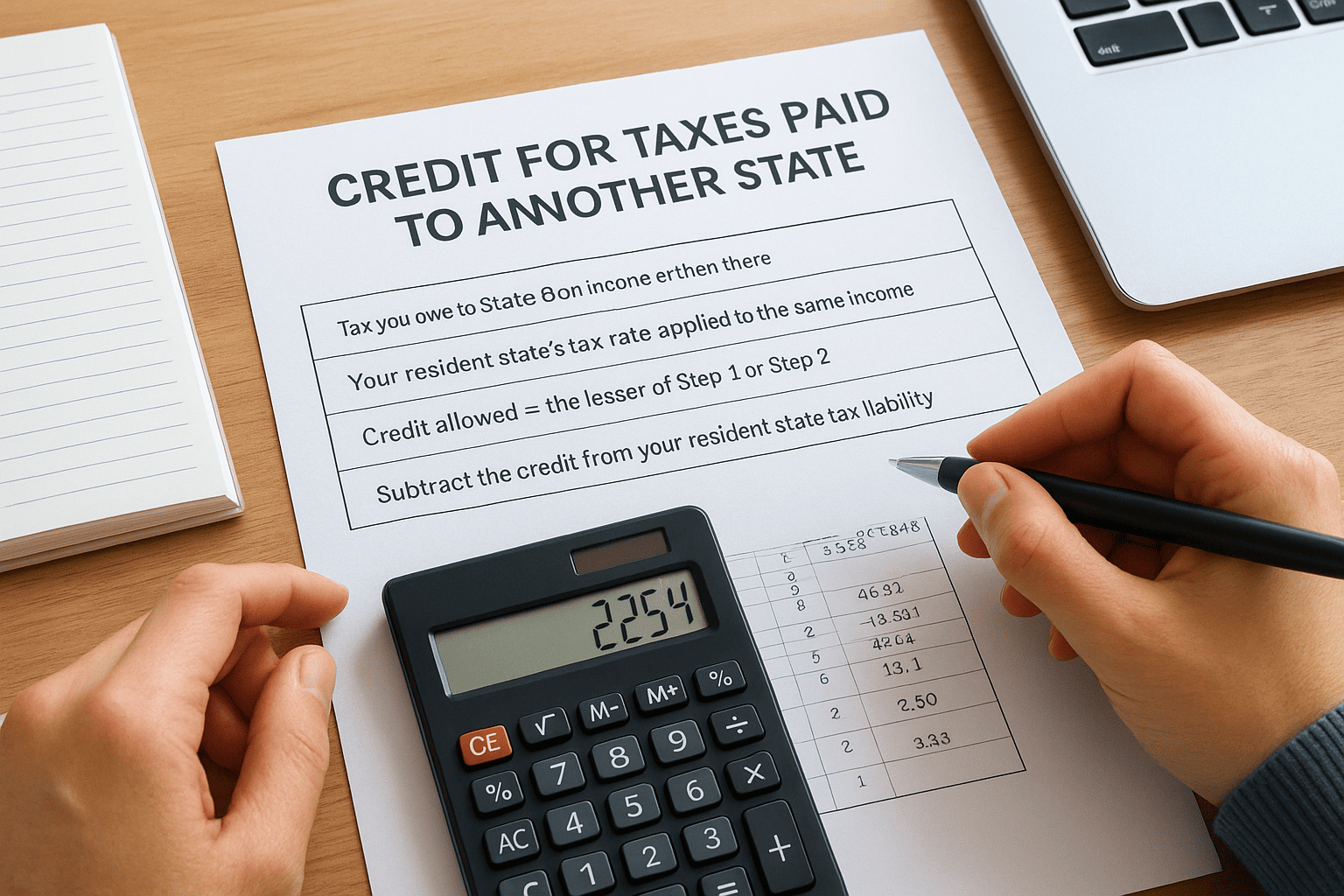

How to calculate the credit for taxes paid to another state

Most states call this the credit for taxes paid to another state, and it appears as a dedicated schedule or worksheet in your resident state's return package. The credit calculation follows a straightforward formula, but it caps at a specific amount to prevent you from claiming more than your resident state would have taxed on the same income.

Here is the standard credit calculation template:

| Step | What You Calculate |

|---|---|

| 1 | Tax you owe to State B on income earned there |

| 2 | Your resident state's tax rate applied to the same income |

| 3 | Credit allowed = the lesser of Step 1 or Step 2 |

| 4 | Subtract the credit from your resident state tax liability |

Apply this calculation once for each nonresident state where you owed tax. Enter each credit on the appropriate line of your resident return's credit schedule, then subtract the combined total from your gross resident tax before applying withholding to determine your final balance due or refund.

Step 8. Avoid errors, fix withholding, keep records

Completing your returns is not the finish line. The last step in how to file taxes with multiple states is a quality-check pass that catches calculation mistakes, fixes withholding for future years, and organizes the records you need to defend your filings if a state audits you later. Skipping this step is the difference between a clean filing and a penalty notice that arrives six months after you thought you were done.

Catch the most common multi-state filing errors

Before you submit anything, review each return for the errors that trip up multi-state filers most often. The most expensive mistake is filing your resident return before your nonresident returns are final, which forces you to estimate your credit for taxes paid to another state. A close second is carrying the wrong income allocation figure from Step 5 onto a nonresident return, which shifts your tax liability between states and can produce a balance due in one state and an overpayment in another.

Run through this checklist before you file each return:

- Confirm that the income allocated to each nonresident state adds up to your total income without any amount counted twice

- Verify that the tax liability figure on each nonresident return matches exactly what you entered on your resident credit schedule

- Check that every W-2 box 15 entry matches the state income you reported on the corresponding state return

- Confirm your move date splits income correctly on any part-year return you prepared

Adjust your withholding for next year

If you owed a significant balance to any state or received a large refund, your current withholding setup is not working for your multi-state situation. Submit a new Form W-4 to your employer to adjust federal withholding, and check whether your employer can withhold for your resident state if they currently withhold only for the work state. For self-employment income, recalculate your quarterly estimated payments for each state based on the income you expect to allocate there in the coming year.

Keep records that protect you if a state audits you

State tax agencies have a longer memory than most filers expect, and strong documentation is your only protection if a state questions your residency status, your income allocation, or your credit calculations years after you filed. Store organized copies of every supporting document in a dedicated folder for each tax year.

Most states can audit a return for three to four years after the filing date, so hold every supporting document for at least five years.

Keep the following for each state return you file:

- A copy of the completed state return with all schedules attached

- The workday calendar you used to allocate wages, including travel receipts and hotel records

- All W-2s, 1099s, and K-1s that show state income breakdowns

- Proof of your move date if you filed as a part-year resident, such as a lease agreement, utility transfer confirmation, or closing documents

Wrap up and what to do next

Knowing how to file taxes with multiple states comes down to working through each step in the right order: map your income, confirm your residency status, check reciprocity rules, gather your documents, allocate income correctly, prepare nonresident and part-year returns first, and then claim your credit on your resident return. Each step feeds directly into the next, so cutting corners early creates compounding problems by the time you reach your final filing.

Your situation may be straightforward, or it may involve overlapping residency claims, a convenience-of-employer dispute, or business income spread across several states. When the complexity goes beyond what a standard tax software package handles, working with a qualified professional protects you from costly errors. The team at Tax Experts of OC handles multi-state filings for clients nationwide, with direct access to a CPA and Enrolled Agent who can sort through your specific facts and file every return correctly.